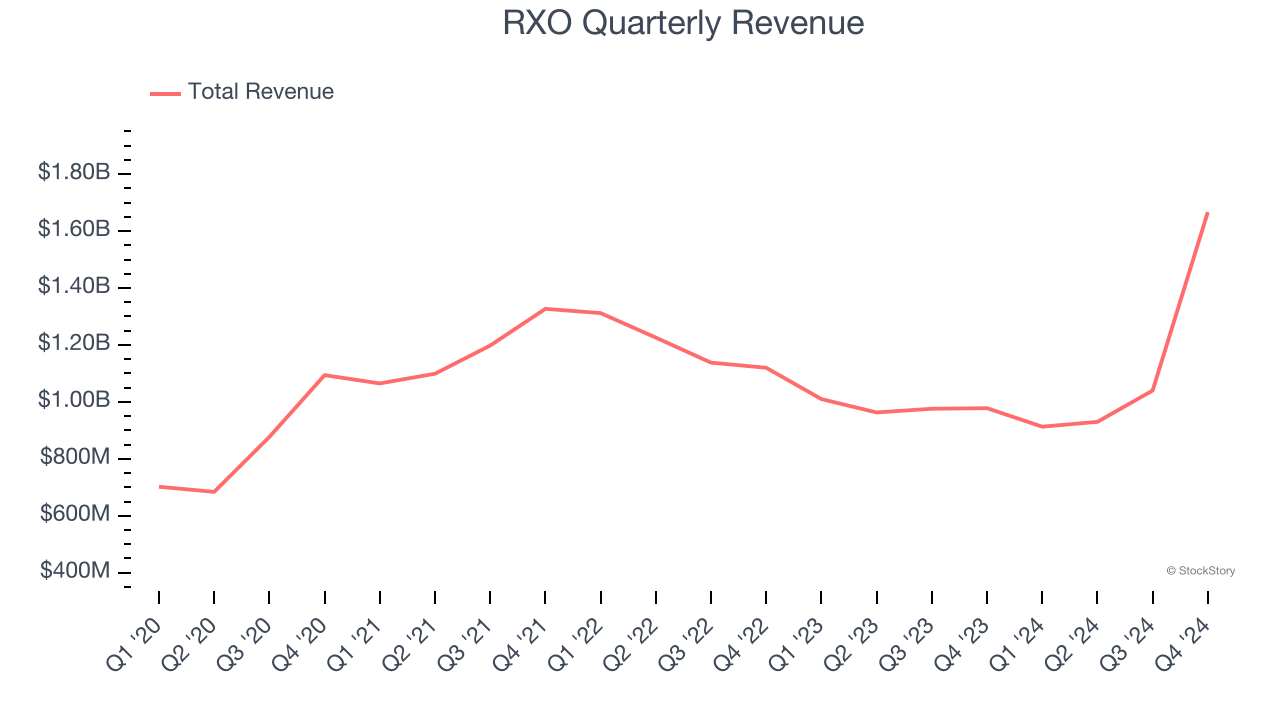

Freight Delivery Company RXO (NYSE:RXO) announced better-than-expected revenue in Q4 CY2024, with sales up 70.4% year on year to $1.67 billion. Its non-GAAP profit of $0.06 per share was in line with analysts’ consensus estimates.

Is now the time to buy RXO? Find out by accessing our full research report, it’s free.

RXO (RXO) Q4 CY2024 Highlights:

- Revenue: $1.67 billion vs analyst estimates of $1.66 billion (70.4% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.06 vs analyst estimates of $0.06 (in line)

- Adjusted EBITDA: $42 million vs analyst estimates of $41.45 million (2.5% margin, 1.3% beat)

- EBITDA guidance for Q1 CY2025 is $25 million at the midpoint, below analyst estimates of $30.43 million

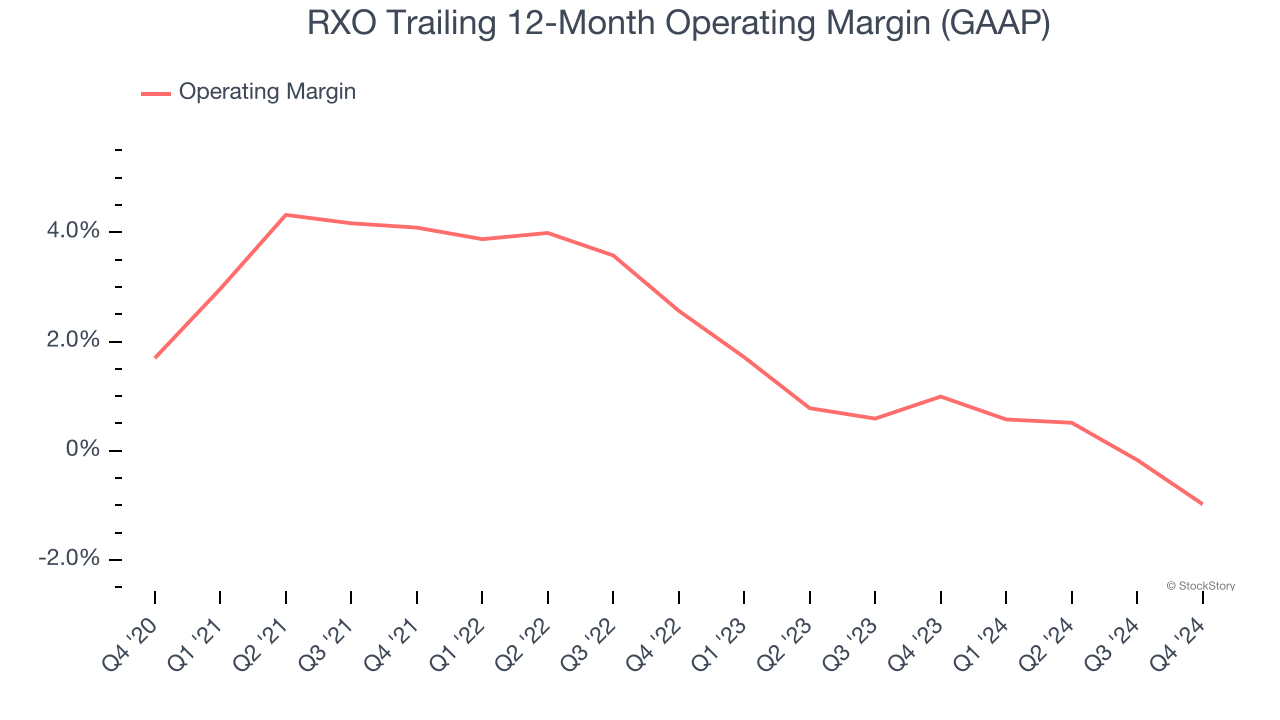

- Operating Margin: -1.4%, down from 1.4% in the same quarter last year

- Free Cash Flow was -$19 million, down from $1 million in the same quarter last year

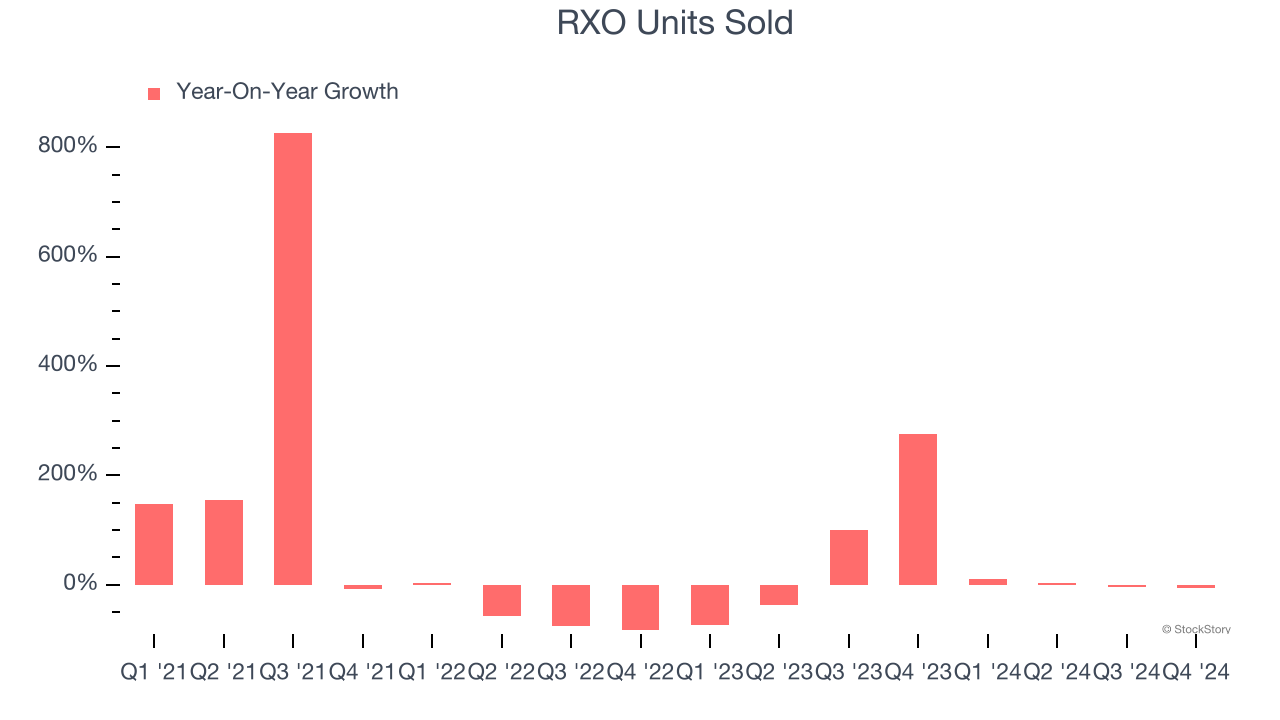

- Sales Volumes fell 6% year on year (275% in the same quarter last year)

- Market Capitalization: $4.06 billion

Drew Wilkerson, chief executive officer of RXO, said, “The integration of Coyote Logistics remains ahead of schedule and we’re again raising our estimate for annualized cost synergies. We now expect to achieve at least $50 million in synergies.”

Company Overview

With access to millions of trucks, RXO (NYSE:RXO) offers full-truckload, less-than-truckload, and last-mile deliveries.

Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, RXO’s 7.9% annualized revenue growth over the last four years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

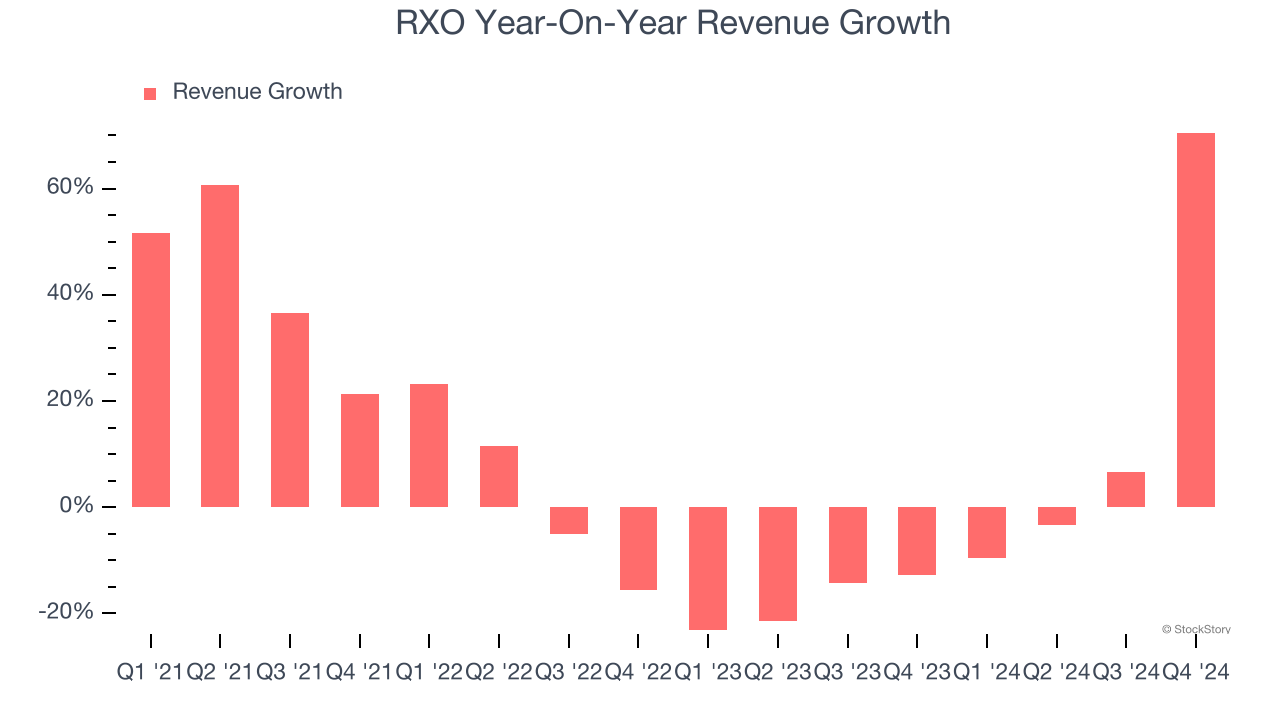

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. RXO’s recent history marks a sharp pivot from its four-year trend as its revenue has shown annualized declines of 2.6% over the last two years. RXO isn’t alone in its struggles as the Ground Transportation industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

We can dig further into the company’s revenue dynamics by analyzing its units sold. Over the last two years, RXO’s units sold averaged 33.4% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, RXO reported magnificent year-on-year revenue growth of 70.4%, and its $1.67 billion of revenue beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 50.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will fuel better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

RXO was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.7% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, RXO’s operating margin decreased by 2.7 percentage points over the last five years. The company’s performance was poor no matter how you look at it - it shows operating expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, RXO generated an operating profit margin of negative 1.4%, down 2.9 percentage points year on year. Since RXO’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

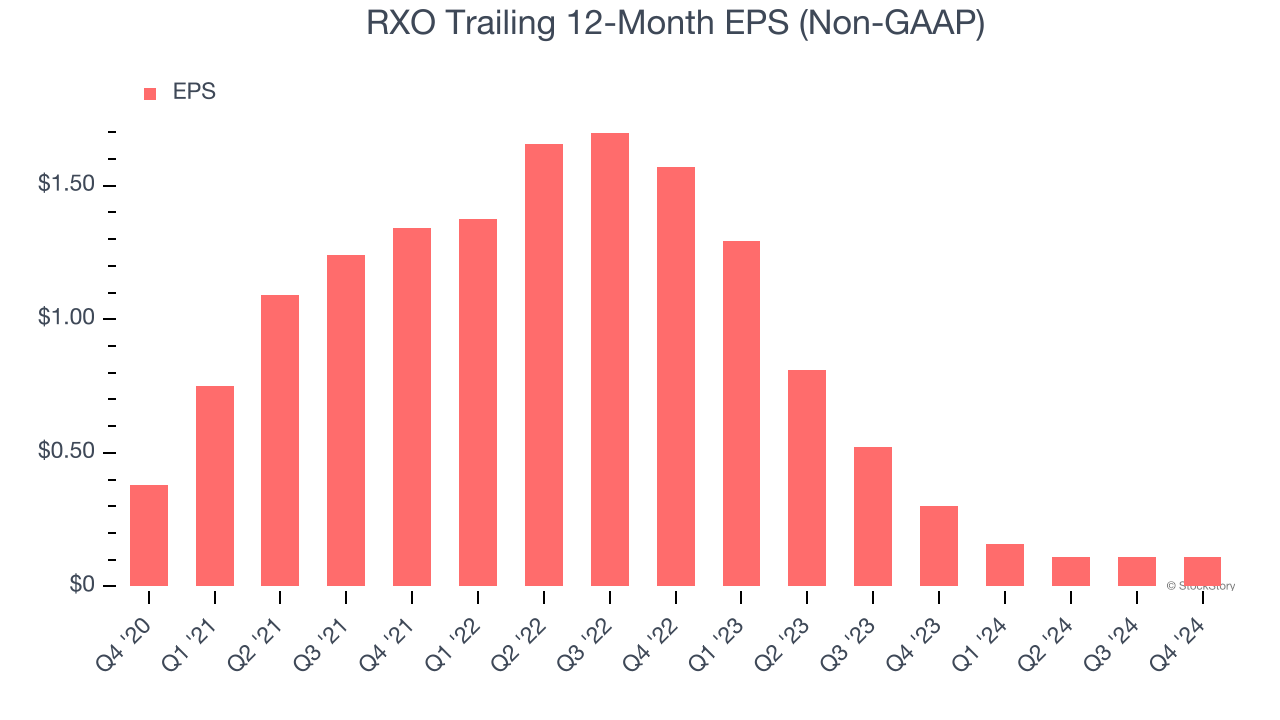

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for RXO, its EPS declined by 26.5% annually over the last four years while its revenue grew by 7.9%. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For RXO, its two-year annual EPS declines of 73.5% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, RXO reported EPS at $0.06, in line with the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects RXO to perform poorly. Analysts forecast its full-year EPS of $0.11 will hit $0.42.

Key Takeaways from RXO’s Q4 Results

It was good to see RXO narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA guidance for next quarter missed significantly, weighing on shares. The stock traded down 5.2% to $24.01 immediately after reporting.

Big picture, is RXO a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.