BridgeBio Pharma (BBIO), a mid-cap biotech company, has investors thrilled with its commercial engine scaling following the approval of Acoramidis (brand name Attruby), a therapy for a serious heart condition called transthyretin amyloid cardiomyopathy (ATTR-CM). Additionally, the company is getting ready to introduce potentially three new products in 2026, pending approval.

While BBIO stock is up more than 150% year to date, outpacing the S&P 500 Index ($SPX) gain of 15%, Wall Street sees more upside and has rated the stock a “Strong Buy.”

For investors looking for a fast-growing biotech with real revenue and multiple upcoming catalysts, BridgeBio is suddenly front and center. Let’s find out if it is the right time to grab this biotech stock.

A Breakout Quarter Powered by Attruby’s Commercial Momentum

BridgeBio’s new drug Attruby, which treats a dangerous heart condition called ATTR-CM, is off to a blockbuster start. In the second quarter, the company reported $110.6 million in Q2 revenue, a dramatic jump from just $2.2 million a year earlier. The surge was fueled primarily by $71.5 million in U.S. net sales of Attruby. While its commercial launch has only just begun, demand is clearly strong. Doctors have already written 3,751 prescriptions through Aug. 1, and more than 1,000 prescribers have adopted the drug. Additionally, demand is increasing month over month, particularly among individuals who have never had treatment.

Additionally, Attruby is not only selling well, but also showing significant patient benefits. Three points were brought to light by a recent analysis of the ATTRibute-CM study:

- For some genetic ATTR-CM patients, the chance of mortality or serious cardiac issues is reduced by 59%.

- After beginning the therapy, patients who rapidly raise their TTR levels have significantly higher survival rates.

- Fewer hospitalizations and fewer new cases of heart rhythm problems.

This strengthens the claim that Attruby could become the best treatment available for years to come.

2026 Could Be a Game Changer

Over the next six to 12 months, BridgeBio will release findings from three major late-stage programs, and any of them might open up a whole new market:

- BBP-418 (Muscular dystrophy), by fall 2025, which could become the first-ever approved treatment for LGMD2I/R9.

- Encaleret (ADH1), by fall 2025, which targets a rare calcium disorder with no approved drug.

- Infigratinib (Achondroplasia), in early 2026, has the potential to become the first oral therapy for the most common form of dwarfism.

If even one of these succeeds, BridgeBio’s value could jump. If two or all three succeed, the company could enter a multi-product growth era.

In the quarter, operating expenses went up because the company is investing heavily in the commercial launch. This resulted in a net loss of $181.9 million in the quarter. While the company has a blockbuster product in the market, it could take a while before revenue translates into profit. Nevertheless, with $756.9 million in cash and investments at the end of the quarter, the company is financially sound. BridgeBio believes this cash balance is enough to continue the Attruby launch, complete all upcoming Phase 3 trials, and prepare for new product launches. The company also raised money through note issuances and royalty deals, giving it flexibility without immediately needing to dilute shareholders. Analysts who cover the stock expect revenue to increase by 122% in 2025 to $493.4 million before rising another 74% in 2026.

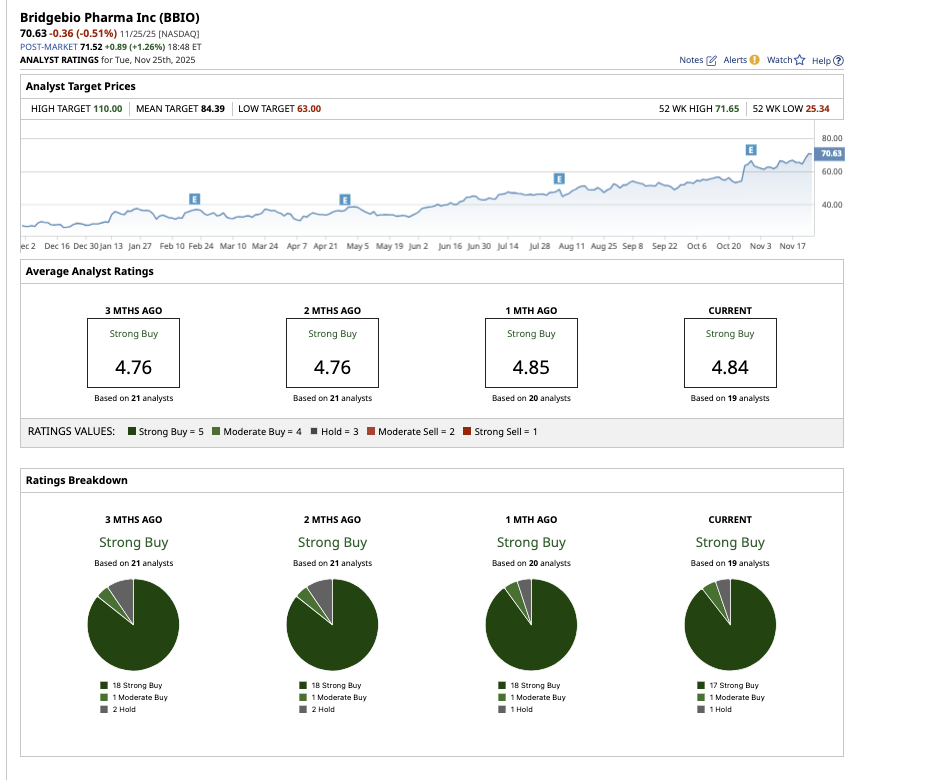

What Is the Target Price for BBIO Stock?

Overall, on Wall Street, BridgeBio Pharma stock is a “Strong Buy.” Out of 19 analysts covering the stock, 17 have a “Strong Buy” rating, one rates it a “Moderate Buy,” and one rates it a “Hold.” The average target price of $84.39 suggests the stock has upside potential of 20% above current levels. Plus, the high price estimate of $110 implies the stock can rally as much as 56% over the next 12 months.

Why Wall Street Sees Potential

Wall Street’s optimistic view of the stock could be because of three factors. First, Attruby’s rapid growth proves demand is strong for its first commercial drug. Second, upcoming trial results could significantly increase the company’s value. Finally, the company is financially strong and well-positioned. Analysts believe the market still hasn’t priced in the potential of these pipeline programs.

BridgeBio is positioning itself to become a major rare-disease drug company, with multiple long-term revenue streams. Before the company steps into a much larger league, it could be a great biotech stock to add to a diversified long-term portfolio.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart