Increased Argentinian beef imports under a new lower-tariff quota will add at most 2–2.5% to U.S. supply, offering consumers little immediate grocery-price relief (with any softening likely delayed up to two years), while striking domestic ranchers with tighter margins and slower herd rebuilding as the already decades-low U.S. cattle inventory remains the primary driver of record prices—despite government promises of long-term support that will take years to matter.

Details of key points impacting the cattle market:

- Modest Consumer Price Relief: Experts agree that increased Argentinian beef imports are unlikely to cause sharp drops in U.S. grocery store prices because Argentina's total export volume is a minimal share of the U.S. market (around 2-2.5% of the total U.S. beef supply, even if all its global exports came here). Any relief would likely be modest and potentially delayed for consumers, with a possible lag of up to two years for noticeable effects at the retail level.

- Pressure on U.S. Producers: Imports are expected to have a more significant negative impact on U.S. cattle producers, particularly smaller operations, by eroding profit margins and creating market instability. This added competition could signal downward pressure on live cattle futures and discourage the rebuilding of the domestic herd.

- Tight Domestic Supplies: The U.S. cattle market is currently facing its smallest herd size in decades due to drought and high feed costs, which is the primary driver of record-high domestic beef prices. This tight domestic supply caps how far prices can fall from imports alone.

- Government Action and Timeline: The U.S. government is implementing new trade frameworks to increase the import quota for Argentinian beef at a lower tariff rate, alongside plans to support domestic producers through herd expansion initiatives. However, these domestic expansion measures will take significant time (years) to have a material effect on supply and prices.

- Limited Market Overhaul: The volume of Argentinian beef is too small to overhaul the entire U.S. market overnight, but the governmental intervention is a source of concern and potential instability for the industry.

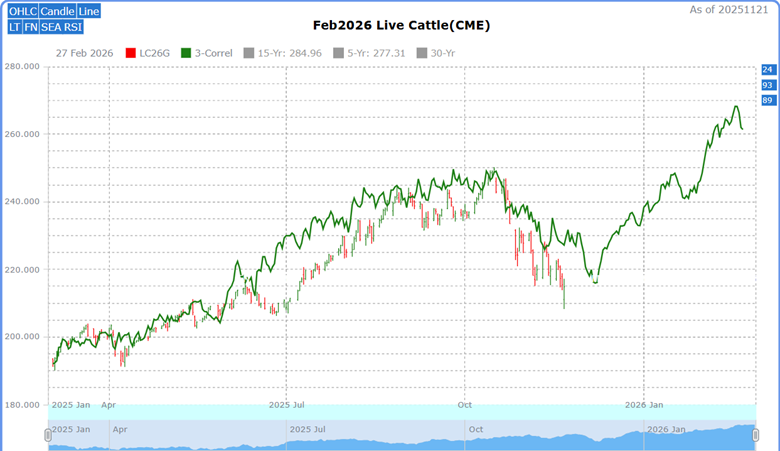

Technical Picture

Source: Barchart

The year-to-date live cattle chart for February shows an impressive uptrend until mid-October, when the Argentina tariff update was announced. Decisively closing below the upsloping 50-day moving average. Since then, the moving average has turned down. Creating a near-term bearish outlook on live cattle prices. Today, as this article is being written, the live cattle market has been locked limit down since the open.

I would have a hard time finding a reason to buy live cattle in this down trend. But trends can change, and with upcoming seasonal and correlated market years, traders may want to add this market to their watch list.

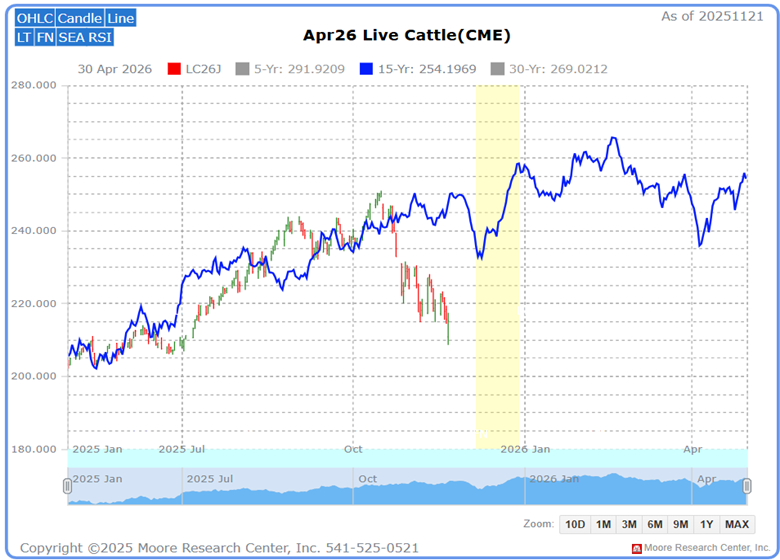

Correlated Market Years

Source: Moore Research Center, Inc. (MRCI)

The current market sell-off may seem extreme, but MRCI research has found there have been three previous years with correlated price action (green) that recovered to rally higher. Those years were 1989 (91%), 1993 (86%), and 2024 (85%). Please keep in mind the significant low in the near future, which will tie into a decent seasonal low.

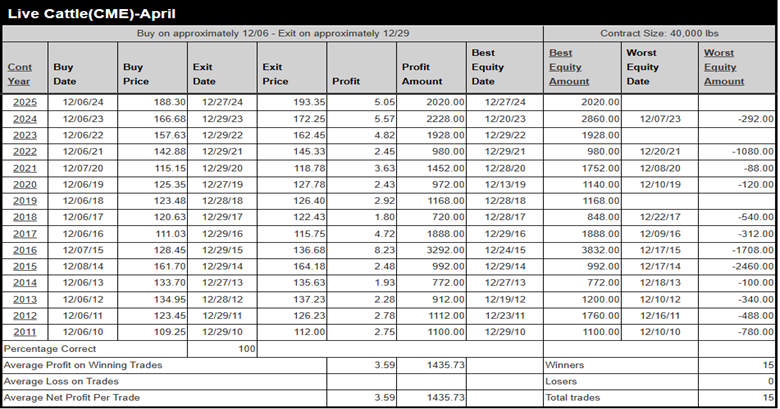

Seasonal Pattern

Source: MRCI

Source: MRCI

Traders, as good as this trade sounds, please remember the current trend is down. Before acting, wait for signs of buying to enter the market to support this setup.

As a crucial reminder, while seasonal patterns can provide valuable insights, they should not be the basis for trading decisions. Traders must consider various technical and fundamental indicators, risk management strategies, and market conditions to make informed, balanced trading decisions.

Assets to Trade Live Cattle

Futures traders could trade the standard-size contract (LE). At this time, there are no ETFs for live cattle alone. There are a few commodity ETFs that blend hogs and cattle.

In Closing….

The technical picture on February live cattle tells the story plain enough: the contract ran straight up through mid-October, then broke hard once the Argentina tariff news hit, slicing below the 50-day moving average and turning it lower for the first time in months. As this is written, the market is locked in a limit-down, bleeding state, reinforcing a clear near-term bearish bias. For anyone holding long cattle contracts or holding cash cattle, the pressure is real and immediate; buying the dip here feels like trying to catch a falling knife.

That said, Moore Research's correlated-year work flags 1989, 1993, and 2024 as years with similar mid-cycle sell-offs that eventually reversed and rallied hard into spring. Those patterns all put in significant lows right around now before turning higher, lining up with the typical December–January seasonal bottom in live cattle. The setup is worth watching, but the trend is still down—wait for confirmed buying (an up-sloping 50-day moving average or a higher swing low) before stepping in. Until then, the path of least resistance remains lower, and the slight bump in Argentinian tonnage only adds another brick to the wall U.S. producers are already up against.

On the date of publication, Don Dawson did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.