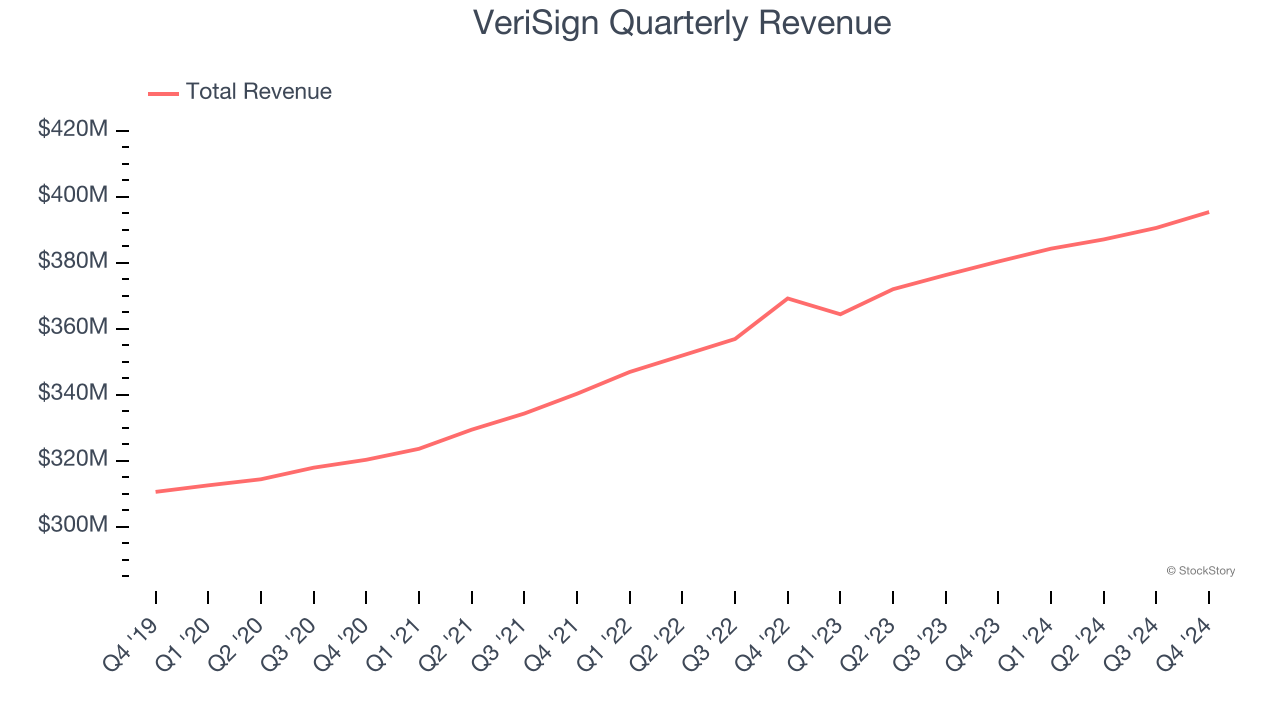

Domain name registry operator Verisign (NASDAQ:VRSN) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 3.9% year on year to $395.4 million. Its GAAP profit of $2 per share was in line with analysts’ consensus estimates.

Is now the time to buy VeriSign? Find out by accessing our full research report, it’s free.

VeriSign (VRSN) Q4 CY2024 Highlights:

- Revenue: $395.4 million vs analyst estimates of $394.9 million (3.9% year-on-year growth, in line)

- EPS (GAAP): $2 vs analyst estimates of $2.01 (in line)

- Operating Margin: 66.7%, in line with the same quarter last year

- Free Cash Flow Margin: 56.1%, down from 63.4% in the previous quarter

- Market Capitalization: $21.23 billion

Company Overview

While the company is not a domain registrar and does not directly sell domain names to end users, Verisign (NASDAQ:VRSN) operates and maintains the infrastructure to support domain names such as .com and .net.

E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, VeriSign’s 5.5% annualized revenue growth over the last three years was weak. This was below our standard for the software sector and is a poor baseline for our analysis.

This quarter, VeriSign grew its revenue by 3.9% year on year, and its $395.4 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, a slight deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

VeriSign does a decent job acquiring new customers, and its CAC payback period checked in at 46.5 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

Key Takeaways from VeriSign’s Q4 Results

There weren't any resounding positives in these results. Revenue and EPS were in line with expectations. The stock traded down 2.3% to $215 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.