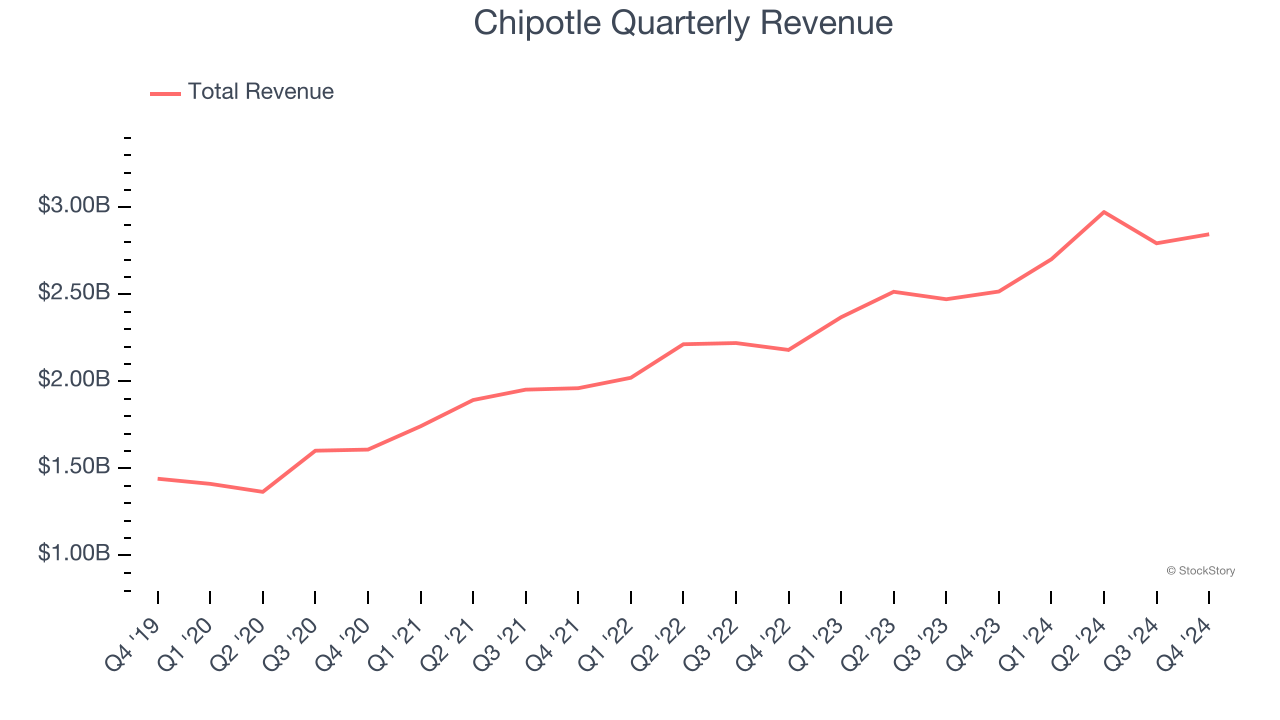

Mexican fast-food chain Chipotle (NYSE:CMG) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 13.1% year on year to $2.85 billion. Its non-GAAP profit of $0.25 per share was in line with analysts’ consensus estimates.

Is now the time to buy Chipotle? Find out by accessing our full research report, it’s free.

Chipotle (CMG) Q4 CY2024 Highlights:

- Revenue: $2.85 billion vs analyst estimates of $2.85 billion (13.1% year-on-year growth, in line)

- Adjusted EPS: $0.25 vs analyst estimates of $0.25 (in line)

- Adjusted EBITDA: $511.6 million vs analyst estimates of $518.3 million (18% margin, 1.3% miss)

- Operating Margin: 14.6%, in line with the same quarter last year

- Free Cash Flow Margin: 12.4%, up from 3.7% in the same quarter last year

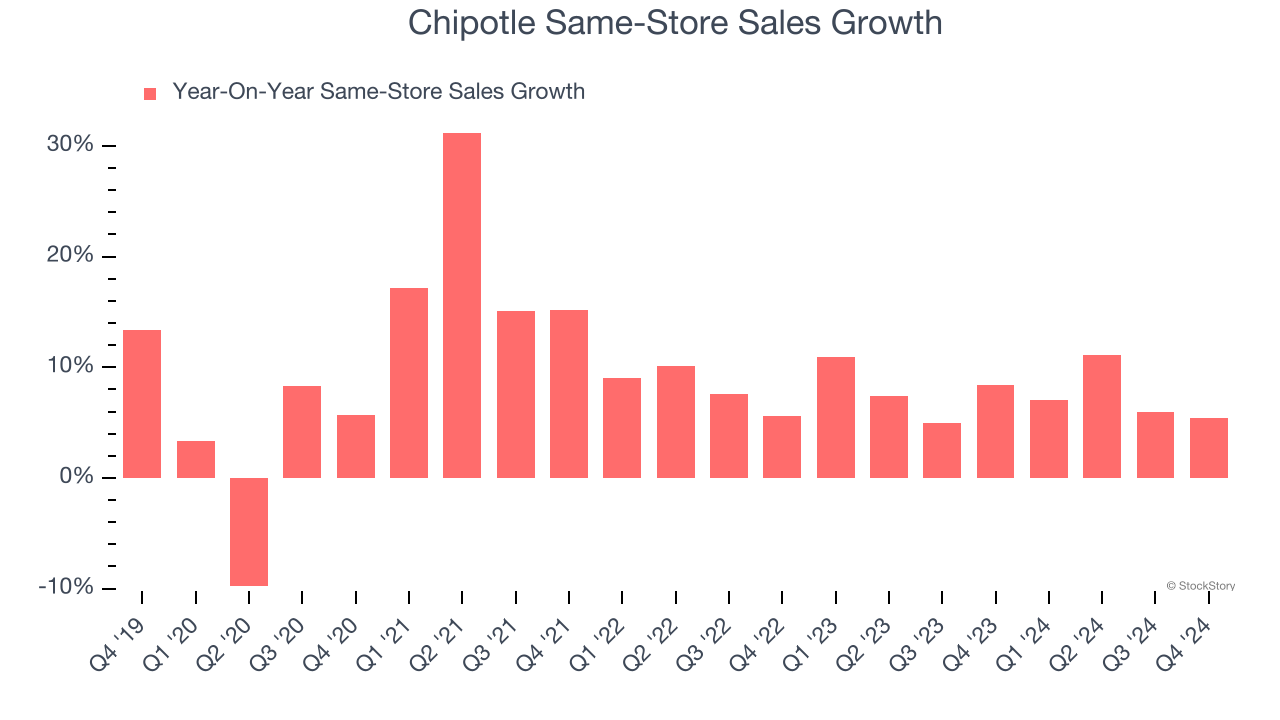

- Same-Store Sales rose 5.4% year on year (8.4% in the same quarter last year)

- Market Capitalization: $79.58 billion

"Chipotle had another outstanding year, delivering strong transaction driven comps each quarter, expanding margins, adding over 300 new restaurants, gaining momentum in key industry leading brand metrics, making progress on many restaurant operating initiatives and building our footprint internationally," said Scott Boatwright, CEO, Chipotle.

Company Overview

Born from a desire to offer quick meals with fresh, flavorful ingredients, Chipotle (NYSE:CMG) is a fast-food chain known for its healthy, Mexican-inspired cuisine and customizable dishes.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years.

With $11.31 billion in revenue over the past 12 months, Chipotle is one of the most widely recognized restaurant chains and benefits from customer loyalty, a luxury many don’t have. Its scale also gives it negotiating leverage with suppliers, enabling it to source its ingredients at a lower cost.

As you can see below, Chipotle’s 15.2% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Chipotle’s year-on-year revenue growth was 13.1%, and its $2.85 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a slight deceleration versus the last five years. We still think its growth trajectory is attractive given its scale and implies the market is baking in success for its menu offerings.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Restaurant Performance

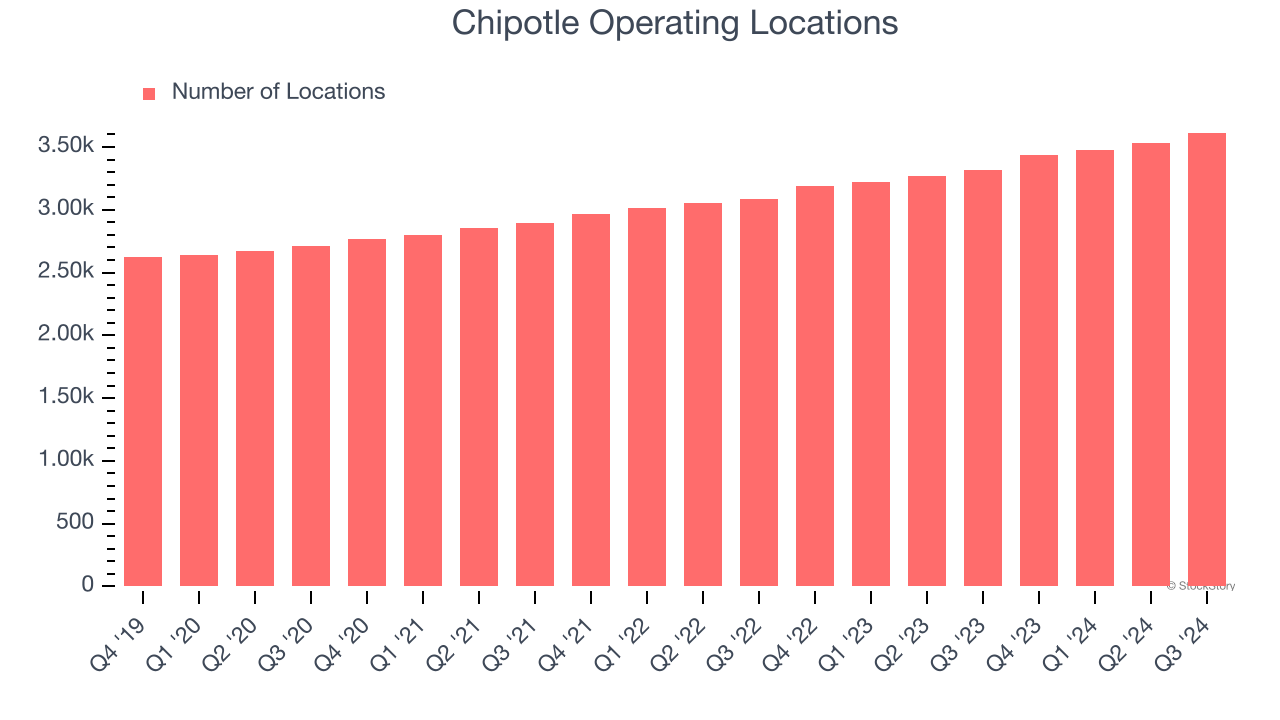

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Chipotle opened new restaurants at a rapid clip over the last two years, averaging 7.7% annual growth, much faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Note that Chipotle reports its restaurant count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Chipotle has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 7.7%. This performance suggests its rollout of new restaurants is beneficial for shareholders. We like this backdrop because it gives Chipotle multiple ways to win: revenue growth can come from new restaurants or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Chipotle’s same-store sales rose 5.4% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Chipotle’s Q4 Results

We struggled to find many positives in these results. Revenue and EPS were just in line, which was not good enough for a stock trading at a premium multiple. The company also has a new CEO after the previous CEO left to take the top job at Starbucks, so there could be some additional worry about how the company may perform under new leadership. The stock traded down 4.5% to $56.38 immediately following the results.

Big picture, is Chipotle a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.