Even though Fifth Third Bancorp (currently trading at $42.58 per share) has gained 7.8% over the last six months, it has lagged the S&P 500’s 13% return during that period. This might have investors contemplating their next move.

Does this present a buying opportunity for FITB? Or does the price properly account for its business quality and fundamentals?

Why Does Fifth Third Bancorp Spark Debate?

Named after the merger of Third National Bank and Fifth National Bank in 1908, Fifth Third Bancorp (NASDAQ:FITB) is a financial services company that provides banking, lending, wealth management, and investment services to individuals and businesses across the Midwest and Southeast.

Two Things to Like:

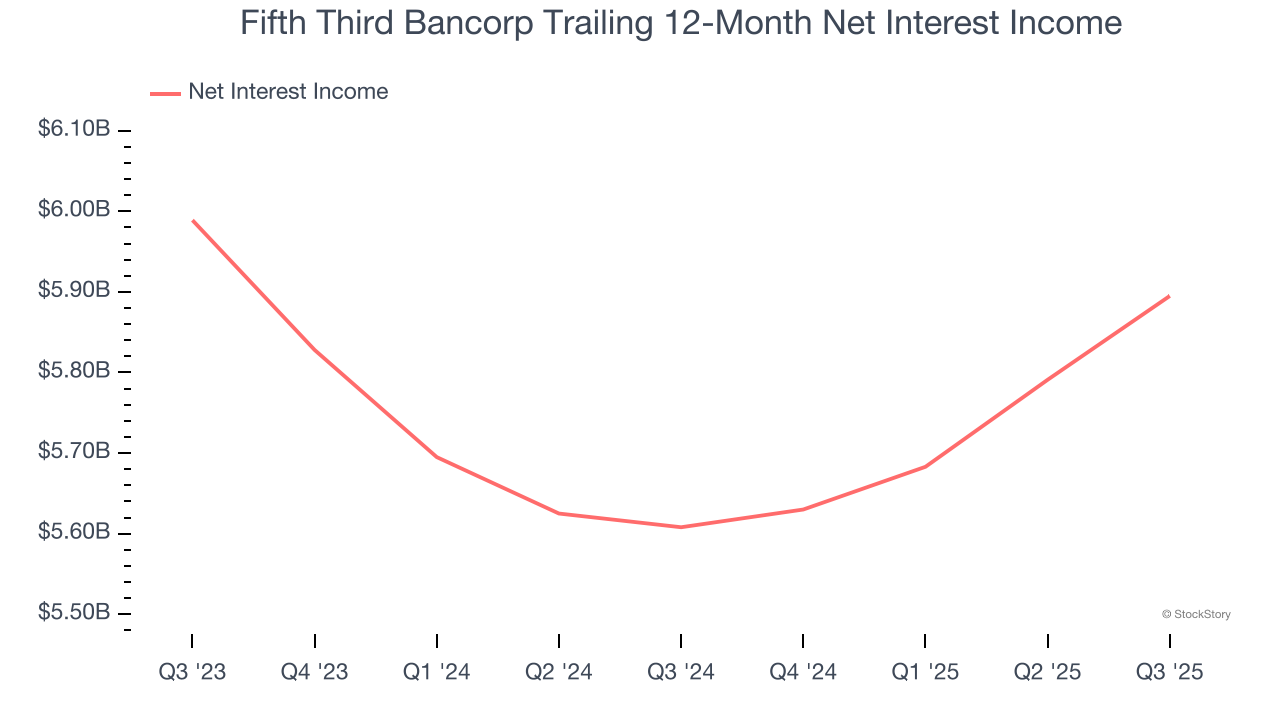

1. Projected Net Interest Income Growth Is Remarkable

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Fifth Third Bancorp’s net interest income to rise by 27.8%, an improvement versus its flat result for the past two years.

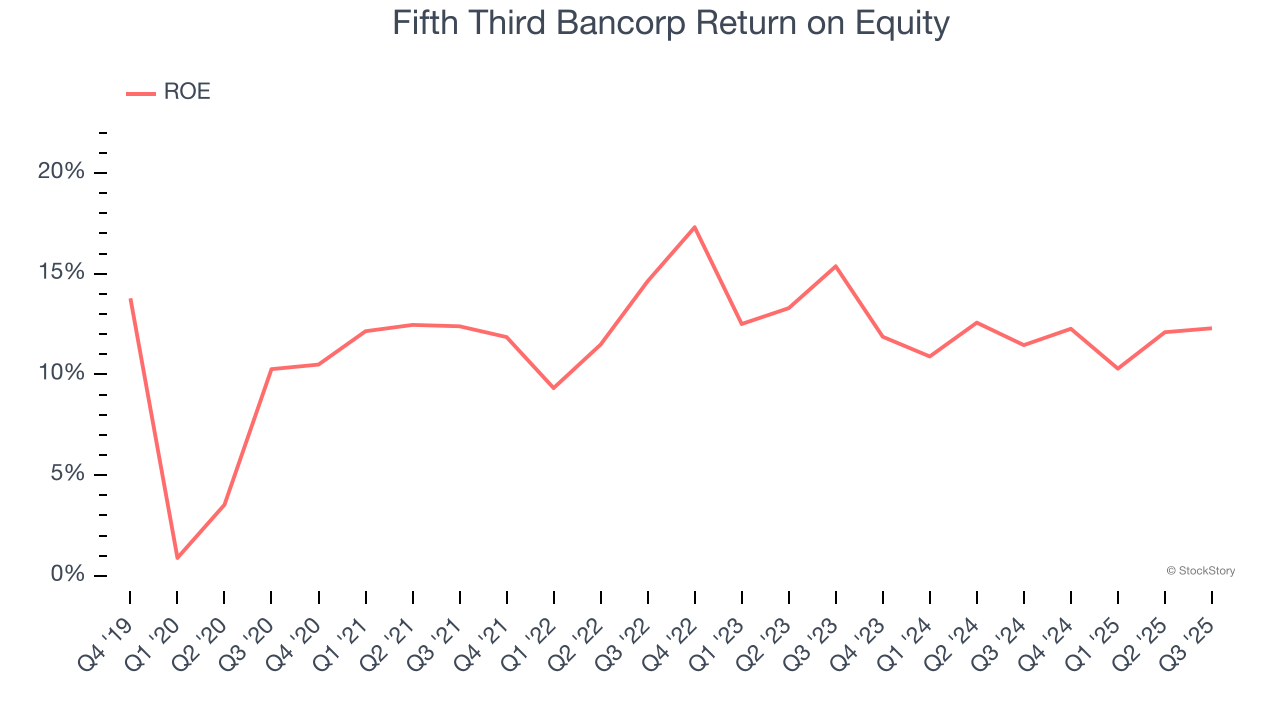

2. Stellar ROE Showcases Lucrative Growth Opportunities

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Fifth Third Bancorp has averaged an ROE of 12.4%, excellent for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows Fifth Third Bancorp has a strong competitive moat.

One Reason to be Careful:

Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

Fifth Third Bancorp’s net interest income has grown at a 4.1% annualized rate over the last five years, worse than the broader banking industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

Final Judgment

Fifth Third Bancorp has huge potential even though it has some open questions. With its shares lagging the market recently, the stock trades at 1.4× forward P/B (or $42.58 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

Stocks We Like Even More Than Fifth Third Bancorp

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.