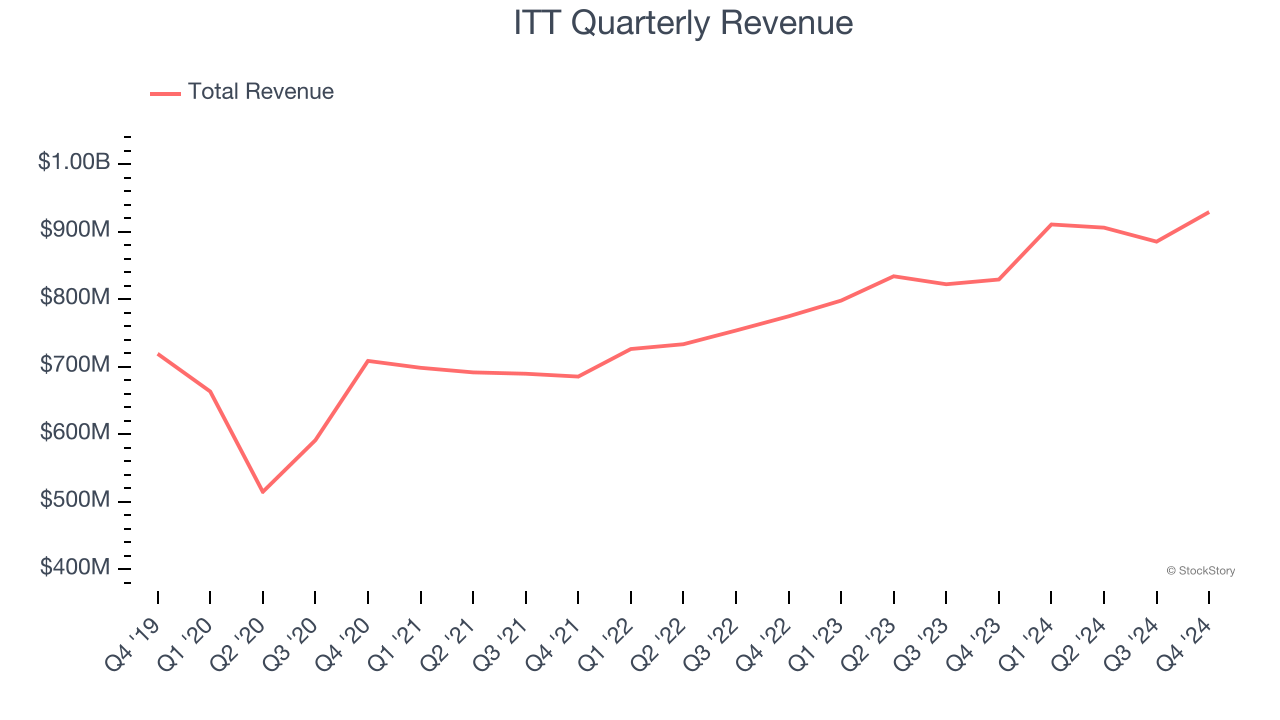

Engineered components manufacturer for critical industries ITT Inc. (NYSE: ITT) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 12% year on year to $929 million. Its non-GAAP profit of $1.50 per share was 1.8% above analysts’ consensus estimates.

Is now the time to buy ITT? Find out by accessing our full research report, it’s free.

ITT (ITT) Q4 CY2024 Highlights:

- Revenue: $929 million vs analyst estimates of $928.3 million (12% year-on-year growth, in line)

- Adjusted EPS: $1.50 vs analyst estimates of $1.47 (1.8% beat)

- Adjusted EBITDA: $222.4 million vs analyst estimates of $201.8 million (23.9% margin, 10.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $6.30 at the midpoint, missing analyst estimates by 3%

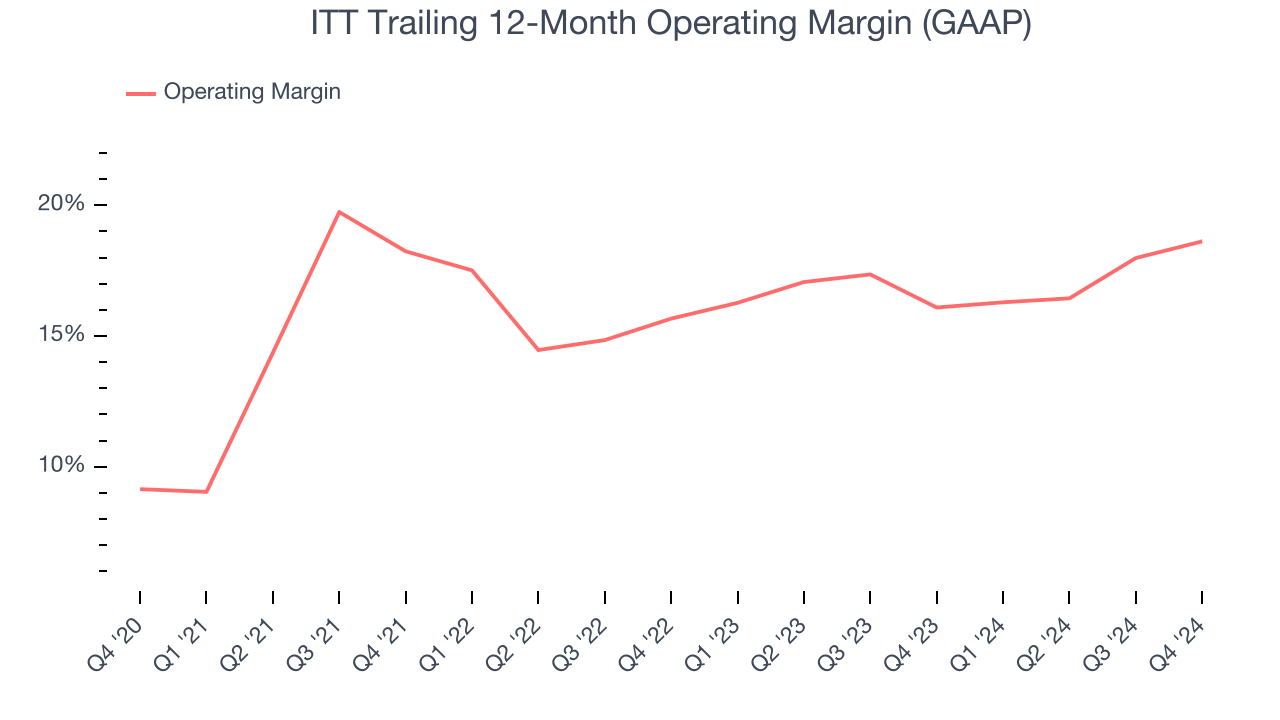

- Operating Margin: 17.2%, up from 14.3% in the same quarter last year

- Free Cash Flow Margin: 20.1%, up from 15.8% in the same quarter last year

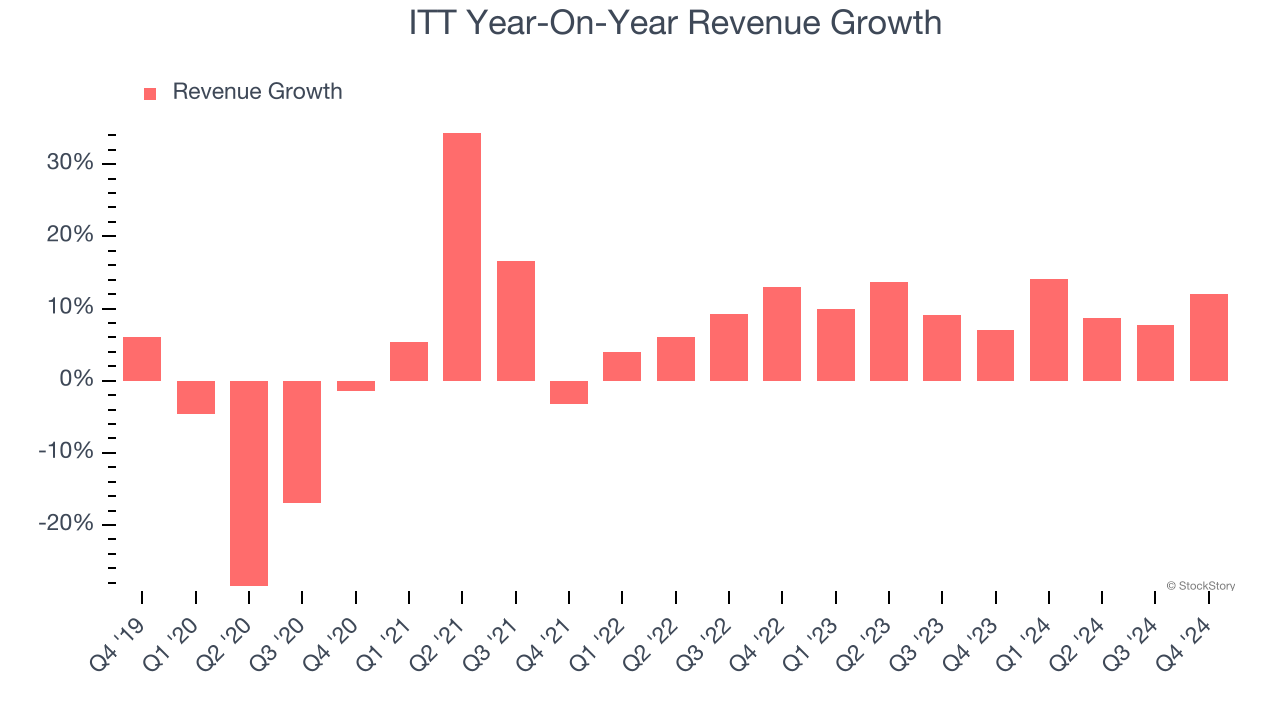

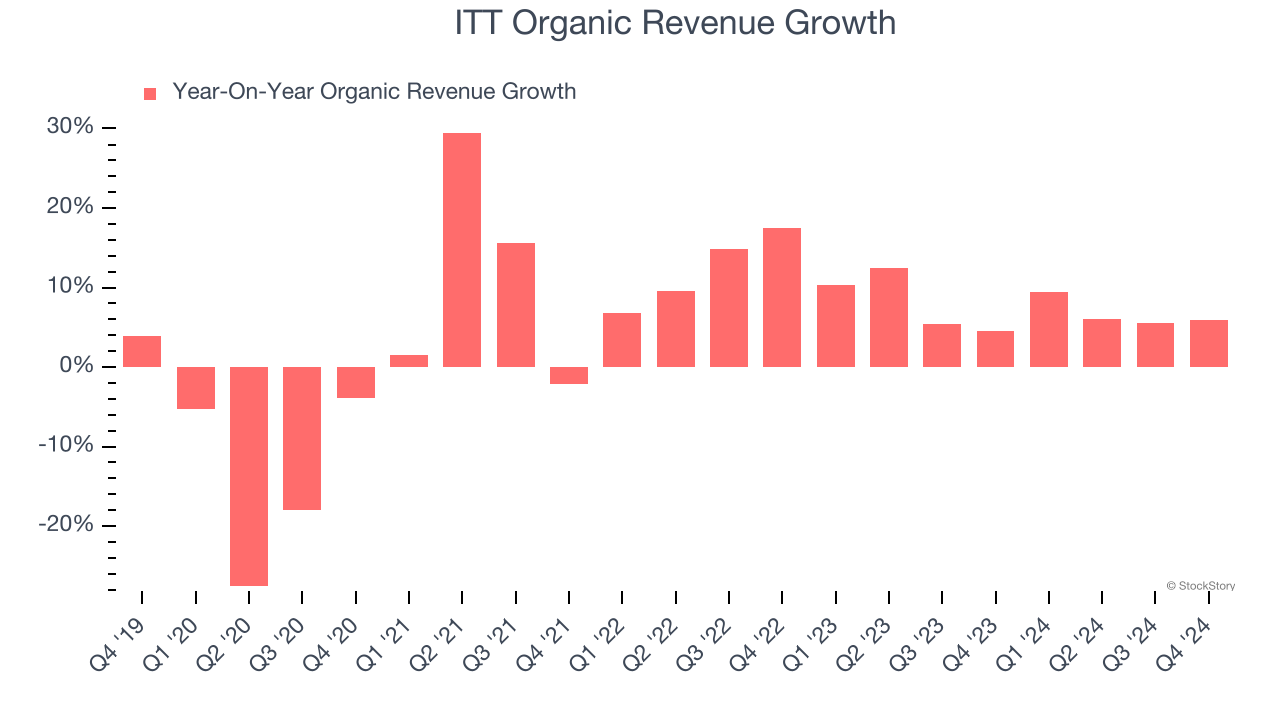

- Organic Revenue rose 5.9% year on year (4.5% in the same quarter last year)

- Market Capitalization: $12.19 billion

“In 2024, our teams delivered on our commitments once again. We grew revenues 11% in total, 7% organically, with strength across all segments. Our businesses drove strong margin expansion and eclipsed our long-term margin target two years ahead of plan. We deployed over $860 million of capital through the acquisitions of cryogenic pump manufacturer, Svanehøj, and defense interconnect specialist, kSARIA. These acquisitions, coupled with the divestiture of our automotive component business, significantly enhanced ITT’s opportunities in higher growth and higher margin flow and connectors businesses whilst strategically shifting our portfolio. On top of this, we invested over $100 million in growth and productivity to further our differentiation, paid down over $500 million of debt related to M&A, and returned over $200 million of capital to shareholders. We entered 2025 with a $1.6 billion backlog, continued growth and margin expansion opportunities in our core and ramping value creation from our acquisitions,” said Luca Savi, ITT’s Chief Executive Officer and President.

Company Overview

Playing a crucial role in the development of the first transatlantic television transmission in 1956, ITT (NYSE:ITT) provides motion and fluid handling equipment for various industries

Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, ITT’s sales grew at a tepid 5% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector, but there are still things to like about ITT.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. ITT’s annualized revenue growth of 10.2% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

ITT also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, ITT’s organic revenue averaged 7.4% year-on-year growth. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, ITT’s year-on-year revenue growth was 12%, and its $929 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

ITT has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 15.9%.

Looking at the trend in its profitability, ITT’s operating margin rose by 9.5 percentage points over the last five years, showing its efficiency has meaningfully improved.

In Q4, ITT generated an operating profit margin of 17.2%, up 2.9 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

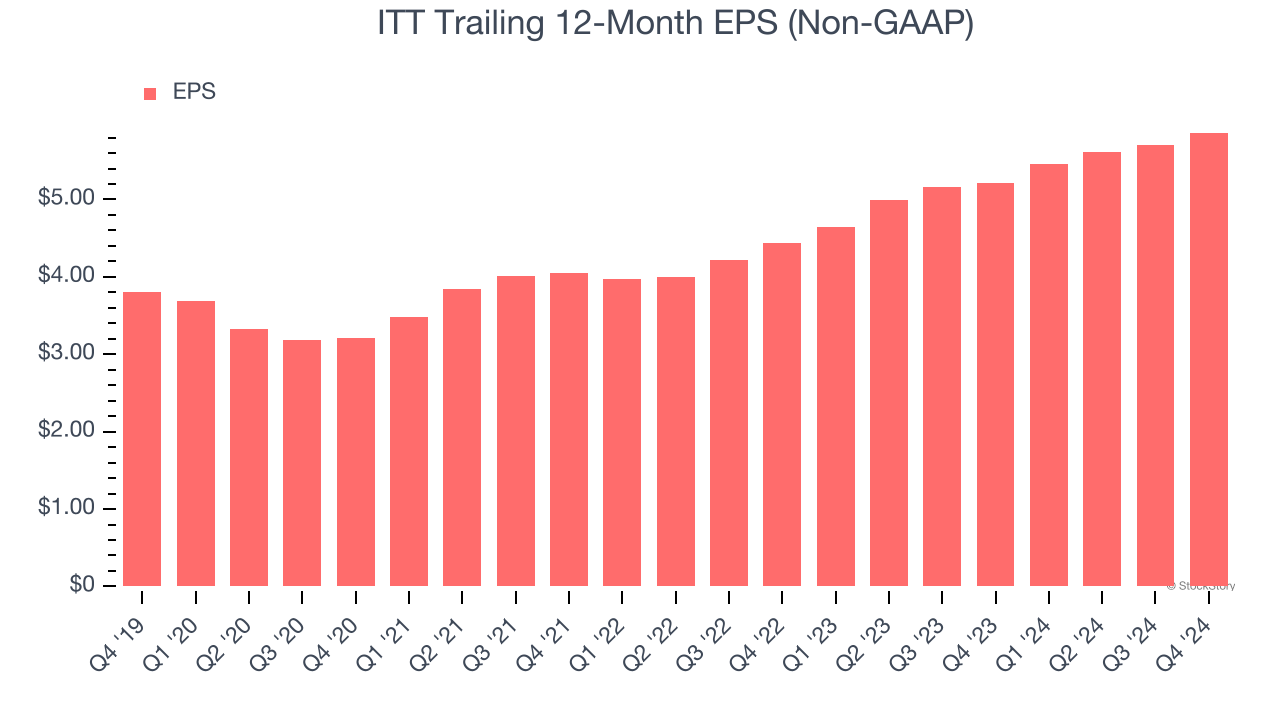

ITT’s EPS grew at a decent 9% compounded annual growth rate over the last five years, higher than its 5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

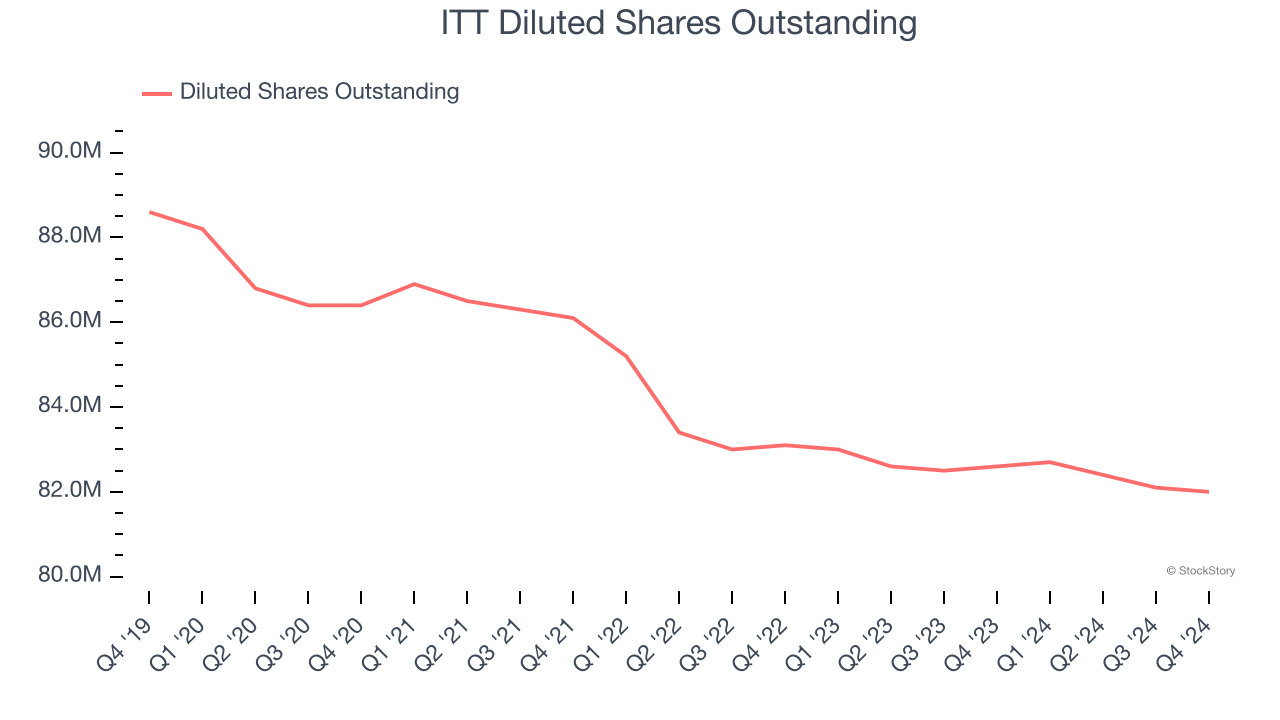

We can take a deeper look into ITT’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, ITT’s operating margin expanded by 9.5 percentage points over the last five years. On top of that, its share count shrank by 7.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ITT, its two-year annual EPS growth of 14.9% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, ITT reported EPS at $1.50, up from $1.34 in the same quarter last year. This print beat analysts’ estimates by 1.8%. Over the next 12 months, Wall Street expects ITT’s full-year EPS of $5.86 to grow 10.8%.

Key Takeaways from ITT’s Q4 Results

We were impressed by how significantly ITT blew past analysts’ EBITDA expectations this quarter. We were also glad its organic revenue and EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, this quarter had some positives but also blemishes. The stock remained flat at $151.17 immediately following the results.

Is ITT an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.