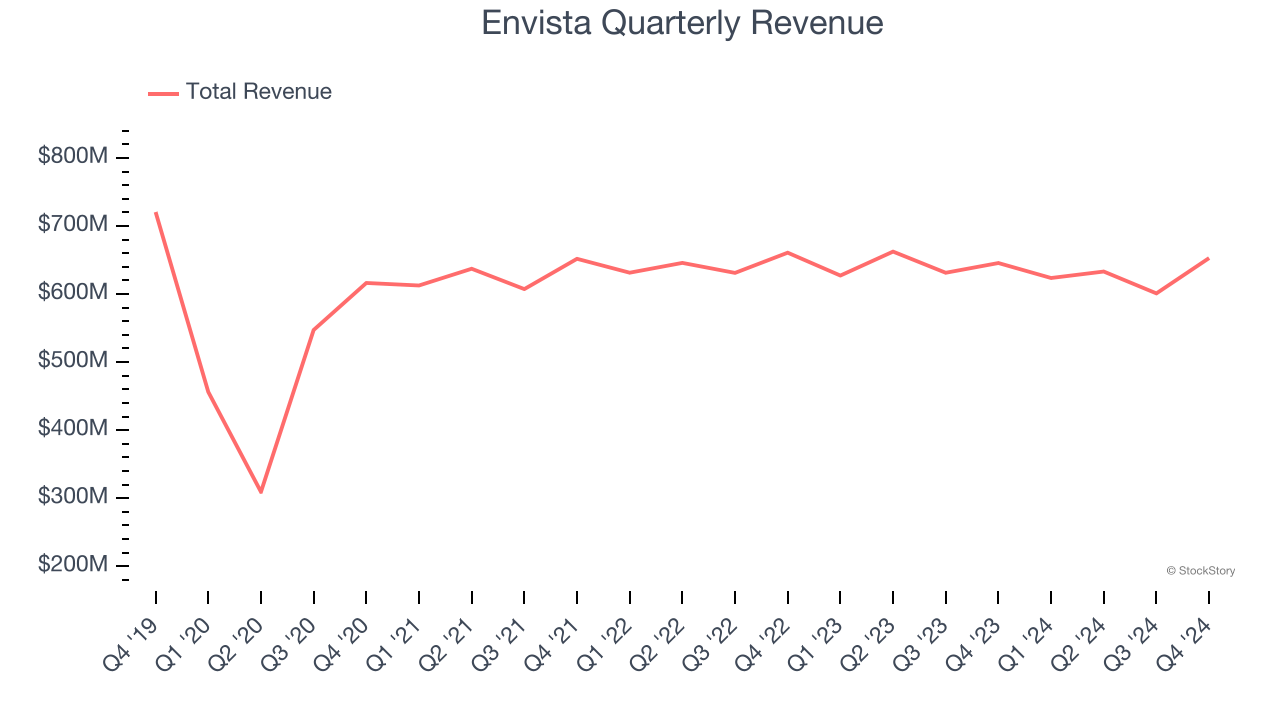

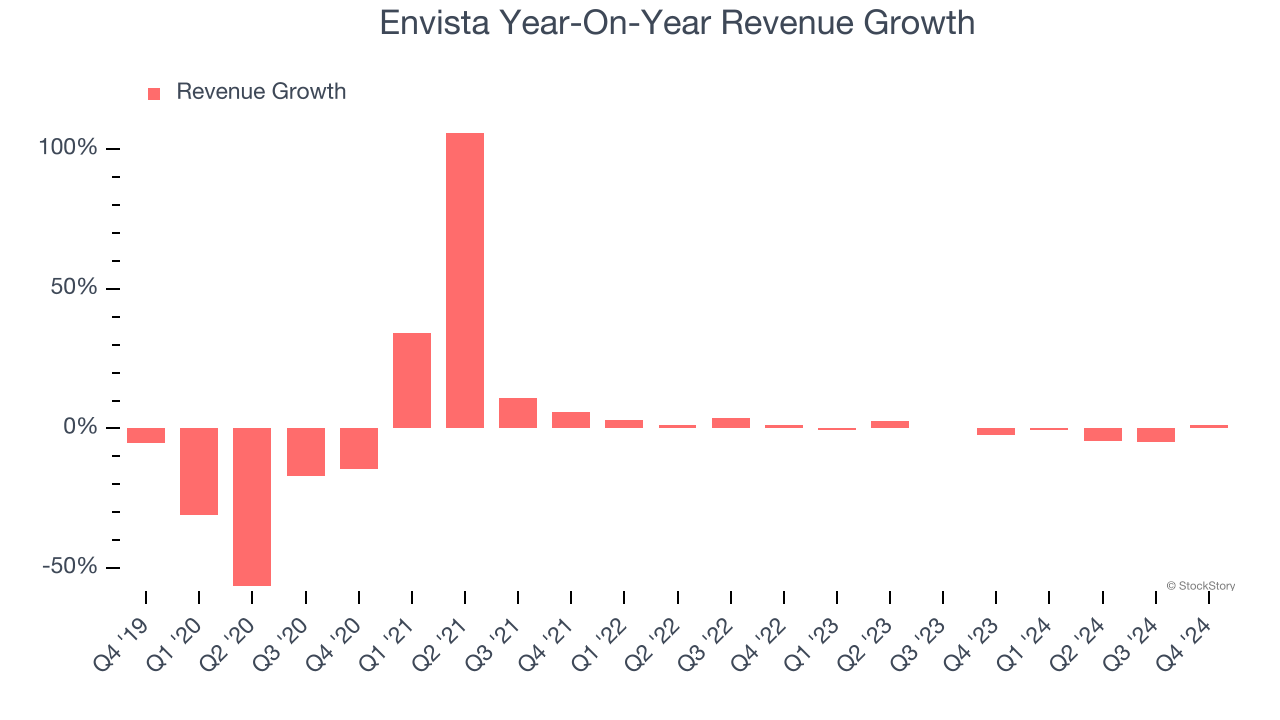

Dental products company Envista Holdings (NYSE:NVST) announced better-than-expected revenue in Q4 CY2024, with sales up 1.1% year on year to $652.9 million. Its non-GAAP profit of $0.24 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy Envista? Find out by accessing our full research report, it’s free.

Envista (NVST) Q4 CY2024 Highlights:

- Revenue: $652.9 million vs analyst estimates of $647.5 million (1.1% year-on-year growth, 0.8% beat)

- Adjusted EPS: $0.24 vs analyst estimates of $0.22 (9.9% beat)

- Adjusted EBITDA: $91 million vs analyst estimates of $78.47 million (13.9% margin, 16% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $1 at the midpoint, missing analyst estimates by 10.9%

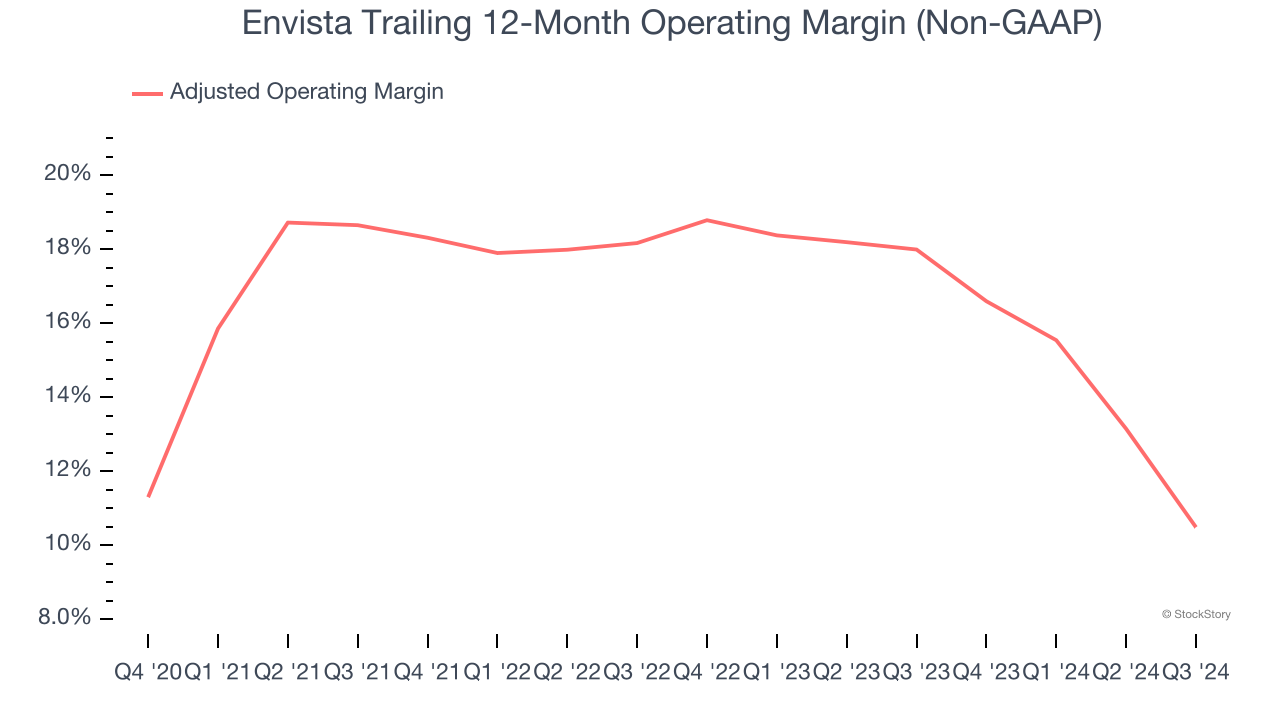

- Operating Margin: 7.1%, up from -31.4% in the same quarter last year

- Free Cash Flow Margin: 19%, up from 14.5% in the same quarter last year

- Market Capitalization: $3.54 billion

"In Q4 2024, Envista delivered results that were in line with expectations, indicating that our focus on growth, operations, and people is having a positive impact," said Paul Keel, Envista's CEO.

Company Overview

Spun off from Danaher in 2019, Envista Holdings (NYSE:NVST) designs, manufactures, and markets a wide range of dental solutions, including diagnostic tools, implants, orthodontics, and consumables.

Dental Equipment & Technology

The dental equipment and technology industry encompasses companies that manufacture orthodontic products, dental implants, imaging systems, and digital tools for dental professionals. These companies benefit from recurring revenue streams tied to consumables, ongoing maintenance, and growing demand for aesthetic and restorative dentistry. However, high R&D costs, significant capital investment requirements, and reliance on discretionary spending make them vulnerable to economic cycles. Over the next few years, tailwinds for the sector include innovation in digital workflows, such as 3D printing and AI-driven diagnostics, which enhance the efficiency and precision of dental care. However, headwinds include economic uncertainty, which could reduce patient spending on elective procedures, regulatory challenges, and potential pricing pressures from consolidated dental service organizations (DSOs).

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Envista struggled to consistently generate demand over the last five years as its sales dropped at a 1.8% annual rate. This was below our standards and signals it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Envista’s annualized revenue declines of 1.1% over the last two years align with its five-year trend, suggesting its demand consistently shrunk.

This quarter, Envista reported modest year-on-year revenue growth of 1.1% but beat Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Adjusted Operating Margin

Envista has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average adjusted operating margin of 15.4%.

Analyzing the trend in its profitability, Envista’s adjusted operating margin rose by 1.3 percentage points over the last five years. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 9.3 percentage points on a two-year basis. If Envista wants to pass our bar, it must prove it can expand its profitability consistently.

This quarter, Envista generated an adjusted operating profit margin of 13.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

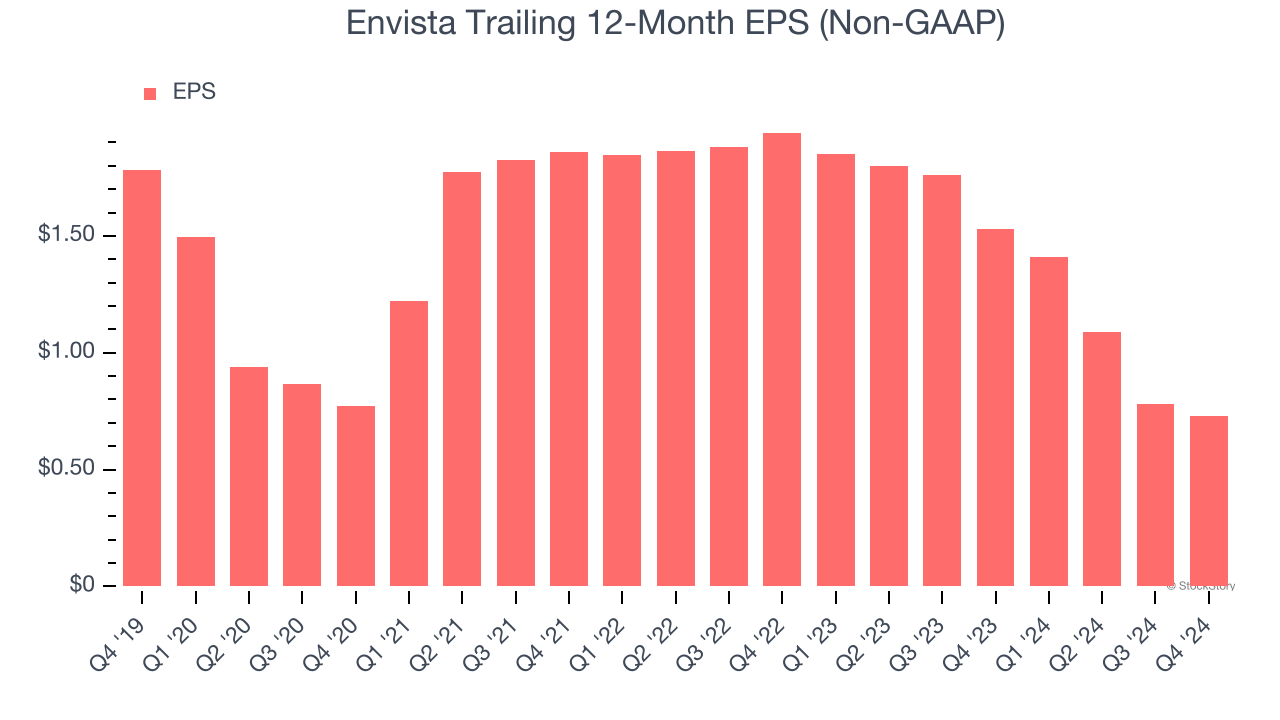

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Envista, its EPS declined by more than its revenue over the last five years, dropping 16.3% annually. However, its adjusted operating margin actually expanded during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

We can take a deeper look into Envista’s earnings to better understand the drivers of its performance. A five-year view shows Envista has diluted its shareholders, growing its share count by 9%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Envista reported EPS at $0.24, down from $0.29 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.9%. Over the next 12 months, Wall Street expects Envista’s full-year EPS of $0.73 to grow 53.7%.

Key Takeaways from Envista’s Q4 Results

It was good to see Envista narrowly top analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed significantly. Overall, this quarter could have been better. The stock remained flat at $20.57 immediately after reporting.

The latest quarter from Envista’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.