Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Kemper (NYSE:KMPR) and the best and worst performers in the insurance industry.

The insurance industry absorbs and diversifies risk, providing financial protection against unforeseen life, health, property, and liability events. Profits come from underwriting—collecting more in premiums than paid in claims—and investing the 'float'. This cyclical industry benefits from 'hard markets' with strong pricing power and higher interest rates that enhance investment income. AI adoption is improving underwriting through sophisticated data analysis and reducing costs via automation. However, 'soft markets' and low rates create headwinds, while the industry faces elevated claims costs from climate catastrophes, inflation, and rising litigation expenses.

The 57 insurance stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 3.8%.

In light of this news, share prices of the companies have held steady as they are up 3.5% on average since the latest earnings results.

Kemper (NYSE:KMPR)

Originally known as Unitrin until rebranding in 2011, Kemper (NYSE:KMPR) is an insurance holding company that provides automobile, homeowners, life, and other insurance products to individuals and businesses across the United States.

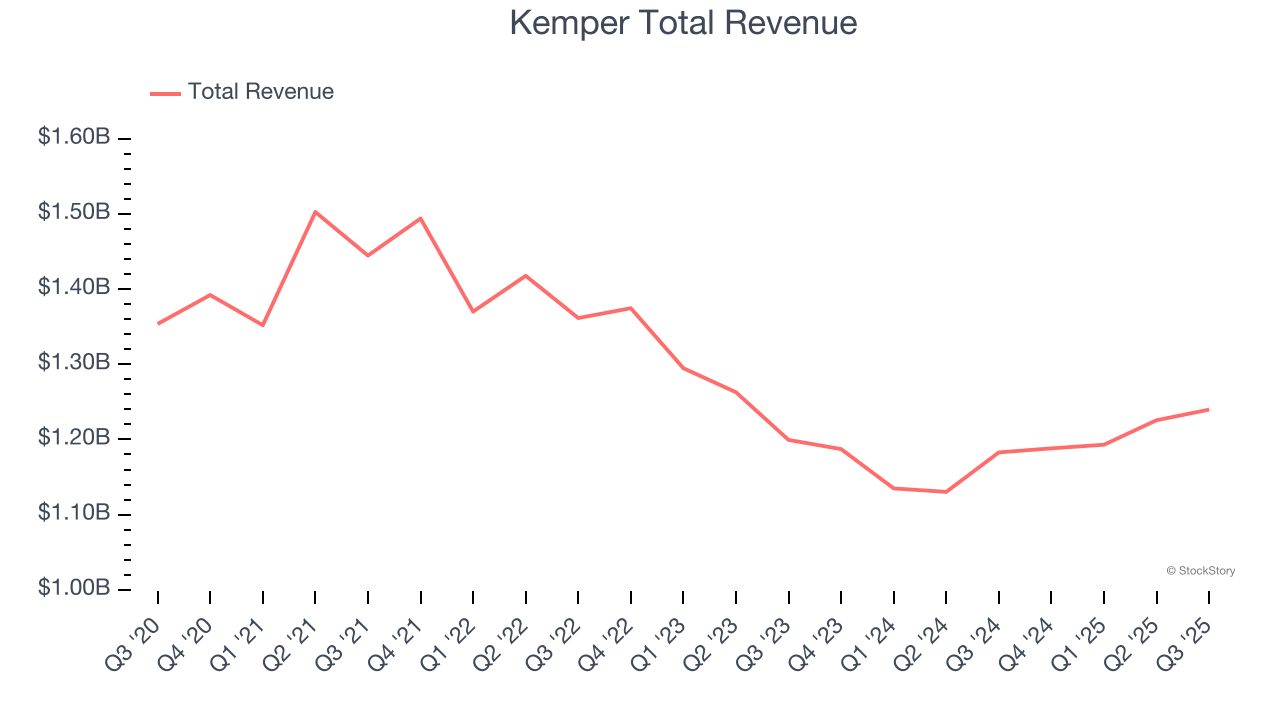

Kemper reported revenues of $1.24 billion, up 4.8% year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a softer quarter for the company with a significant miss of analysts’ EPS estimates and a significant miss of analysts’ book value per share estimates.

“Our results for the quarter were disappointing and below our expectations,” said C. Thomas Evans, Jr., Interim CEO.

Unsurprisingly, the stock is down 4.5% since reporting and currently trades at $40.71.

Read our full report on Kemper here, it’s free for active Edge members.

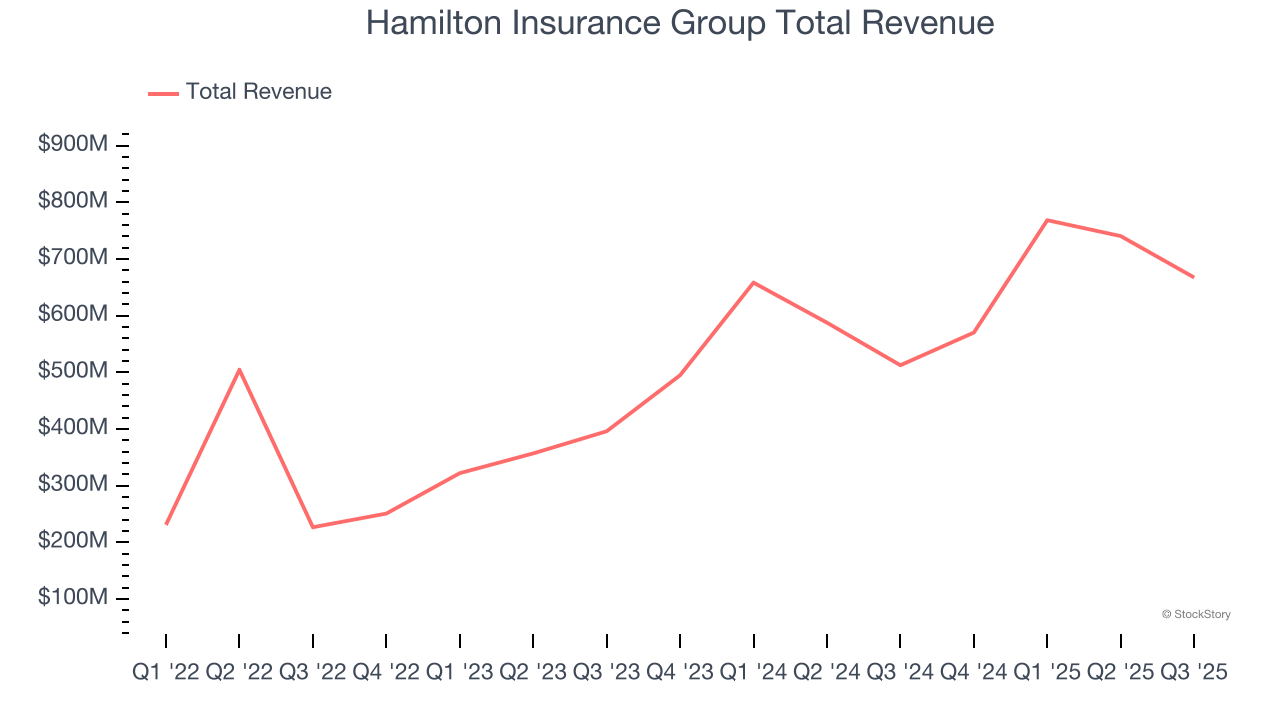

Best Q3: Hamilton Insurance Group (NYSE:HG)

Founded in 2013 and operating through three distinct underwriting platforms across four countries, Hamilton Insurance Group (NYSE:HG) operates global specialty insurance and reinsurance platforms across Lloyd's, Ireland, Bermuda, and the United States.

Hamilton Insurance Group reported revenues of $667.7 million, up 30.2% year on year, outperforming analysts’ expectations by 10.3%. The business had an incredible quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 18.2% since reporting. It currently trades at $27.88.

Is now the time to buy Hamilton Insurance Group? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Brighthouse Financial (NASDAQ:BHF)

Spun off from MetLife in 2017 to focus specifically on retail financial products, Brighthouse Financial (NASDAQ:BHF) provides annuity contracts and life insurance products designed to help individuals protect wealth, generate income, and transfer assets.

Brighthouse Financial reported revenues of $2.17 billion, flat year on year, falling short of analysts’ expectations by 4%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and net premiums earned estimates.

The stock is flat since the results and currently trades at $65.41.

Read our full analysis of Brighthouse Financial’s results here.

Root (NASDAQ:ROOT)

Pioneering a data-driven approach that rewards good driving habits, Root (NASDAQ:ROOT) is a technology-driven auto insurance company that uses mobile apps to acquire customers and data science to price policies based on individual driving behavior.

Root reported revenues of $387.8 million, up 26.9% year on year. This print beat analysts’ expectations by 4.5%. It was an incredible quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ net premiums earned estimates.

The stock is down 9.5% since reporting and currently trades at $80.98.

Read our full, actionable report on Root here, it’s free for active Edge members.

Hartford (NYSE:HIG)

Recognizable by its iconic stag logo that dates back to 1810, The Hartford (NYSE:HIG) provides property and casualty insurance, group benefits, and investment products to individuals and businesses across the United States.

Hartford reported revenues of $7.23 billion, up 7.1% year on year. This number topped analysts’ expectations by 1.2%. Overall, it was a strong quarter as it also logged an impressive beat of analysts’ net premiums earned estimates and a beat of analysts’ EPS estimates.

The stock is up 9.7% since reporting and currently trades at $137.05.

Read our full, actionable report on Hartford here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.