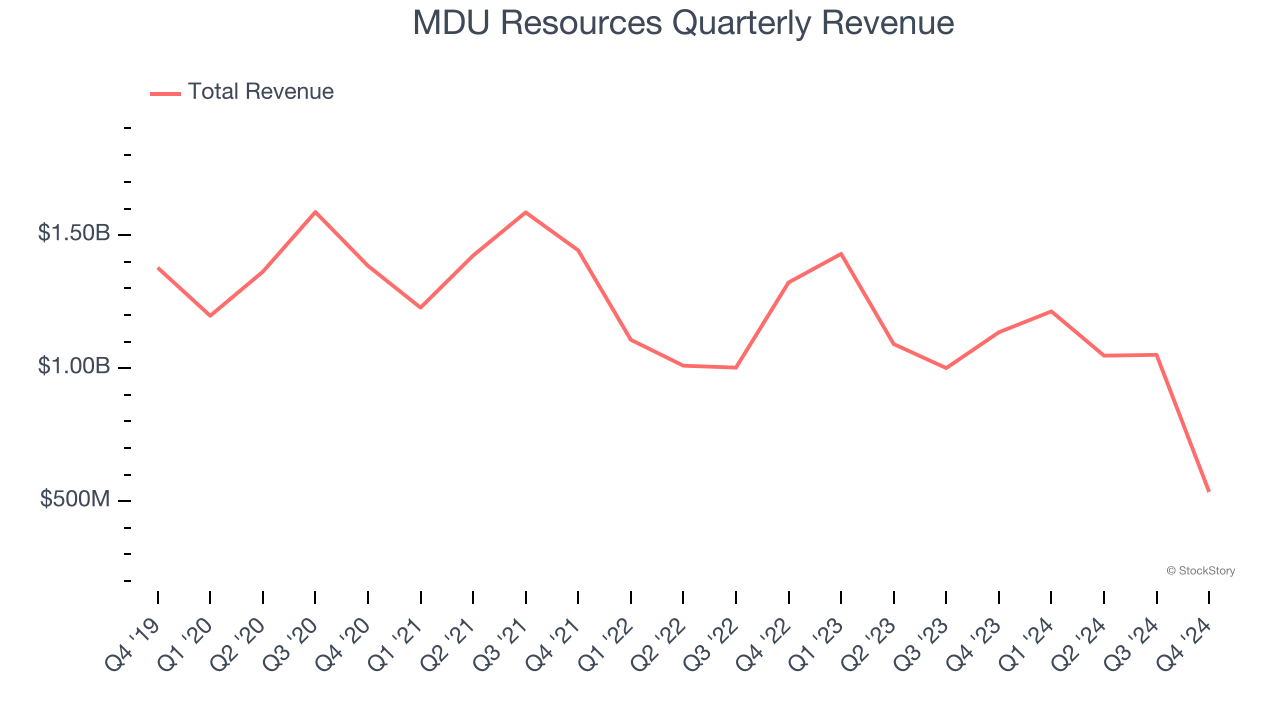

Energy and construction materials company MDU Resources (NYSE:MDU) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 52.8% year on year to $535.5 million. Its GAAP profit of $0.27 per share was 26% below analysts’ consensus estimates.

Is now the time to buy MDU Resources? Find out by accessing our full research report, it’s free.

MDU Resources (MDU) Q4 CY2024 Highlights:

- Revenue: $535.5 million vs analyst estimates of $790.6 million (52.8% year-on-year decline, 32.3% miss)

- EPS (GAAP): $0.27 vs analyst expectations of $0.37 (26% miss)

- Adjusted EBITDA: $145.3 million vs analyst estimates of $170.2 million (27.1% margin, 14.6% miss)

- EPS (GAAP) guidance for the upcoming financial year 2025 is $0.93 at the midpoint, missing analyst estimates by 3.6%

- Operating Margin: 17.6%, up from 12.7% in the same quarter last year

- Market Capitalization: $3.67 billion

"MDU Resources delivered exceptional results in 2024, underscoring the strength of our employees, strategic investments and continued focus on operational excellence," said Nicole A. Kivisto, President and CEO of MDU Resources.

Company Overview

Founded to provide electricity to towns in Minnesota, MDU Resources (NYSE:MDU) provides products and services in the utilities and construction materials industries.

Energy Products and Services

Areas like the energy transition and emission reduction are thematic and front of mind today. This can be a double-edged sword for the energy products and services industry. Those who innovate and build new expertise can jolt demand while those who cling to legacy technologies or fall behind in the trending areas could see their market shares diminish. Bigger picture, energy products and services companies are still at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

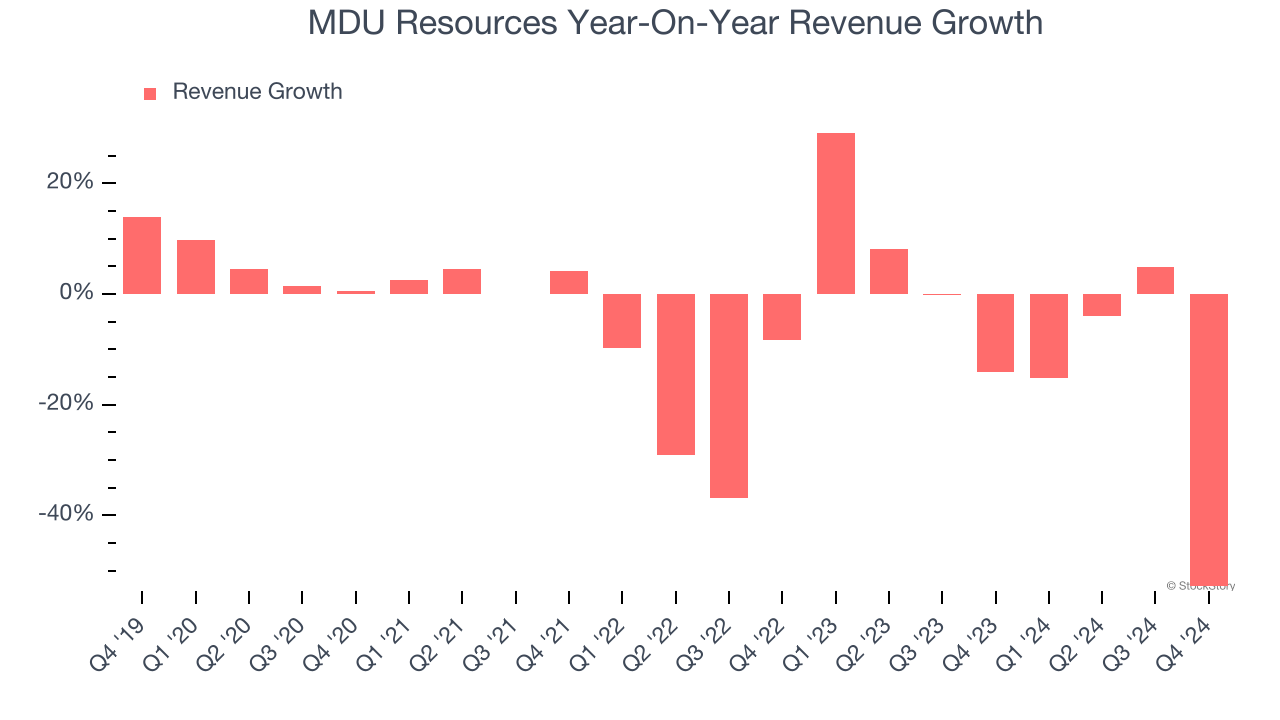

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. MDU Resources’s demand was weak over the last five years as its sales fell at a 6.3% annual rate. This was below our standards and signals it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. MDU Resources’s annualized revenue declines of 6.9% over the last two years align with its five-year trend, suggesting its demand consistently shrunk. MDU Resources isn’t alone in its struggles as the Energy Products and Services industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, MDU Resources missed Wall Street’s estimates and reported a rather uninspiring 52.8% year-on-year revenue decline, generating $535.5 million of revenue.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

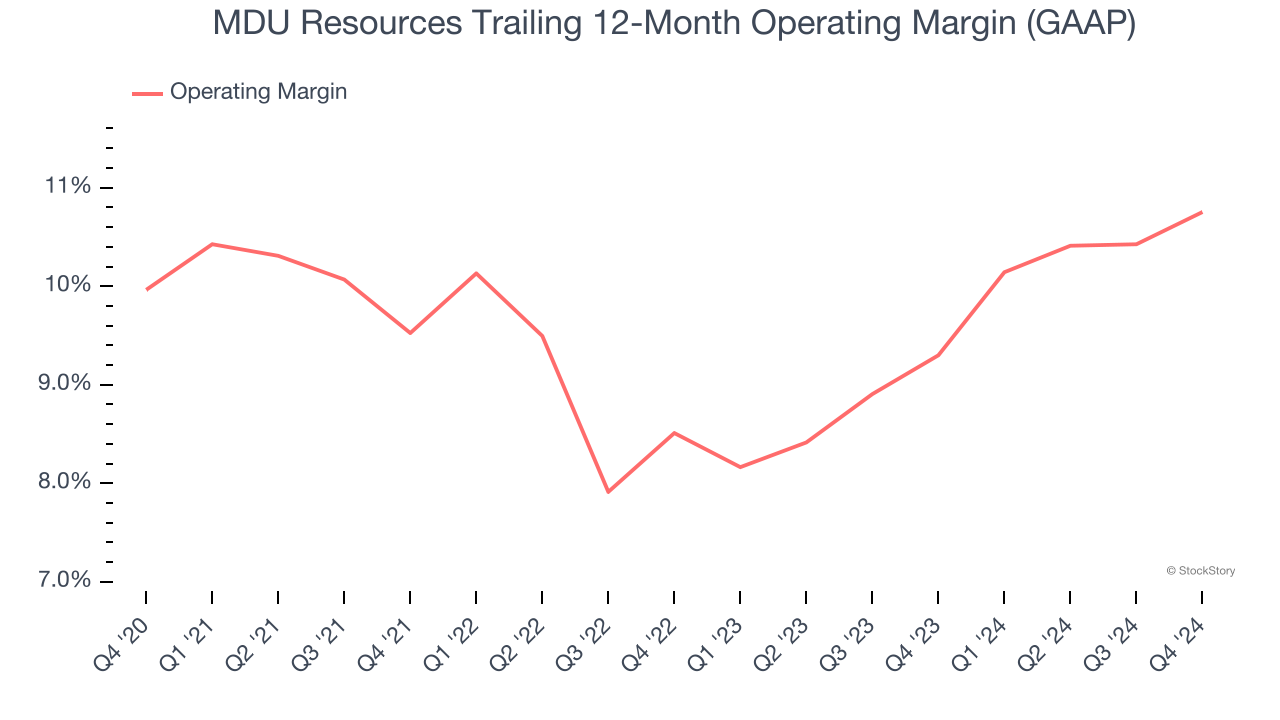

MDU Resources has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.6%, higher than the broader industrials sector.

Analyzing the trend in its profitability, MDU Resources’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years . Shareholders will want to see MDU Resources grow its margin in the future.

In Q4, MDU Resources generated an operating profit margin of 17.6%, up 4.9 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

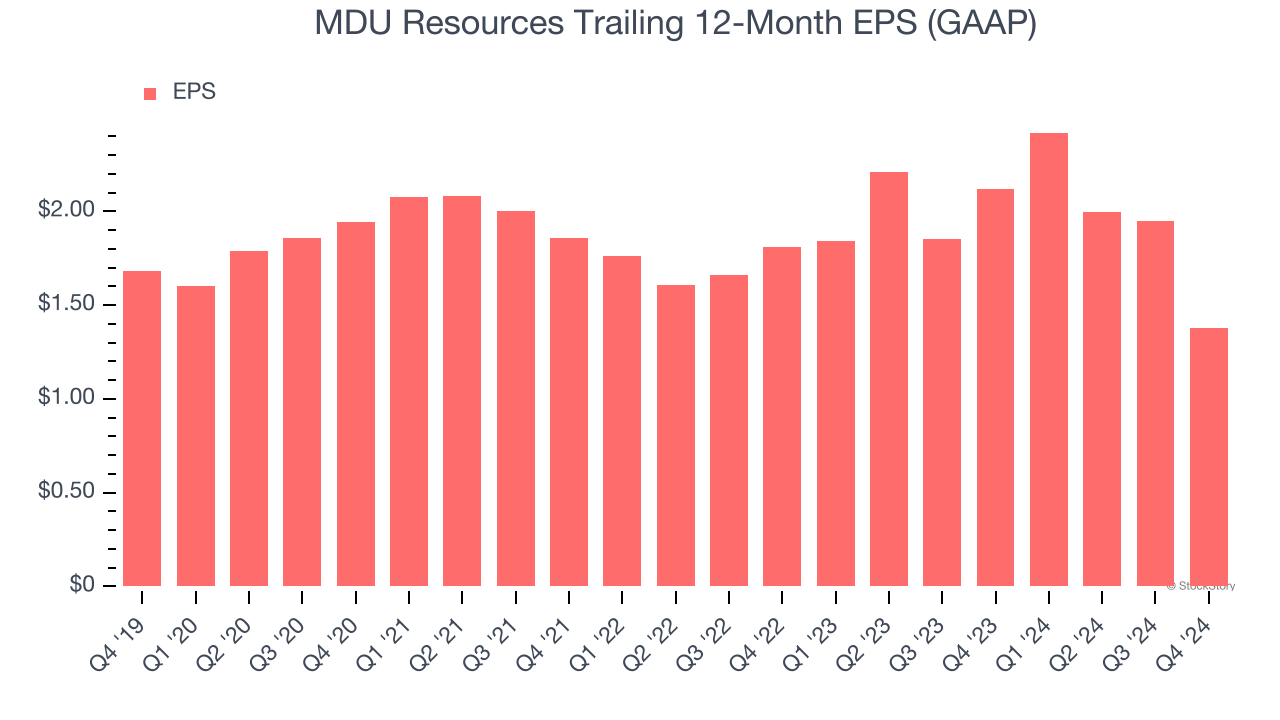

Sadly for MDU Resources, its EPS and revenue declined by 4% and 6.3% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, MDU Resources’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For MDU Resources, its two-year annual EPS declines of 12.8% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, MDU Resources reported EPS at $0.27, down from $0.84 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects MDU Resources’s full-year EPS of $1.38 to shrink by 34.6%.

Key Takeaways from MDU Resources’s Q4 Results

We struggled to find many positives in these results as its revenue, EPS, EBITDA, and full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.3% to $17.55 immediately following the results.

MDU Resources underperformed this quarter, but does that create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.