Broadcom (AVGO) is scheduled to report its fourth-quarter and fiscal 2025 results on Dec. 11. The stock is heading into earnings with strong momentum after recently hitting new highs.

Investors’ enthusiasm for Broadcom stock stems from the expanding use of its custom semiconductor solutions across the artificial intelligence (AI) ecosystem. Further, AVGO stock got a notable boost when the company secured roughly $10 billion in orders for AI-focused racks powered by its XPUs, Broadcom’s custom accelerators.

Investors’ confidence also received a lift from Google’s (GOOGL) latest Gemini 3 AI model rollout, which was trained on Google’s in-house Tensor Processing Units (TPUs). Since Broadcom co-designs those TPUs, the move served as a strong endorsement of its technology. With rumors that Google will eventually rent out its TPU capacity to external customers, Broadcom stands to benefit as demand for the AI chips it helps build rises.

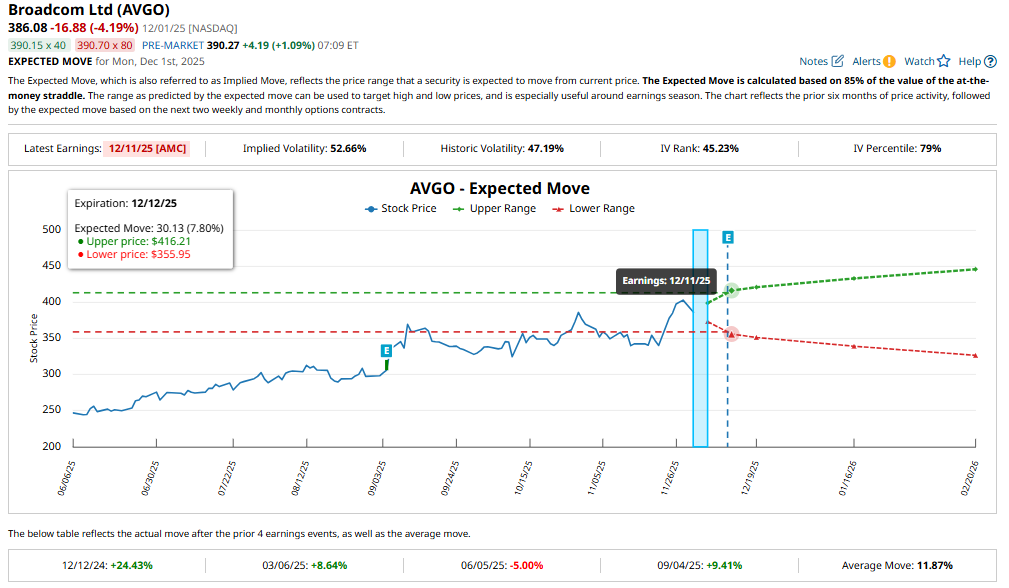

With expectations already high for Broadcom, particularly around AI revenue growth, will the upcoming earnings report be strong enough to push AVGO stock higher? Options traders currently anticipate a move of about 7.8% in either direction following earnings, slightly lower than the stock’s average movement of 11.9% over the past four quarters. Traders should note that AVGO shares leapt more than 9% following the last quarterly report.

Q4 Expectations: Broadcom Positioned for Robust Growth

Broadcom is well-positioned to deliver strong growth in Q4, driven by significant AI-led tailwinds. Furthermore, the addition of a new customer provides a multi-year growth opportunity.

Broadcom delivered revenue of $16 billion in the third quarter, up 22% year-over-year. Moreover, its top-line growth rate accelerated from the 20% increase posted in Q2. Profitability followed suit, with adjusted EBITDA climbing 30% year-over-year to $10.7 billion.

Much of Broadcom’s growth continues to originate from the semiconductor division, which is experiencing a significant uplift from AI. The segment generated $9.2 billion in Q3 revenue, 26% higher than the previous year. This was driven by explosive demand for AI-focused products. AI-related sales surged 63% to $5.2 billion, strengthening from 46% growth reported in Q2. These trends highlight Broadcom’s growing role in powering AI infrastructure. Broadcom’s backlog expanded to $110 billion. This pipeline provides Broadcom with a solid foundation for future growth.

As for Q4, the momentum in Broadcom’s business is likely to accelerate. Broadcom’s management expects Q4 revenue to reach $17.4 billion, up 24% from last year. The forecast reflects a quarter-over-quarter acceleration in growth rate. Semiconductor sales are projected to rise 30%, including a 66% leap in AI semiconductor revenue to $6.2 billion. Even infrastructure software revenue is forecast to grow a healthy 15% to around $6.7 billion.

While its top-line growth rate is likely to accelerate, margins may ease sequentially, reflecting a greater mix of high-growth XPU and wireless products. Even with a sequential decline in gross margins, the company’s bottom-line growth is expected to remain solid.

Analysts expect Broadcom to deliver earnings of $5.42 per share in fisacl 2025, reflecting a 46.1% increase year-over-year. For the current quarter, analysts anticipate EPS of $1.49, up 19.2%. However, note that Broadcom has missed earnings expectations in the last two quarters.

Should You Buy, Sell, Or Hold Broadcom Stock?

Broadcom is expected to deliver strong growth in Q4 led by demand for its AI-focused products. Thanks to its solid growth prospects, analysts are bullish on AVGO stock ahead of the Q4 earnings release. However, Broadcom’s shares are no bargain at current levels.

With shares trading at a forward price-earnings (P/E) ratio of roughly 52.5 times, much of the optimism about its future growth is already priced in. Wall Street does expect Broadcom’s earnings to climb substantially in the coming years, including a projected 41.7% jump in fiscal 2026. Even so, the elevated valuation suggests investors might already be paying for much of that future performance today.

In short, Broadcom’s long-term AI opportunities justify the premium price. However, a pullback could be a solid buying opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Analysts Say AWS Will Drive ‘Significant Upside’ for Amazon. Should You Buy AMZN Stock Now?

- This Analyst Predicts Tesla Stock Will Crush Traditional Automakers, ‘They Had Plenty of Warning Time’

- Top 100 Stocks to Buy: Par Pacific Holdings Looks Tempting, But Should You Bite?

- How Should You Play NVDA Stock Amid Reports That China Banned ByteDance from Using Nvidia GPUs?