Valued at a market cap of $4.5 trillion, Nvidia (NVDA) is the largest company in the world. The chipmaker has surged over 1,100% in the last three years and a staggering 25,000% in the previous decade. Today, it sits at the epicenter of the artificial intelligence megatrend with an order book that continues to expand every quarter.

Last month, Nvidia CEO Jensen Huang revealed the tech giant has already secured $500 billion worth of orders spanning 2025 and 2026. This figure includes revenue from its current Blackwell graphics processing units, upcoming Rubin chips, and related networking equipment.

The announcement signals that demand for AI infrastructure shows no signs of slowing down despite growing concerns about whether tech giants are overspending.

What to Expect From Nvidia in Fiscal Q3?

Nvidia’s upcoming earnings release will provide analysts and investors with insights into its growth trajectory. According to consensus estimates, Nvidia is forecast to report revenue of $55 billion and adjusted earnings of $1.25 per share in fiscal Q3 of 2026 (ended in October). In the year-ago period, it reported revenue of $35 billion and earnings of $0.81 per share.

Moreover, analysts project revenue in fiscal 2026 to grow by 56.8% year-over-year (YoY) to $61.7 billion, while earnings are expected to increase by 52.31% to $4.55 per share.

The earnings call takes on added importance because Nvidia customers, including Alphabet (GOOG) (GOOGL), Amazon (AMZN), Microsoft (MSFT), and Meta (META), have all recently announced plans to increase their capital spending on AI infrastructure significantly.

Every dollar of that spending flows largely to Nvidia, which controls over 90% of the AI chip market. With analysts estimating the order book implies $60 billion more in calendar 2026 revenue than previously expected, Wednesday's report could validate Nvidia's position as the indispensable supplier powering the AI boom.

Nvidia’s Growing Ecosystem

Nvidia’s order book is remarkable, given that it plans to ship 20 million Blackwell GPUs over roughly five quarters, which is five times the growth rate of its previous Hopper generation. For context, Hopper shipped 4 million GPUs over its entire lifetime.

This explosive growth reflects two compounding forces driving the AI industry. First, the computational requirements for training and running AI models continue to expand exponentially. Second, as AI models become smarter and more useful, more people and businesses rely on them, resulting in a higher demand for computing power.

CFO Colette Kress emphasized that Nvidia now has visibility into gigawatts worth of data center capacity needs already being planned for the Rubin architecture, even though those chips won't reach full production until next year.

As stated earlier, major cloud providers are collectively investing massive amounts in capital expenditures, with Nvidia positioned to capture the lion's share as they build out AI infrastructure. The timing proves fortuitous as Nvidia's Grace Blackwell platform delivers unprecedented performance advantages.

Independent benchmarks show that the GB200 system provides 10 times better performance than the previous generation H200 while simultaneously offering the lowest cost per token generated in the industry.

This combination of superior performance and better economics creates a compelling value proposition that justifies the premium pricing and helps sustain the virtuous cycle driving AI adoption.

Nvidia's competitive moat extends beyond raw chip performance. The company has reinvented computing from the ground up through extreme co-design, developing six different chips simultaneously to optimize the entire data center stack. This comprehensive approach spans processors, networking, memory systems, and software, creating barriers to entry that rivals struggle to overcome.

The CUDA software ecosystem with 350 specialized libraries across different industries further entrenches Nvidia's dominant position. Nvidia announced full-scale Blackwell production in Arizona, marking a significant milestone in American semiconductor manufacturing. With supply chains expanding globally and architectural advantages widening, Nvidia appears well-positioned to capitalize on the AI revolution throughout 2026 and beyond.

What Is the NVDA Stock Price Target?

While Nvidia continues to grow at a robust pace, its trajectory is decelerating. For instance, sales rose by 126% YoY in fiscal 2024 and 114% in 2025. Analysts forecast sales to increase by 59% in 2026, 40% in 2027, and 24.6% in 2028.

Similarly, adjusted earnings expanded by 288% in 2024 and by 131% in 2025. According to consensus estimates, earnings growth is projected to increase by 38% annually between 2026 and 2028.

NVDA stock trades at 31.9 times forward earnings, which is below its 10-year average of 36.9 times. If the tech stock continues to trade at its current multiple, it should gain over 40% over the next 15 months.

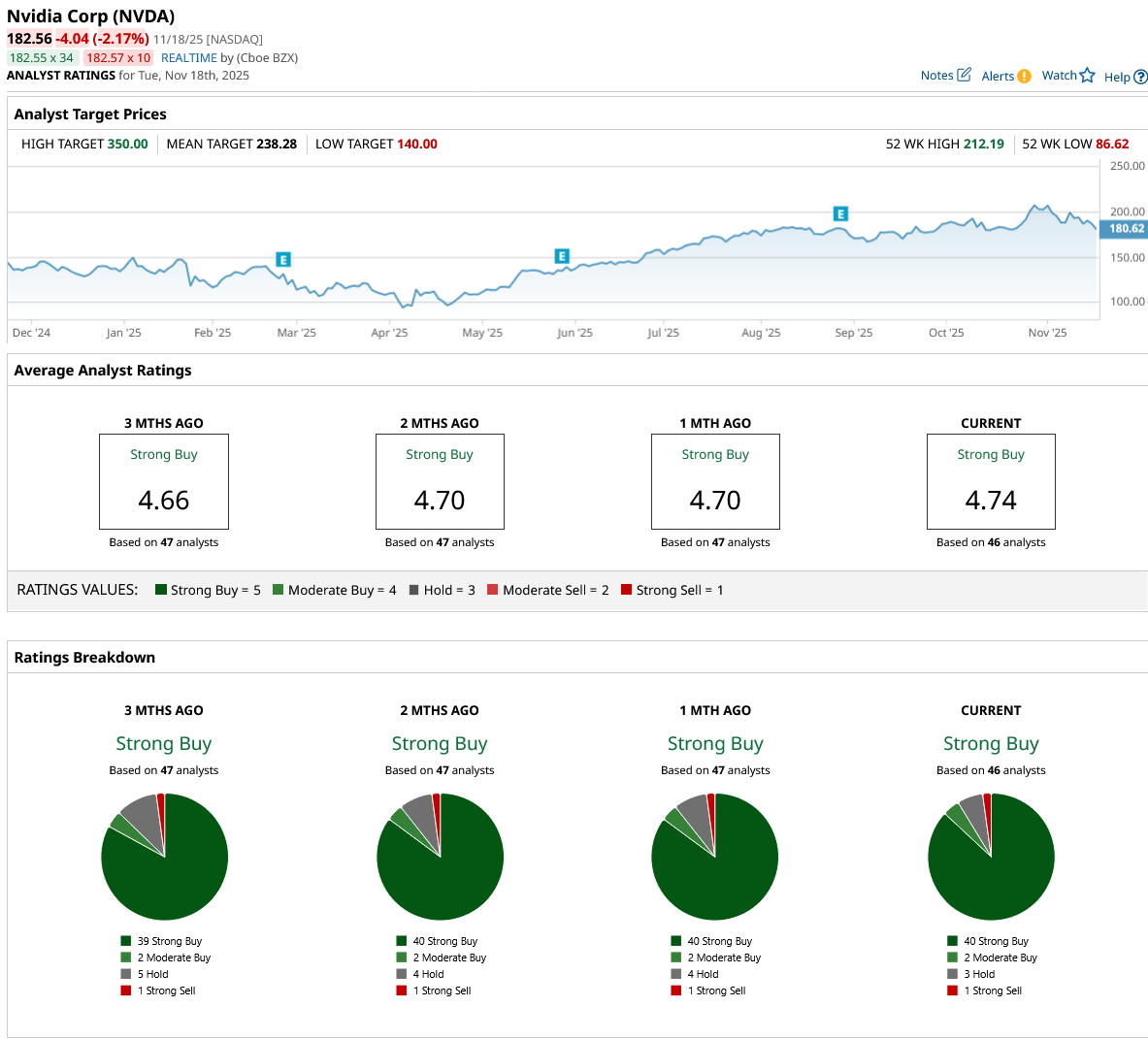

Out of the 46 analysts tracking NVDA stock, 40 recommend “Strong Buy,” two recommend “Moderate Buy,” three recommend “Hold,” and one recommends “Strong Sell.” The average NVDA stock price target is $238, above the current price of $182.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart