Agnico-Eagle Mines (AEM) shares have more than doubled this year, thanks to the stellar rise in gold prices (GCZ25). While gold prices took a breather and briefly fell below $4,000 per ounce, they have since returned above the psychological price level.

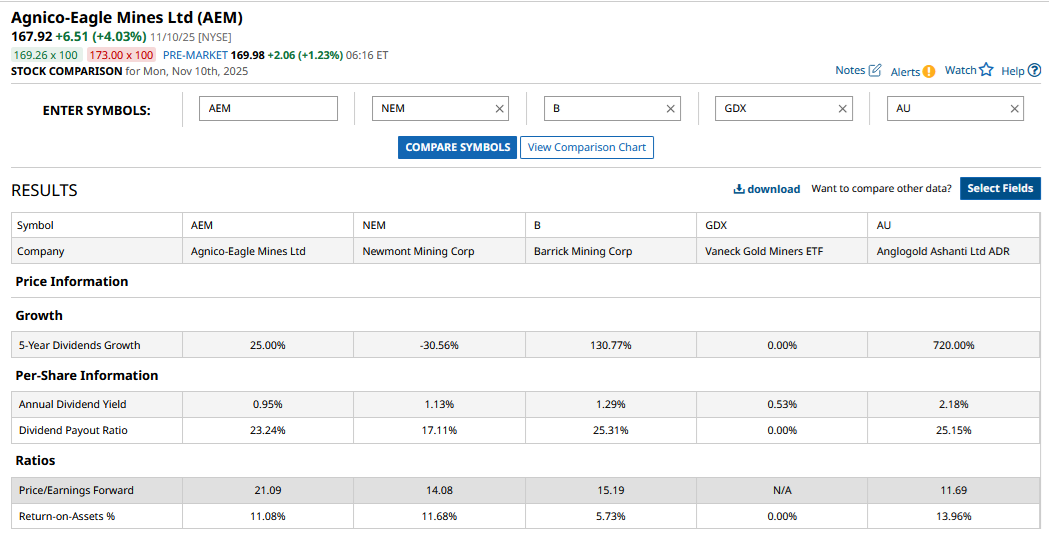

Higher gold prices have meant a free cash flow bonanza for gold miners, which they are invariably using to either deleverage their balance sheets or increase shareholder payouts through higher share buybacks and dividends. Recently, Barrick Gold (B) announced an increase in its dividend, and more gold miners could follow suit over the next couple of months. I believe gold’s outlook looks positive for 2026, and I find AEM a good dividend stock to load up for 2026. Let’s discuss, beginning with a brief overview of the company’s Q3 2025 earnings.

AEM Expects to Meet Its 2025 Guidance

AEM produced 867,000 ounces of gold in the third quarter at an all-in-sustaining cost (AISC) of $1,373 per ounce. For the full year, the company is optimistic about meeting the midpoint of the production guidance, which is 3.3 million ounces, while expecting the AISC to come in at the top end of the guidance at $1,300 per ounce. AEM has seen a rise in its AISC due to the timing of sustaining capex and a rise in cash costs. Notably, AEM's cash costs rose in Q3 due to higher royalties resulting from the surge in gold prices.

AEM is Investing to Enhance Its Production

AEM is investing significantly to enhance its current production. Detour underground, Hope Bay, and Upper Beaver are among the five key projects that the company is focusing on. The company expects these projects – all of which are organic growth opportunities – to represent between 1.3 million to 1.5 million ounces in gold production. It particularly cited the example of the Detour underground project, which, once ramped up to the projected production of 1 million ounces, can alone generate annual after-tax free cash flows of $2 billion at the current gold prices.

AEM’s Capital Allocation Policy

AEM is quite conservative with its capital allocation policy and repaid debt worth $400 million in Q3. The company’s net cash position rose to $2.2 billion in Q3, which basically means that the cash and cash equivalents on its balance sheet exceed its debt by that amount. AEM’s long-term gross debt is now below $200 million, and given the massive free cash flows that the company is generating, it might increase shareholder payouts, as there isn't much deleveraging opportunity left.

AEM currently intends to pay a third of its free cash flows to shareholders in a mix of dividends and share repurchases. While the company reaffirmed during the Q3 call that share repurchases remain its priority, it also talked about “potentially higher dividends.” During the earnings call, CFO Jamie Porter said, “At current gold prices, we’re generating a lot of cash, but we will remain disciplined and continue to take a measured approach to capital allocation with a focus on increasing returns to our shareholders over the long term."

In a nutshell, AEM’s capital allocation policy is maintaining a stable dividend – it has paid one since 1983 – while pursuing opportunistic share repurchases. The company has paid cumulative dividends worth $5 billion in its history, the bulk of which were over the last few years.

I believe AEM might need to seriously consider adding a variable component to its dividend policy, something many other mining companies have pivoted to. Flexible dividends make sense for mining companies as their fortunes are intertwined with the commodity that they produce, which, by nature, is quite volatile. Incidentally, gold, which is otherwise seen as a stable asset, has also been quite volatile in recent months.

While AEM might not increase its base dividend substantially, as cutting it later would send a negative signal, a variable or special dividend might be something that could be up for discussion. This would especially be true now, as the company has nearly repaid all of its debt and would have plenty of cash flows to play around with next year, given where gold prices stand today.

AEM Looks Like a Good Buy for 2026

All said, a possible dividend hike in 2026 notwithstanding, I continue to remain bullish on gold and see AEM as a good play in the gold mining space. The valuations don’t appear stretched at a forward enterprise value-to-earnings before interest, tax, depreciation, and amortization (EV-to-EBITDA) multiple of 10.2x, even as they are admittedly higher than historical averages.

Gold miners look set for a structural re-rating given the euphoria toward the precious metal. Moreover, thanks to strong balance sheets following the stellar cash flows over the last couple of years, gold mining companies, including AEM, can command a premium valuation over their historical averages.

Notably, AEM’s reserves are in “safe” jurisdictions in Canada, Mexico, Australia, and Finland, with Canada accounting for a lion’s share of its production as well as reserves. Markets allot a valuation premium to companies that have their mining assets in safer jurisdictions. Overall, AEM is one dividend stock I am bullish on for 2026 as gold prices look set to continue their momentum.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart