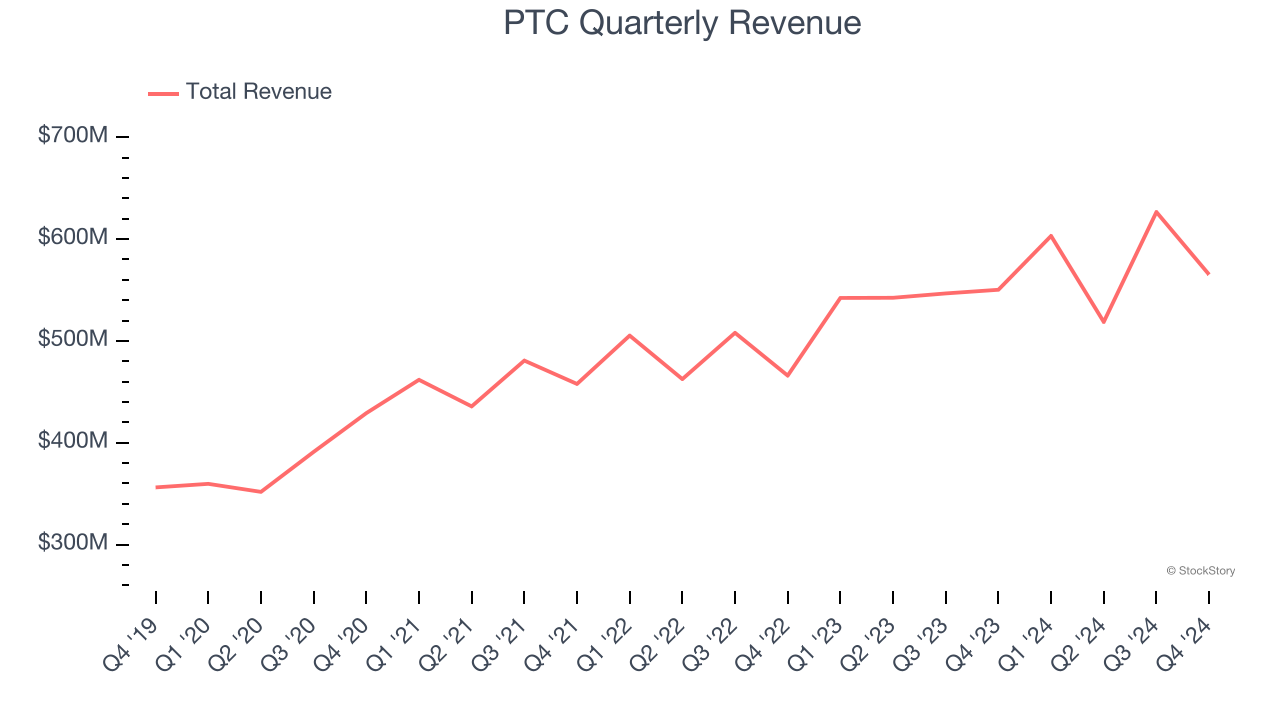

Engineering and design software provider PTC (NASDAQ:PTC) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 2.7% year on year to $565.1 million. On the other hand, next quarter’s revenue guidance of $605 million was less impressive, coming in 5.8% below analysts’ estimates. Its GAAP profit of $0.68 per share was 26.6% above analysts’ consensus estimates.

Is now the time to buy PTC? Find out by accessing our full research report, it’s free.

PTC (PTC) Q4 CY2024 Highlights:

- Revenue: $565.1 million vs analyst estimates of $554.8 million (2.7% year-on-year growth, 1.9% beat)

- EPS (GAAP): $0.68 vs analyst estimates of $0.54 (26.6% beat)

- Adjusted Operating Income: $191.3 million vs analyst estimates of $175.3 million (33.9% margin, 9.2% beat)

- The company dropped its revenue guidance for the full year to $2.48 billion at the midpoint from $2.56 billion, a 2.9% decrease

- Operating Margin: 20.4%, down from 21.6% in the same quarter last year

- Free Cash Flow Margin: 41.7%, up from 14.9% in the previous quarter

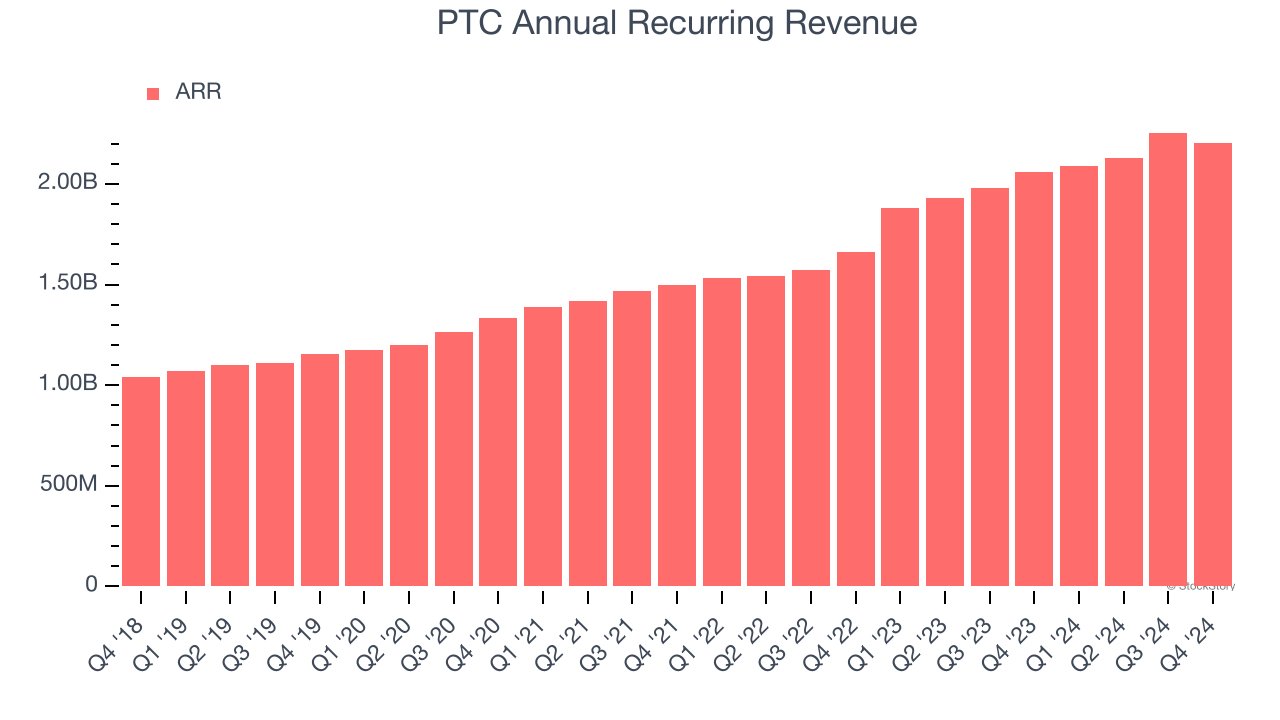

- Annual Recurring Revenue: $2.21 billion at quarter end, up 7.2% year on year

- Market Capitalization: $23 billion

"In Q1'25, we delivered solid year-over-year constant currency ARR growth of 11% and cash flow growth above 25%, which was in-line with our guidance. Our differentiated strategy leverages our unique portfolio to help product companies accelerate their time to market and manage increasing complexity. It's an exciting time because our products are at the epicenter of driving business transformation at our customers," said Neil Barua, President and CEO, PTC.

Company Overview

Used to design the Airbus A380 and Boeing 787 Dreamliner commercial airplanes, PTC’s (NASDAQ:PTC) software-as-service platform helps engineers and designers create and test products before manufacturing.

Design Software

The demand for rich, interactive 2D, 3D, VR and AR experiences is growing, and while the ubiquitous metaverse might still be more of a buzzword than a real thing, what is real is the demand for the tools to create these experiences, whether they are games, 3D tours or interactive movies.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, PTC’s sales grew at a sluggish 8% compounded annual growth rate over the last three years. This fell short of our benchmark for the software sector, but there are still things to like about PTC.

This quarter, PTC reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 1.9%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months, an acceleration versus the last three years. This projection is admirable and suggests its newer products and services will catalyze better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

PTC’s ARR punched in at $2.21 billion in Q4, and over the last four quarters, its growth slightly outpaced the sector as it averaged 10.6% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

PTC’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from PTC’s Q4 Results

It was encouraging to see PTC beat analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance was lowered and missed significantly. Additionally, its revenue guidance for next quarter also fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4% to $182 immediately after reporting.

PTC’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.