With a market cap of $22.7 billion, Edison International (EIX) is one of the nation’s largest electric utility holding companies, providing clean and reliable energy through its subsidiaries. Through Southern California Edison and Edison Energy LLC, the company delivers electricity across a 50,000-square-mile area and offers global decarbonization and energy solutions to diverse customers.

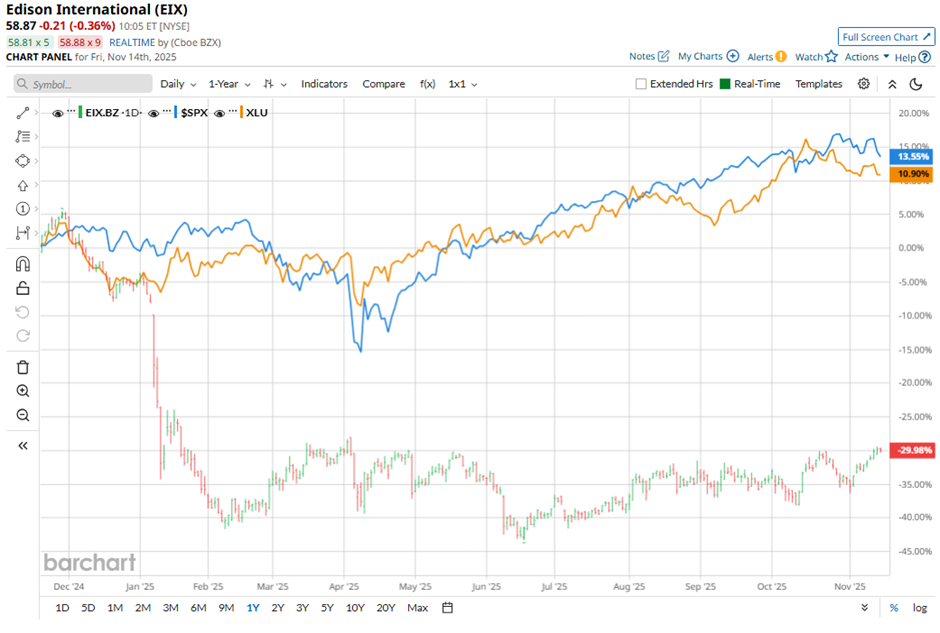

Shares of the Rosemead, California-based company have underperformed the broader market over the past 52 weeks. EIX stock has declined 28.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 12.6%. Moreover, shares of the company are down 26.3% on a YTD basis, compared to SPX's 13.9% gain.

Looking closer, shares of the electric power provider have also lagged behind the Utilities Select Sector SPDR Fund's (XLU) 13.5% rise over the past 52 weeks.

Despite reporting stronger-than-expected Q3 2025 adjusted EPS of $2.34 on Oct. 28, shares of EIX fell 1.2% the next day. The company narrowed its full-year 2025 core EPS guidance to $5.95 - $6.20. Additionally, investors may have been cautious about exposure to wildfire & regulatory risks in California, even with positive steps like the passage of SB 254 and the GRC decision.

For the fiscal year ending in December 2025, analysts expect EIX's adjusted EPS to grow 23.7% year-over-year to $6.10. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

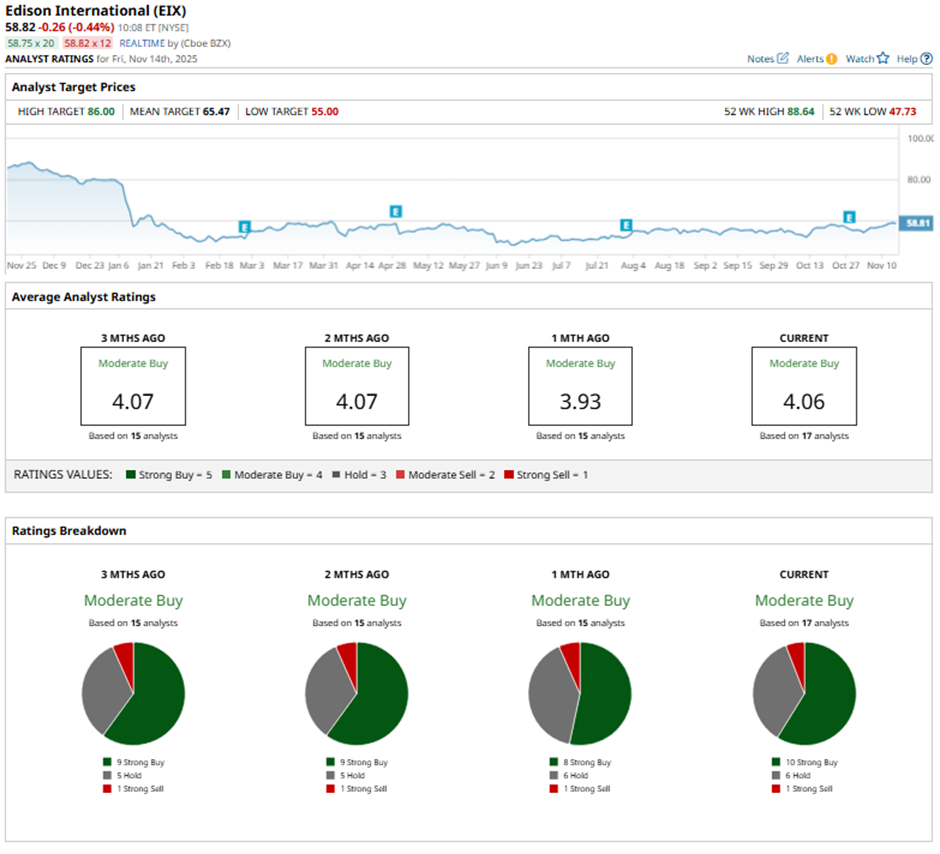

Among the 17 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, six “Holds,” and one “Strong Sell.”

This configuration is slightly more bullish than three months ago, with nine “Strong Buy” ratings on the stock.

On Oct. 30, Ladenburg’s Paul Fremont raised the price target on Edison International to $55 while maintaining a “Neutral” rating.

The mean price target of $65.47 represents a premium of 11.3% to EIX's current price. The Street-high price target of $86 suggests a 46.2% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- I’m Old Enough to Remember When a 500-Point-Drop in the Dow Jones Was a Crisis. Now It’s Just a Warning.

- Down 26% in the Past Month, Mizuho Analysts Still Think Oracle Stock Can Soar 93%. Should You Buy ORCL Now?

- Disney Stock 2026 Forecast: Can Streaming and Parks Make Up for a Linear TV Decline?

- Legendary Investor Michael Burry Warns That Cloud Growth Is Slowing Despite AI Boom. Is This a Bubble?