Memphis, Tennessee-based AutoZone, Inc. (AZO) operates as a retailer and distributor of automotive replacement parts and accessories. Valued at $64.1 billion by market cap, the company offers an extensive product line for cars, sport utility vehicles, vans, and light trucks, including new and remanufactured automotive hard parts, maintenance items, accessories, and non-automotive products.

Shares of this auto parts retailer have outperformed the broader market over the past year. AZO has gained 24.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 11%. In 2025, AZO stock is up 20.3%, surpassing the SPX’s 14% rise on a YTD basis.

Zooming in further, AZO’s outperformance is also apparent compared to the SPDR S&P Retail ETF (XRT). The exchange-traded fund has declined about 1.8% over the past year. Moreover, AZO’s double-digit returns on a YTD basis outshine the ETF’s marginal dip over the same time frame.

AZO's strong performance was driven by solid execution in retail and commercial channels, with commercial sales outpacing retail growth due to improved inventory availability and faster delivery. The company saw market share gains, favorable weather, and international expansion in Mexico and Brazil, offsetting margin pressures from tariff-related costs and a non-cash LIFO charge. Management remains bullish on long-term growth, investing in stores, inventory, and technology to drive future success.

On Sep. 23, AZO shares fell slightly after reporting its Q4 results. Its EPS of $48.71 missed Wall Street expectations of $50.52. The company’s revenue was $6.24 billion, exceeding Wall Street's $6.22 billion forecast.

For the current fiscal year, ending in August 2026, analysts expect AZO’s EPS to grow 4.5% to $151.32 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimates in each of the last four quarters.

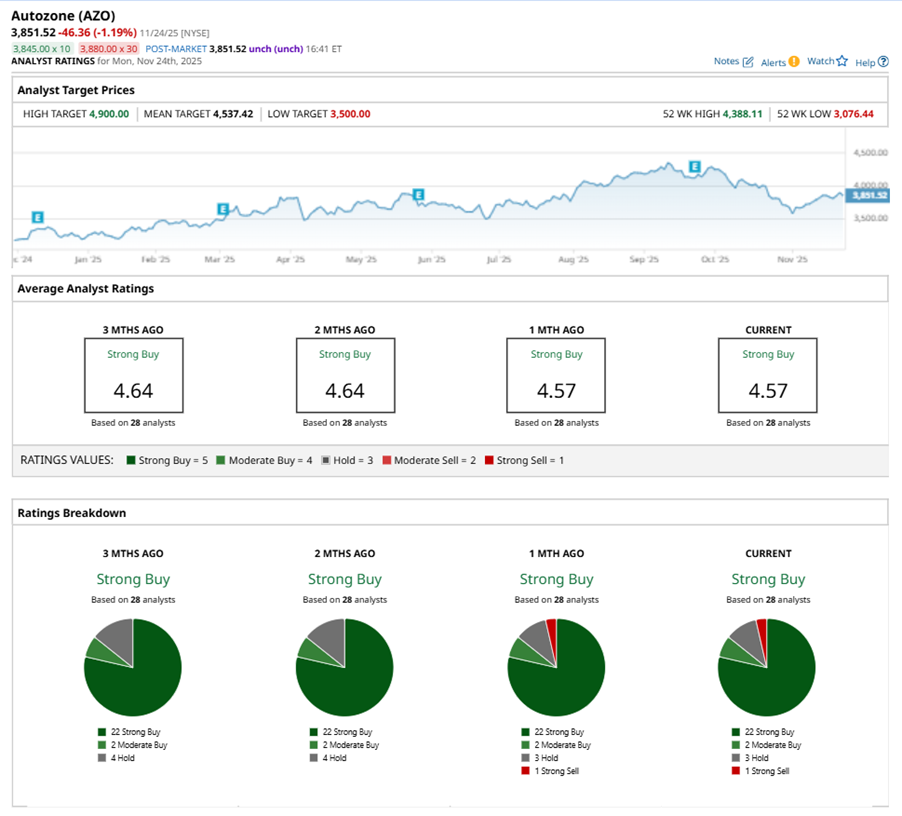

Among the 28 analysts covering AZO stock, the consensus is a “Strong Buy.” That’s based on 22 “Strong Buy” ratings, two “Moderate Buys,” three “Holds,” and one “Strong Sell.”

This configuration is more bearish than two months ago, with no analyst suggesting a “Strong Sell.”

On Nov. 18, Evercore ISI analyst Greg Melich maintained a “Buy” rating on AZO and set a price target of $4,400, implying a potential upside of 14.2% from current levels.

The mean price target of $4,537.42 represents a 17.8% premium to AZO’s current price levels. The Street-high price target of $4,900 suggests a notable upside potential of 27.2%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart