Stablecoins emerged as that somber, boring cousin of their much flashier counterpart, cryptocurrency. Pegged to the U.S. dollar and other national currencies, stablecoins have much less volatility than cryptos, while they are also gaining rapid acceptance as a secure medium of exchange.

However, since Circle (CRCL), the issuer of the second-largest stablecoin, USDC, made its debut on the markets this year, stablecoins have garnered much attention. Although CRCL stock is down slightly from its listing price, the company has been on a steady path of growth. This has not escaped the notice of some market heavyweights.

Wood and Morgan Circling Around Circle

The first noteworthy endorsement of the Circle stock came from maverick investor Cathie Wood. Known for making high-profile bets on revolutionary tech companies, Wood picked up Circle shares worth $30 million. Further, across various ETFs managed by her, Wood purchased about 353,000 shares of the company.

Earlier, Wood sounded optimistic about stablecoins as she stated that they are "usurping part of the role that we thought Bitcoin would play." She explained that while Bitcoin (BTCUSD) was originally expected to serve as a store of value and a dollar proxy, especially in emerging markets, stablecoins like USDC and USDT have become the go-to solution for payments and savings in these economies due to their price stability. This shift has led Wood and her team at ARK Invest to lower their Bitcoin price target by about $300,000 (from $1.5 million to $1.2 million) because stablecoins are capturing a significant monetary function that was previously assumed to be Bitcoin's domain.

On the other hand, investment banking giant J.P. Morgan is so gung-ho about the company that it has double upgraded the stock to “Overweight” from “Underweight.” Raising the price target to $100 from $94, the broker stated, “The quarterly results indicate to us that stablecoins are continuing to make their way into mainstream financial services, with USDC a leading stablecoin and Circle a leading partner. We also see that Circle is bringing more USDC on-platform, which will enable Circle to continue to boost growth while allowing it to more heavily invest in the buildout of its network.”

Now, with these two enthusiastic voices of support in its corner, will the Circle stock be able to come out of its circle of underperformance? Let's analyze.

What Makes Circle Unique?

Circle is well-placed to harness the potent network dynamics and achieve broad uptake, as USDC delivers swifter and more cost-effective transactions relative to legacy payment mechanisms. The stablecoin holds considerable upside amid its integration into conventional commerce and institutional workflows, positioning the issuer to challenge established payment networks through its distinctive ties to both conventional finance and cryptocurrency ecosystems. Among these alliances, collaborations with Kraken and Deutsche Börse Group are set to act as an adoption catalyst of USDC alongside EURC, Circle's euro-backed stablecoin.

Notably, the arrangement with Kraken specifically enhances worldwide accessibility and functionality for USDC and EURC, leveraging the exchange's infrastructure to host on-chain financial services. Meanwhile, the tie-up with Deutsche Börse Group will hasten stablecoin penetration across Europe by embedding Circle's offerings within the exchange operator's established framework, thereby equipping market actors with tailored implementation tools.

A further catalyst for USDC's competitive expansion lies in its agreement with Binance, the dominant global cryptocurrency exchange. Effective from December 2024, the platform has extended USDC availability to its 240 million users, amplifying reach and liquidity.

Meanwhile, what sets Circle's USDC apart from Tether's USDT is the former's emphasis on transactional efficiency and stringent adherence to regulatory standards, in contrast to USDT's primary alignment with cryptocurrency exchanges and high-volume international transfers.

Challenges persist, nonetheless. The bulk of Circle's income derives from yields on the cash equivalents and short-dated instruments underpinning USDC reserves, a model vulnerable to downturns in a quantitative easing regime that could compress interest margins. Compounding this, the firm allocates a substantial fraction of gross receipts as distribution incentives to key wallet providers, including Coinbase and Binance. Amid declining rates and a growth-first posture, the revenue less distribution cost (RLDC) margin has contracted to 38%, implying that only 38 cents of net proceeds accrue per dollar of interest generated.

Increasing USDC circulation, however, could offset some of this pressure. In a related development, Circle unveiled the Arc blockchain in recent months, a dedicated payment ledger optimized for USDC flows, serving as an alternative to third-party networks like Ethereum. Through this, the company can collect transaction-based "gas" fees, introducing a novel income channel absent from its 2024 profile. Though adoption remains nascent, with broader traction still unfolding, Arc diversifies Circle's earnings base away from pure interest dependency.

“Stable” Financials

Despite the decline in the CRCL stock post its Q3 2025 results, the company's results were undisputably strong, with the company reporting a beat on both the topline and bottom line.

Circle's total revenue and reserve income grew by 66% from the previous year to $740 million, as the USDC in circulation jumped by 108% in the same period to $73.7 billion. Earnings per share for the quarter came in at $0.64 compared to break-even in the prior year. The EPS came in much higher than the consensus estimate of $0.19 per share.

A 96bps drop in the reserve return rate, however, to 4.2% spooked the markets. It is a key metric that represents the weighted-average yield earned on the assets backing its stablecoin supply. In Circle's case, it is USDC. A falling return rate directly pressures profit margins if circulation growth doesn’t offset the rate drop. Thus, this is not much of an alarm for Circle, as USDC circulation growth towers over the slight decline in the reverse return rate.

Shifting attention towards liquidity, Circle closed the quarter with a cash balance of $1.35 billion, much higher than its short-term debt levels of $149.1 million.

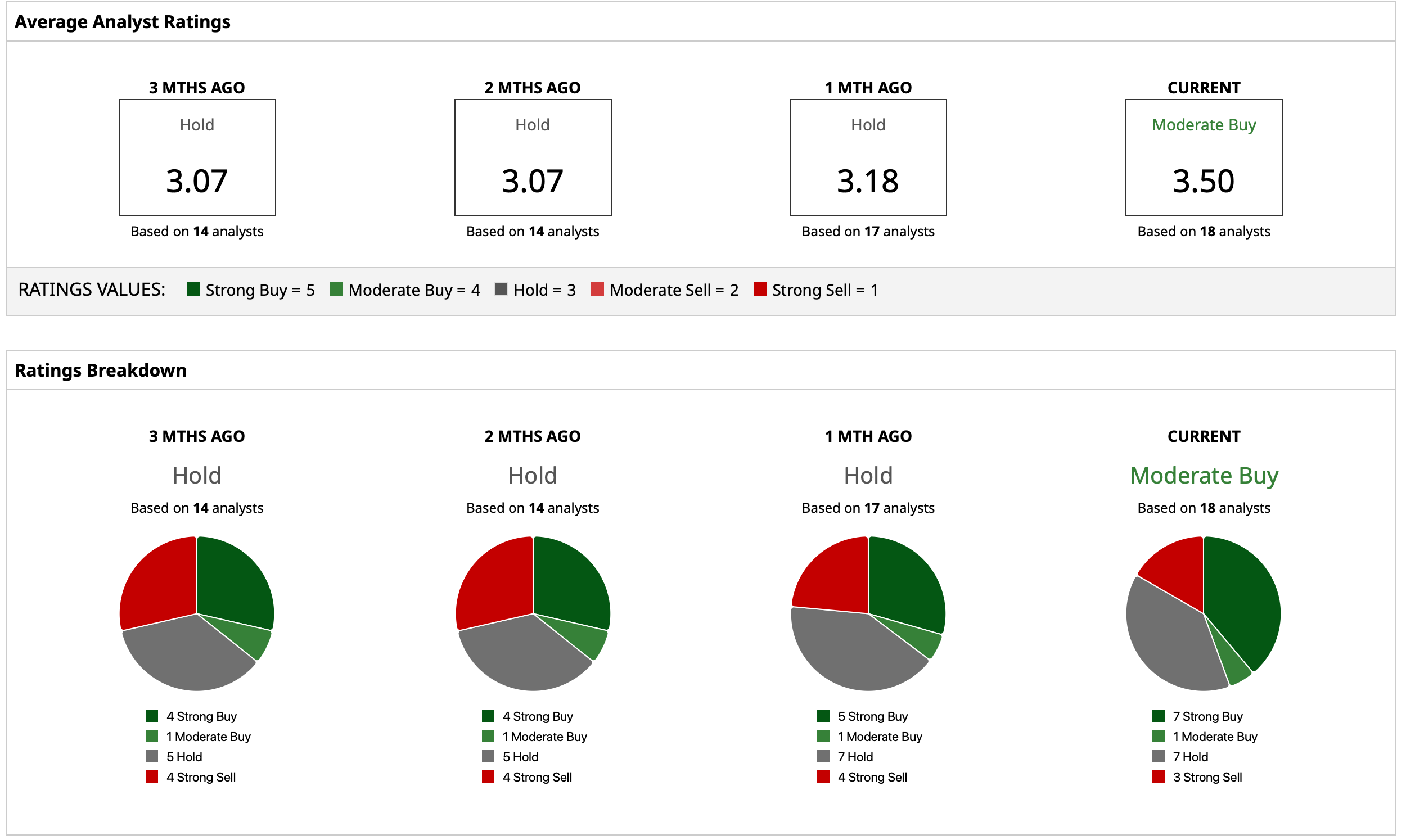

Analyst Opinion on CRCL Stock

Overall, analysts have earmarked a consensus rating of “Moderate Buy” for the CRCL stock, with a mean target price of $167.28. This denotes an upside potential of about 103% from current levels. Out of 18 analysts covering the stock, seven have a “Strong Buy” rating, one has a “Moderate Buy” rating, seven have a “Hold” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- I’m Old Enough to Remember When a 500-Point-Drop in the Dow Jones Was a Crisis. Now It’s Just a Warning.

- Down 26% in the Past Month, Mizuho Analysts Still Think Oracle Stock Can Soar 93%. Should You Buy ORCL Now?

- Disney Stock 2026 Forecast: Can Streaming and Parks Make Up for a Linear TV Decline?

- Legendary Investor Michael Burry Warns That Cloud Growth Is Slowing Despite AI Boom. Is This a Bubble?