As the Q3 earnings season wraps, let’s dig into this quarter’s best and worst performers in the agricultural machinery industry, including Titan International (NYSE:TWI) and its peers.

Agricultural machinery companies are investing to develop and produce more precise machinery, automated systems, and connected equipment that collects analyzable data to help farmers and other customers improve yields and increase efficiency. On the other hand, agriculture is seasonal and natural disasters or bad weather can impact the entire industry. Additionally, macroeconomic factors such as commodity prices or changes in interest rates–which dictate the willingness of these companies or their customers to invest–can impact demand for agricultural machinery.

The 5 agricultural machinery stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 0.6% while next quarter’s revenue guidance was in line.

While some agricultural machinery stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.9% since the latest earnings results.

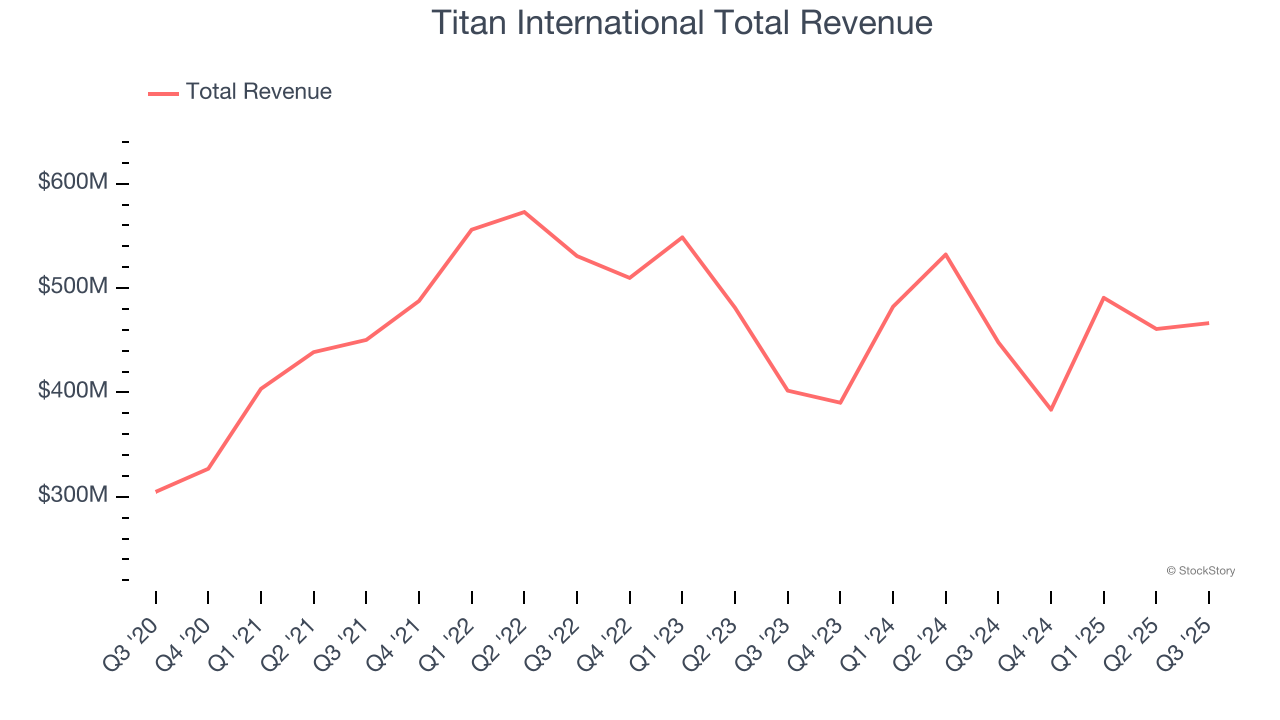

Best Q3: Titan International (NYSE:TWI)

Acquiring Goodyear’s farm tire business in 2005, Titan (NSYE:TWI) is a manufacturer and supplier of wheels, tires, and undercarriages used in off-highway vehicles such as construction vehicles.

Titan International reported revenues of $466.5 million, up 4.1% year on year. This print exceeded analysts’ expectations by 1.7%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Interestingly, the stock is up 1.8% since reporting and currently trades at $8.10.

Is now the time to buy Titan International? Access our full analysis of the earnings results here, it’s free for active Edge members.

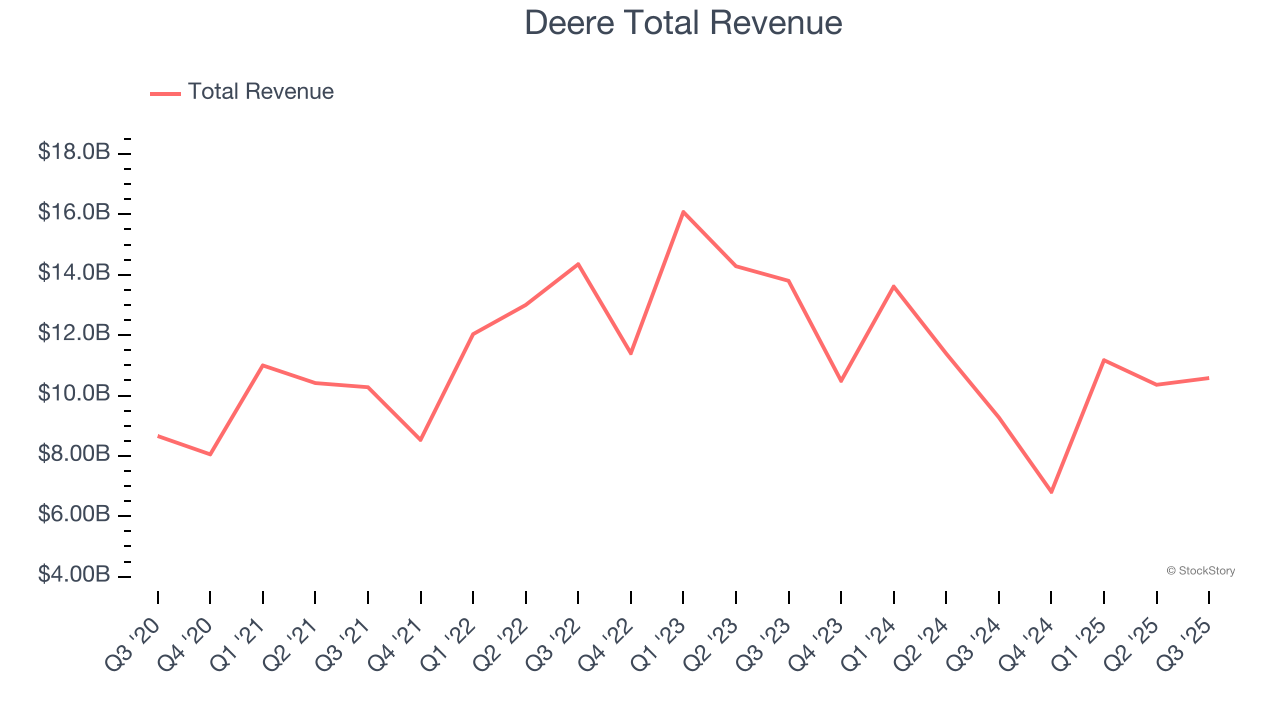

Deere (NYSE:DE)

Revolutionizing agriculture with the first self-polishing cast-steel plow in the 1800s, Deere (NYSE:DE) manufactures and distributes advanced agricultural, construction, forestry, and turf care equipment.

Deere reported revenues of $10.58 billion, up 14.1% year on year, falling short of analysts’ expectations by 9%. However, the business still had a strong quarter with an impressive beat of analysts’ EBITDA estimates and an impressive beat of analysts’ Construction & Forestry revenue estimates.

Deere delivered the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 6.5% since reporting. It currently trades at $465.83.

Is now the time to buy Deere? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Alamo (NYSE:ALG)

Expanding its markets through acquisitions since its founding, Alamo (NSYE:ALG) designs, manufactures, and services vegetation management and infrastructure maintenance equipment for governmental, industrial, and agricultural use.

Alamo reported revenues of $420 million, up 4.7% year on year, exceeding analysts’ expectations by 3.1%. Still, it was a slower quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 7.3% since the results and currently trades at $160.50.

Read our full analysis of Alamo’s results here.

AGCO (NYSE:AGCO)

With a history that features both organic growth and acquisitions, AGCO (NYSE:AGCO) designs, manufactures, and sells agricultural machinery and related technology.

AGCO reported revenues of $2.48 billion, down 4.7% year on year. This result came in 0.5% below analysts' expectations. Taking a step back, it was a mixed quarter as it also logged full-year EPS guidance exceeding analysts’ expectations but a significant miss of analysts’ organic revenue estimates.

AGCO had the slowest revenue growth among its peers. The stock is down 1.4% since reporting and currently trades at $104.64.

Read our full, actionable report on AGCO here, it’s free for active Edge members.

Lindsay (NYSE:LNN)

A pioneer in the field of center pivot and lateral move irrigation, Lindsay (NYSE:LNN) provides a variety of proprietary water management and road infrastructure products and services.

Lindsay reported revenues of $153.6 million, flat year on year. This print beat analysts’ expectations by 1.6%. However, it was a slower quarter as it logged a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

The stock is down 6.3% since reporting and currently trades at $114.87.

Read our full, actionable report on Lindsay here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.