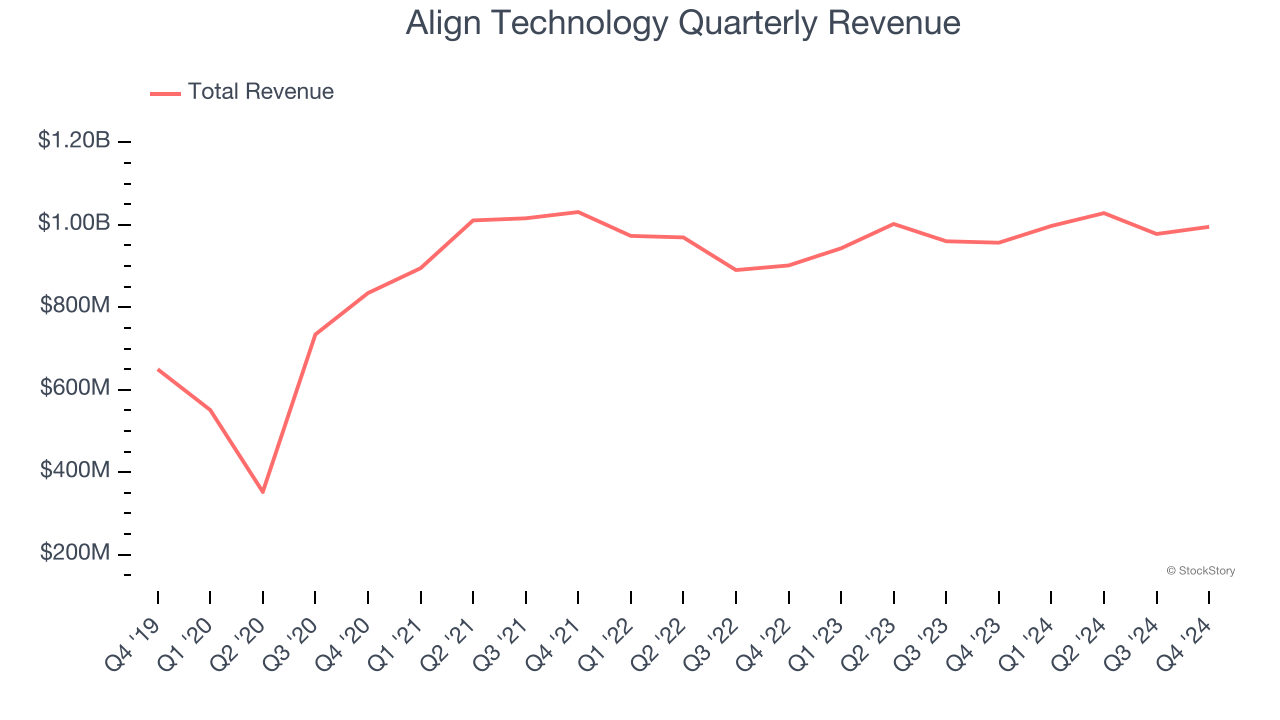

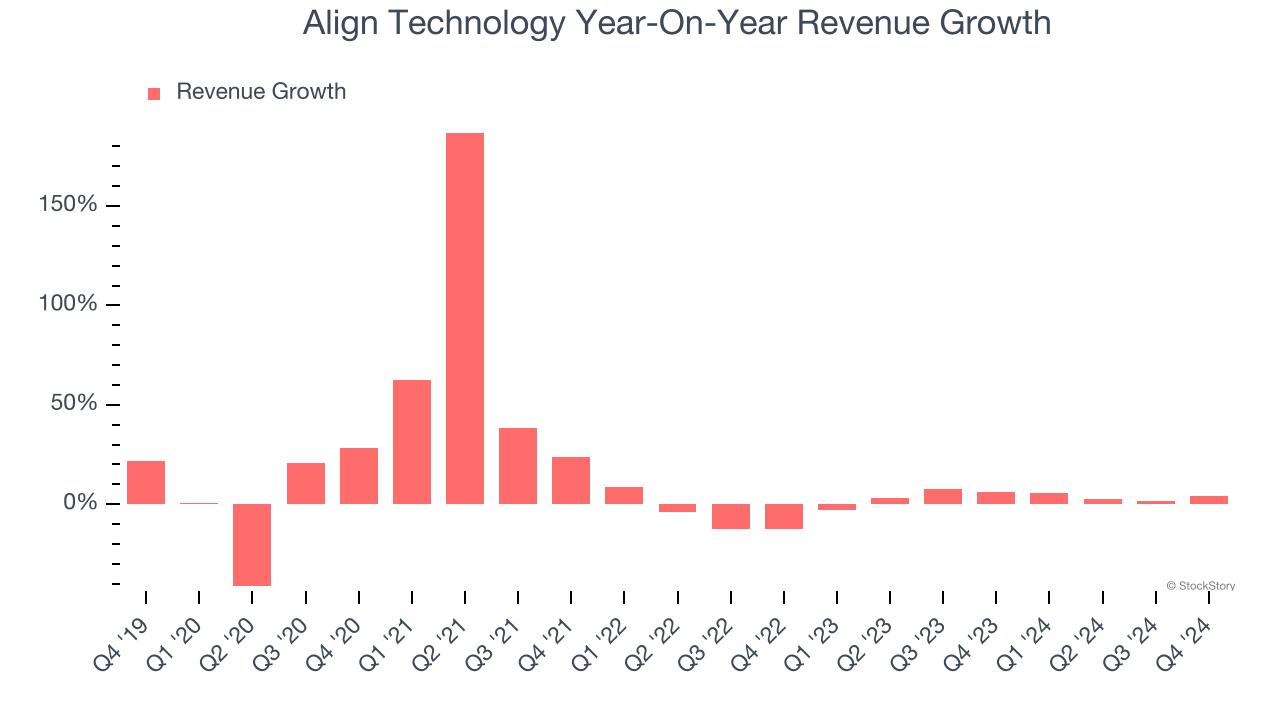

Dental technology company Align Technology (NASDAQ:ALGN) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 4% year on year to $995.2 million. On the other hand, next quarter’s revenue guidance of $975 million was less impressive, coming in 5.5% below analysts’ estimates. Its non-GAAP profit of $2.44 per share was in line with analysts’ consensus estimates.

Is now the time to buy Align Technology? Find out by accessing our full research report, it’s free.

Align Technology (ALGN) Q4 CY2024 Highlights:

- Revenue: $995.2 million vs analyst estimates of $998.3 million (4% year-on-year growth, in line)

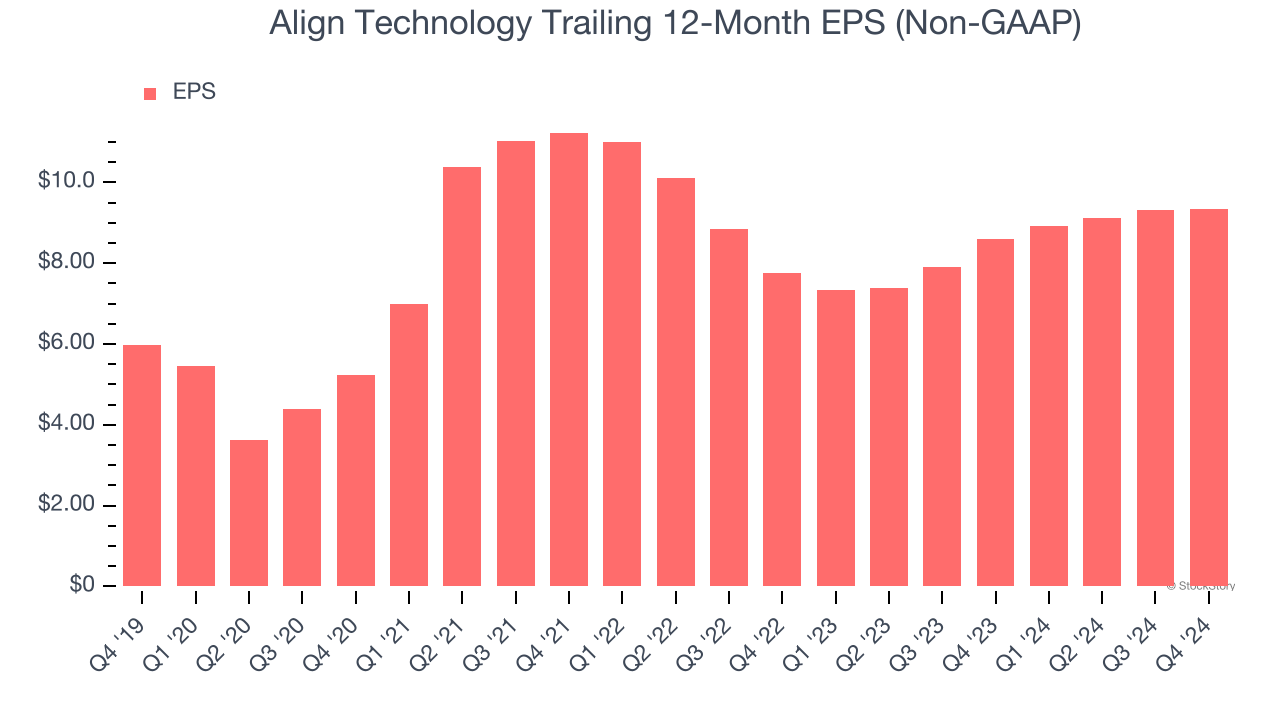

- Adjusted EPS: $2.44 vs analyst estimates of $2.45 (in line)

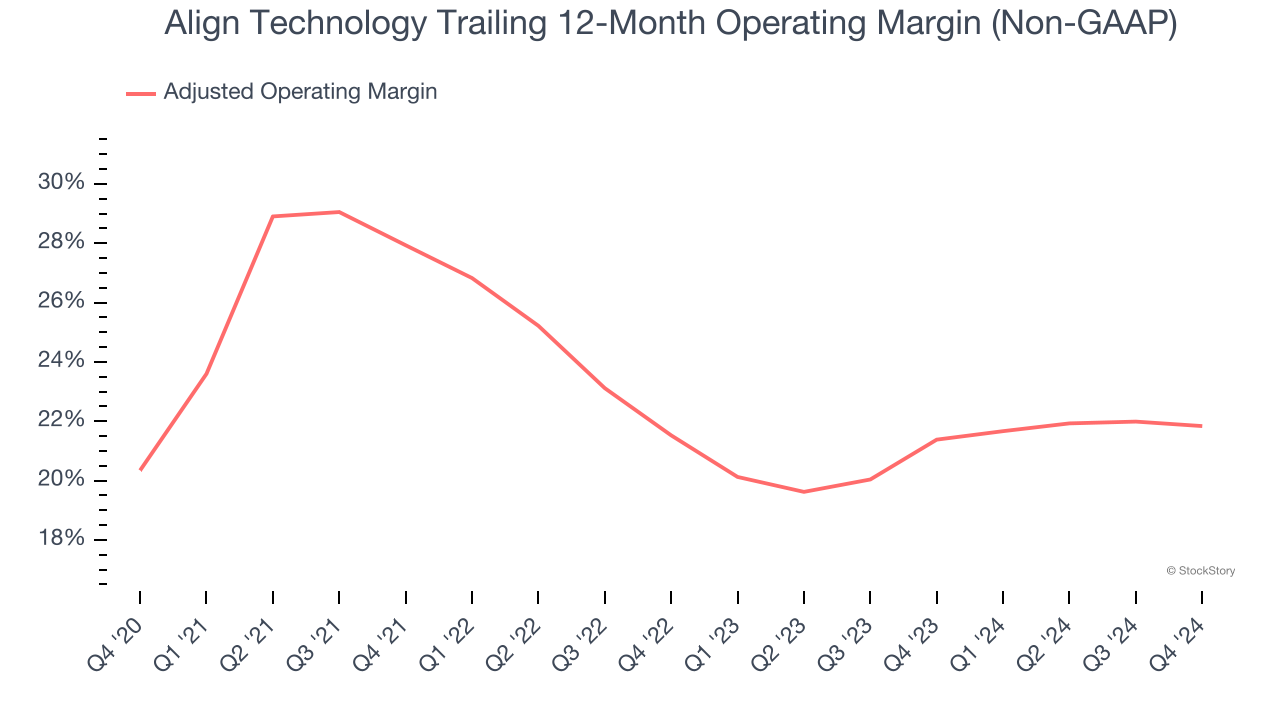

- Adjusted Operating Income: $230.4 million vs analyst estimates of $225.6 million (23.2% margin, 2.1% beat)

- Revenue Guidance for Q1 CY2025 is $975 million at the midpoint, below analyst estimates of $1.03 billion

- Operating Margin: 14.5%, down from 17.9% in the same quarter last year

- Market Capitalization: $16.03 billion

Commenting on Align's Q4'24 and 2024 results, Align Technology President and CEO Joe Hogan said, “I am pleased to report that Q4 total revenues, Clear Aligner volumes, and Systems and Services revenues were in line with our Q4 outlook and both GAAP and non-GAAP operating margins were better than our Q4 outlook. Q4 Clear Aligner ASPs were lower than our Q4 outlook due primarily to the impact from unfavorable foreign exchange from the strengthening U.S. dollar against major currencies from late October through December. On a year-over-year basis, fourth quarter revenues of $995.2 million increased 4.0%, reflecting 14.9% growth from Systems and Services revenues and 1.6% growth from Clear Aligner revenues. On a year-over-year basis, Clear Aligner volumes grew 6.1%, driven by increased shipments across all regions—with strength in the EMEA, APAC, and LATAM regions, and stability in North America. From a channel perspective, Clear Aligner volumes in the ortho and general practitioner dentist (“GP”) channels were up on a year-over-year basis with the number of submitters and utilization amongst the highest in the past few years.

Company Overview

Founded in 1997, Align Technology (NASDAQ:ALGN) specializes in clear aligner therapy and digital dental solutions, offering products like the Invisalign system for teeth straightening and iTero scanners for precise digital imaging.

Dental Equipment & Technology

The dental equipment and technology industry encompasses companies that manufacture orthodontic products, dental implants, imaging systems, and digital tools for dental professionals. These companies benefit from recurring revenue streams tied to consumables, ongoing maintenance, and growing demand for aesthetic and restorative dentistry. However, high R&D costs, significant capital investment requirements, and reliance on discretionary spending make them vulnerable to economic cycles. Over the next few years, tailwinds for the sector include innovation in digital workflows, such as 3D printing and AI-driven diagnostics, which enhance the efficiency and precision of dental care. However, headwinds include economic uncertainty, which could reduce patient spending on elective procedures, regulatory challenges, and potential pricing pressures from consolidated dental service organizations (DSOs).

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Align Technology’s 10.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Align Technology’s recent history shows its demand slowed as its annualized revenue growth of 3.5% over the last two years is below its five-year trend.

This quarter, Align Technology grew its revenue by 4% year on year, and its $995.2 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 2.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.1% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and suggests its newer products and services will spur better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Align Technology has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 22.8%.

Analyzing the trend in its profitability, Align Technology’s adjusted operating margin rose by 1.5 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its past improvements as the company’s margin was relatively unchanged on two-year basis.

This quarter, Align Technology generated an adjusted operating profit margin of 23.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Align Technology’s EPS grew at a remarkable 9.3% compounded annual growth rate over the last five years. Despite its adjusted operating margin expansion and share repurchases during that time, this performance was lower than its 10.7% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q4, Align Technology reported EPS at $2.44, up from $2.42 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Align Technology’s full-year EPS of $9.34 to grow 8.5%.

Key Takeaways from Align Technology’s Q4 Results

We struggled to find many positives in these results, and its revenue guidance for next quarter significantly missed Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.1% to $201 immediately following the results.

Align Technology’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.