The Sherwin-Williams Company (SHW), based in Cleveland, Ohio, develops, manufactures, and sells paints, coatings, and related products. With a market capitalization of around $83.8 billion, its product lines include architectural paints, industrial coatings, automobile refinishing, wood finishes, aerosols, adhesives, and more.

Companies worth $10 billion or more are generally referred to as "large-cap" companies, and Sherwin-Williams' market cap positions it squarely in the "large-cap" category, emphasizing its significant size, operational stability, and impact in the Basic Materials sector.

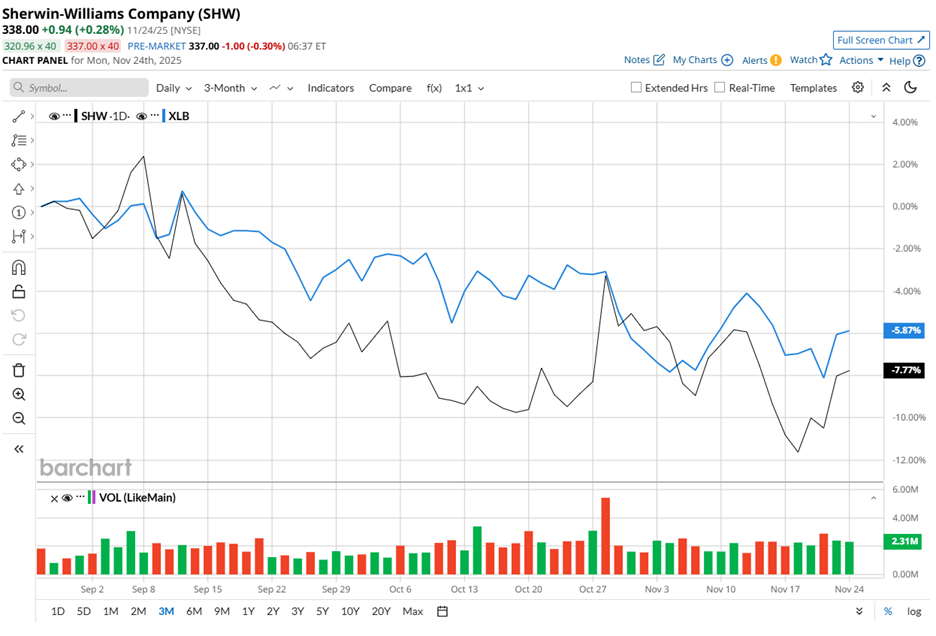

Still, even giants can slip on wet paint. Sherwin-Williams Company’s shares are trading about 15.6% below the November 2024 high of $400.42. The stock has dropped nearly 8% over the past three months, but that’s a deeper pullback than the 5.1% plunge of the S&P 500 Materials Sector SPDR (XLB).

The longer view does not significantly brighten the canvas. SHW stock has experienced a slight year-to-date (YTD) fall and is still down 15.7% over the past 52 weeks. In contrast, XLB is up 3.4% in 2025 but has dropped 8.5% over the same 52-week period, indicating that sector recovery has not lifted every boat.

Plus, SHW stock has been trading below its 50-day and 200-day moving averages since mid-October. Recent rallies crested near each average but failed to break above, signaling persistent downside pressure.

But not all hope is lost. On Oct. 28, SHW jumped 5.5% intraday as investors digested its fiscal 2025 third-quarter results. Revenue rose 3.2% year over year (YoY) to $6.36 billion, beating the estimate. Adjusted EPS grew 6.5% from the prior year’s period to $3.59, clearing the Street’s $3.46 forecast.

Strong cash generation added weight to the momentum. The company produced $2.36 billion in net operating cash and returned $2.13 billion to shareholders through dividends and the repurchase of 4.5 million shares in the first nine months of 2025.

Looking ahead, for the full fiscal year 2025, the company anticipates consolidated net sales to be up in the low single digits compared to full-year 2024. Meanwhile, adjusted EPS is forecasted in the band of $11.25 to $11.45 for the full year.

On the competitive front, the numbers show where the pressure comes from. Rival Ecolab Inc. (ECL) delivered a 9.6% gain over the past 52 weeks and a 14.7% return year-to-date.

Even so, Wall Street is not walking away from the stock. SHW carries a “Moderate Buy” consensus rating from 26 analysts, and the mean price target of $392.67 sits at a premium of 16.2% to current levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart