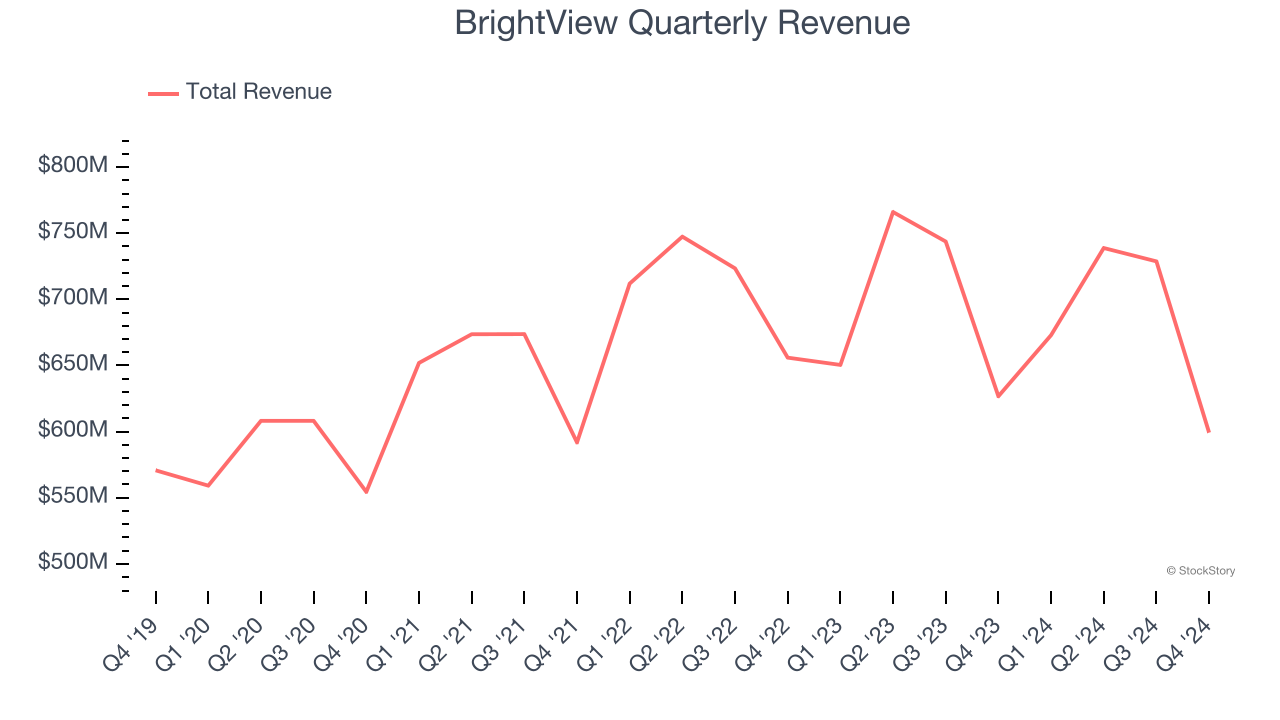

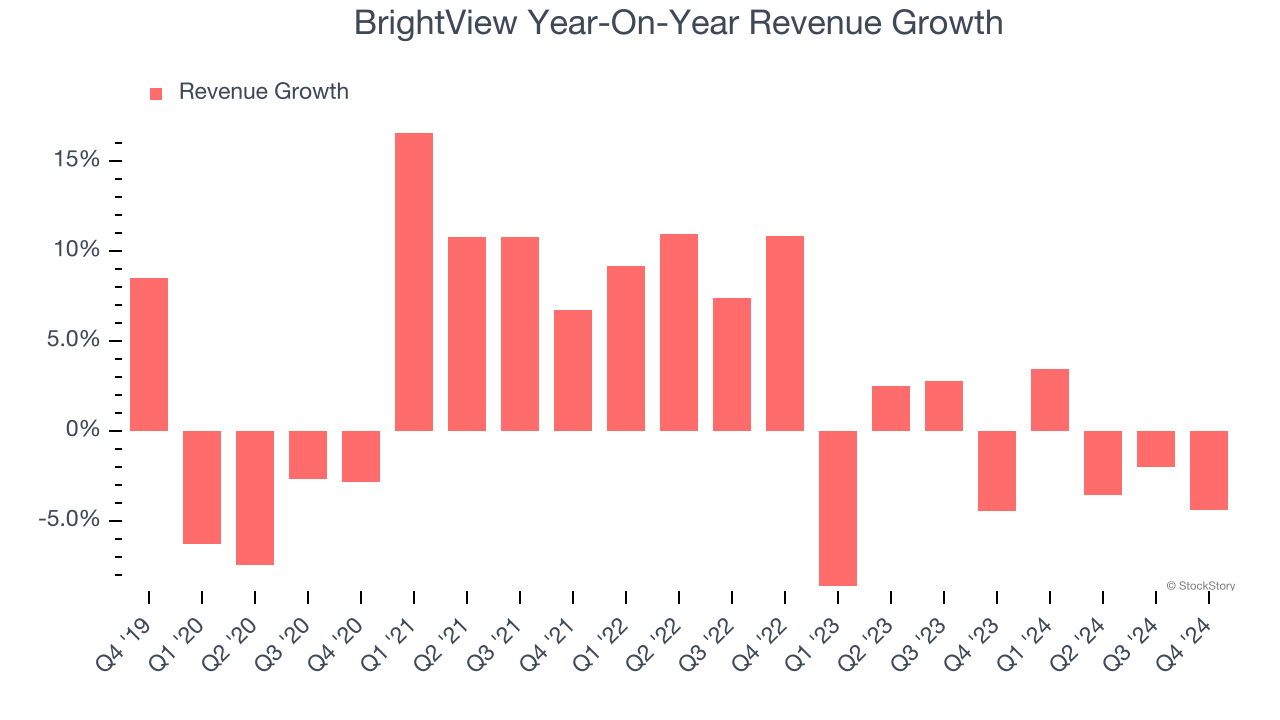

Landscaping service company BrightView (NYSE:BV) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 4.4% year on year to $599.2 million. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $2.8 billion at the midpoint. Its non-GAAP profit of $0.04 per share was in line with analysts’ consensus estimates.

Is now the time to buy BrightView? Find out by accessing our full research report, it’s free.

BrightView (BV) Q4 CY2024 Highlights:

- Revenue: $599.2 million vs analyst estimates of $615.7 million (4.4% year-on-year decline, 2.7% miss)

- Adjusted EPS: $0.04 vs analyst estimates of $0.04 (in line)

- Adjusted EBITDA: $52.1 million vs analyst estimates of $49.1 million (8.7% margin, 6.1% beat)

- The company reconfirmed its revenue guidance for the full year of $2.8 billion at the midpoint

- EBITDA guidance for the full year is $345 million at the midpoint, in line with analyst expectations

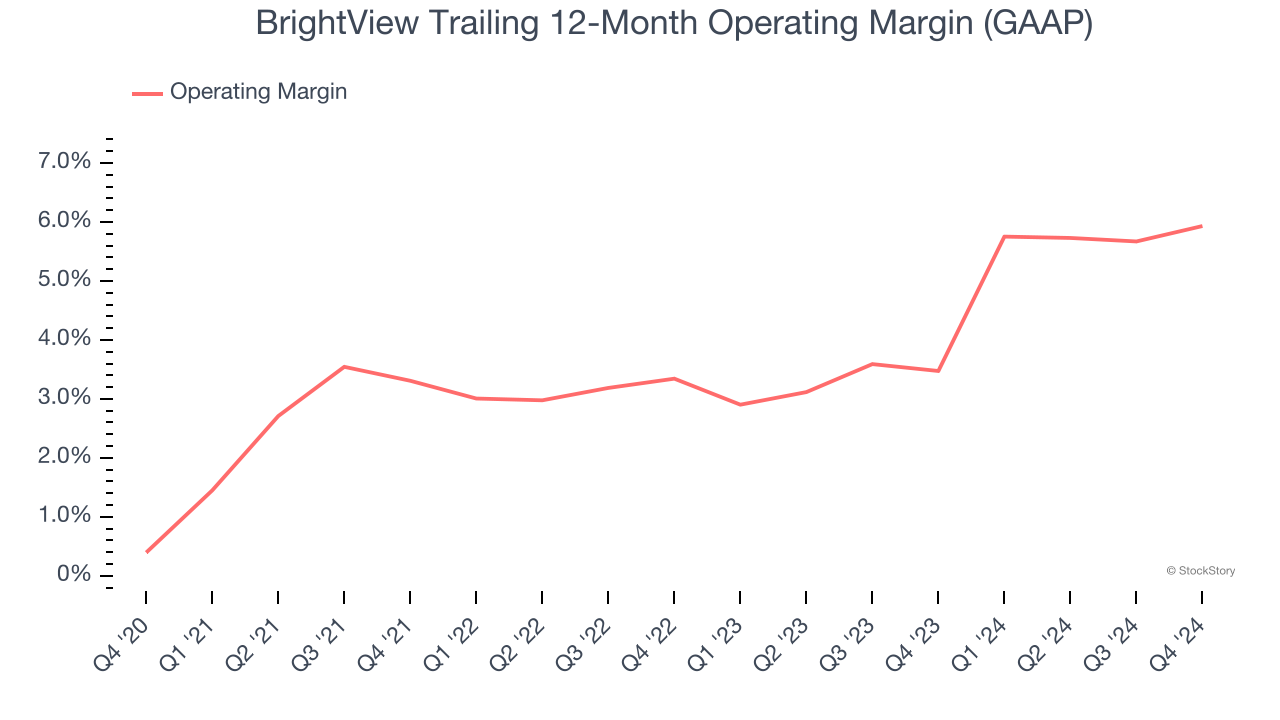

- Operating Margin: -0.1%, in line with the same quarter last year

- Free Cash Flow Margin: 0.3%, down from 2.8% in the same quarter last year

- Market Capitalization: $1.54 billion

"We are off to a strong start to the fiscal year, fueled by the growing momentum of our evolving One BrightView culture,” said BrightView President and Chief Executive Officer Dale Asplund.

Company Overview

An official field consultant for Major League Baseball, BrightView (NYSE:BV) offers landscaping design, development, and maintenance.

Facility Services

Many facility services are non-discretionary (office building bathrooms need to be cleaned), recurring, and performed through contracts. This makes for more predictable and stickier revenue streams. However, COVID changed the game regarding commercial real estate, and office vacancies remain high as hybrid work seems here to stay. This is a headwind for demand, and facility services companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact commercial construction projects that drive incremental demand for these companies’ services.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, BrightView grew its sales at a sluggish 2.3% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. BrightView’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.

This quarter, BrightView missed Wall Street’s estimates and reported a rather uninspiring 4.4% year-on-year revenue decline, generating $599.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

BrightView was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, BrightView’s operating margin rose by 5.5 percentage points over the last five years.

In Q4, BrightView’s breakeven margin was in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

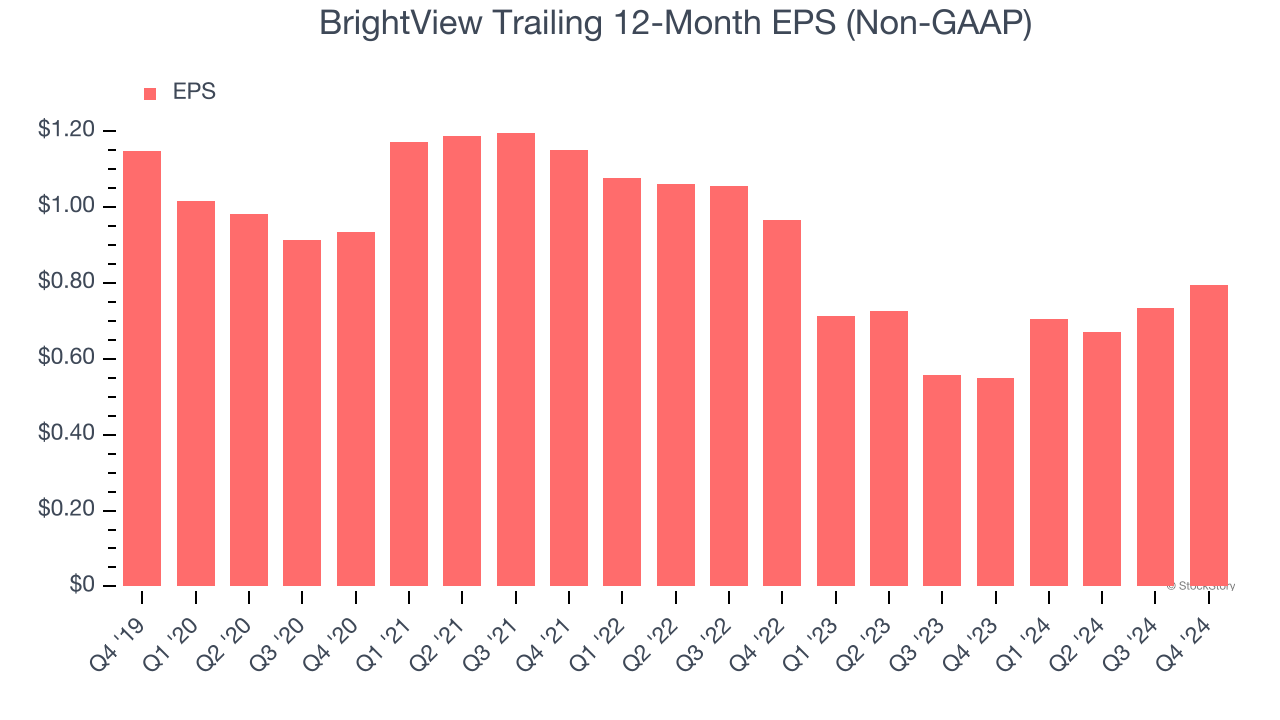

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for BrightView, its EPS declined by 7.1% annually over the last five years while its revenue grew by 2.3%. However, its operating margin actually expanded during this time and it repurchased its shares, telling us the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

BrightView’s two-year annual EPS declines of 9.3% were bad and lower than its two-year revenue performance.

In Q4, BrightView reported EPS at $0.04, up from negative $0.02 in the same quarter last year. This print beat analysts’ estimates by 7%. Over the next 12 months, Wall Street expects BrightView’s full-year EPS of $0.80 to grow 11.6%.

Key Takeaways from BrightView’s Q4 Results

We enjoyed seeing BrightView exceed analysts’ EBITDA expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed significantly. Zooming out, we think this was a mixed quarter. The stock remained flat at $16.10 immediately after reporting.

Big picture, is BrightView a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.