Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Stitch Fix (NASDAQ:SFIX) and its peers.

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

The 17 apparel and accessories stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 2.9% while next quarter’s revenue guidance was 12.9% below.

In light of this news, share prices of the companies have held steady as they are up 4.8% on average since the latest earnings results.

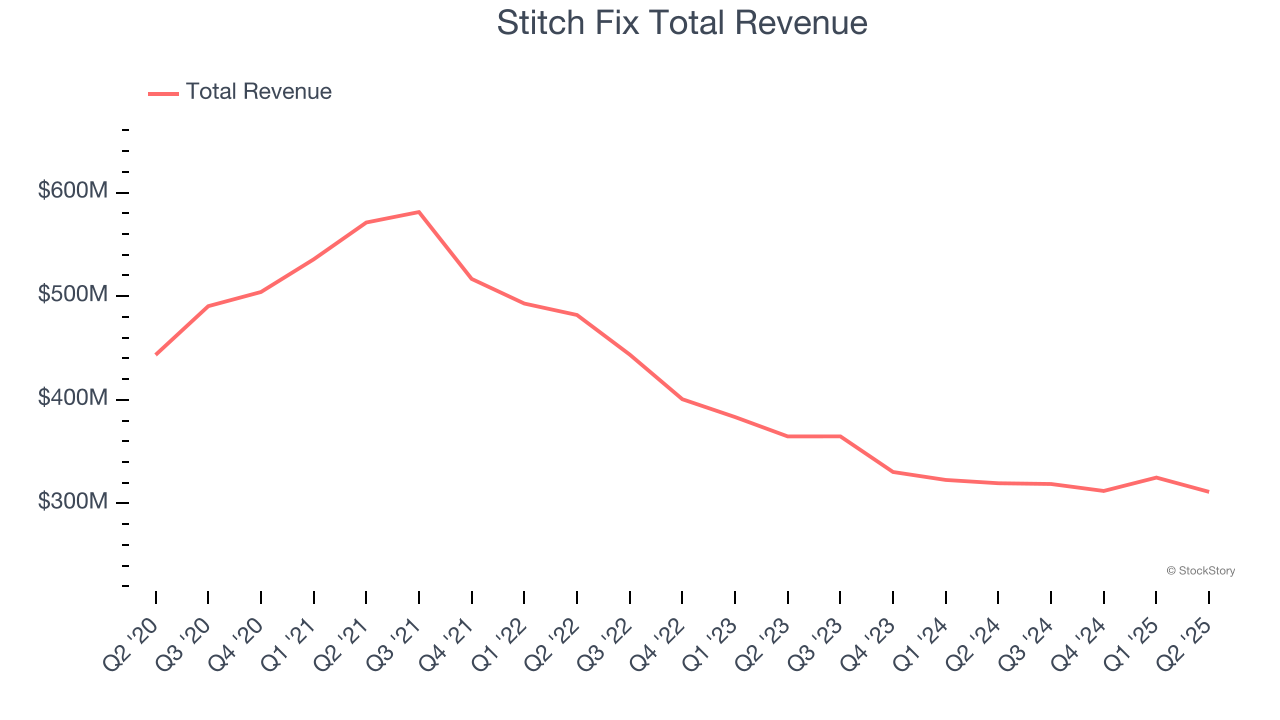

Stitch Fix (NASDAQ:SFIX)

One of the original subscription box companies, Stitch Fix (NASDAQ:SFIX) is an online personal styling and fashion service that curates personalized clothing selections for customers.

Stitch Fix reported revenues of $311.2 million, down 2.6% year on year. This print exceeded analysts’ expectations by 2.4%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates and revenue guidance for next quarter exceeding analysts’ expectations.

“Fiscal 2025 was a milestone year for Stitch Fix. We finished the year with our second consecutive quarter of year-over-year revenue growth on an adjusted basis, and once again gained share in the US apparel market,” said Matt Baer, CEO, Stitch Fix.

Stitch Fix scored the highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 20.4% since reporting and currently trades at $4.49.

Is now the time to buy Stitch Fix? Access our full analysis of the earnings results here, it’s free for active Edge members.

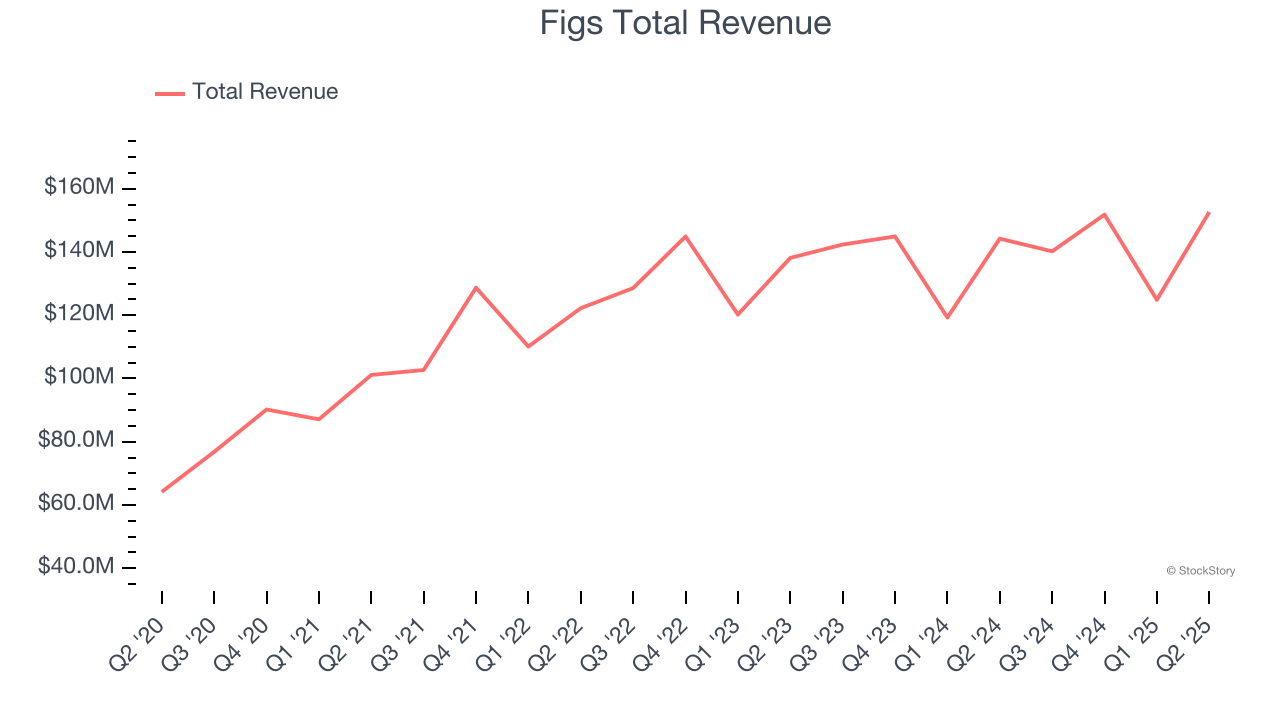

Best Q2: Figs (NYSE:FIGS)

Rising to fame via TikTok and founded in 2013 by Heather Hasson and Trina Spear, Figs (NYSE:FIGS) is a healthcare apparel company known for its stylish approach to medical attire and uniforms.

Figs reported revenues of $152.6 million, up 5.8% year on year, outperforming analysts’ expectations by 5.5%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 22% since reporting. It currently trades at $8.00.

Is now the time to buy Figs? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Carter's (NYSE:CRI)

Rumored to sell more than 10 products for every child born in the United States, Carter's (NYSE:CRI) is an American designer and marketer of children's apparel.

Carter's reported revenues of $585.3 million, up 3.7% year on year, exceeding analysts’ expectations by 3.4%. Still, it was a softer quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 9.4% since the results and currently trades at $29.66.

Read our full analysis of Carter’s results here.

Oxford Industries (NYSE:OXM)

The parent company of Tommy Bahama, Oxford Industries (NYSE:OXM) is a lifestyle fashion conglomerate with brands that embody outdoor happiness.

Oxford Industries reported revenues of $403.1 million, down 4% year on year. This result missed analysts’ expectations by 0.7%. Aside from that, it was a mixed quarter as it also produced full-year EPS guidance beating analysts’ expectations but EPS guidance for next quarter missing analysts’ expectations significantly.

Oxford Industries had the weakest performance against analyst estimates among its peers. The stock is down 5.5% since reporting and currently trades at $38.21.

Read our full, actionable report on Oxford Industries here, it’s free for active Edge members.

Hanesbrands (NYSE:HBI)

A classic American staple founded in 1901, Hanesbrands (NYSE: HBI) is a clothing company known for its array of basic apparel including innerwear and activewear.

Hanesbrands reported revenues of $991.3 million, up 1.8% year on year. This print beat analysts’ expectations by 1.9%. Overall, it was a very strong quarter as it also logged an impressive beat of analysts’ constant currency revenue estimates and EPS guidance for next quarter exceeding analysts’ expectations.

The stock is up 64% since reporting and currently trades at $6.84.

Read our full, actionable report on Hanesbrands here, it’s free for active Edge members.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.