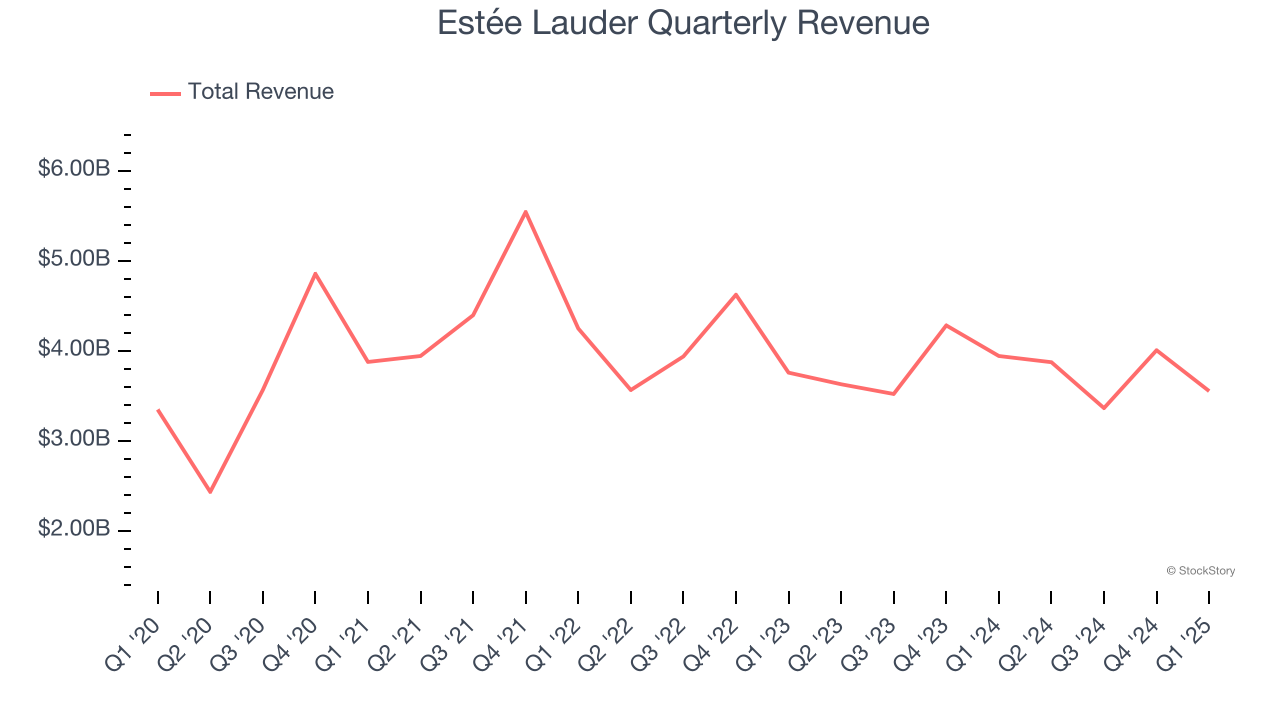

Beauty products company Estée Lauder (NYSE:EL) announced better-than-expected revenue in Q1 CY2025, but sales fell by 9.9% year on year to $3.55 billion. Its non-GAAP profit of $0.65 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Estée Lauder? Find out by accessing our full research report, it’s free.

Estée Lauder (EL) Q1 CY2025 Highlights:

- Revenue: $3.55 billion vs analyst estimates of $3.51 billion (9.9% year-on-year decline, 1.2% beat)

- Adjusted EPS: $0.65 vs analyst estimates of $0.31 (significant beat)

- Adjusted EBITDA: $510 million vs analyst estimates of $439.7 million (14.4% margin, 16% beat)

- Adjusted EPS guidance for the full year is $1.43 at the midpoint, beating analyst estimates by 2.4%

- Operating Margin: 8.6%, down from 13.5% in the same quarter last year

- Free Cash Flow Margin: 4.6%, down from 9.1% in the same quarter last year

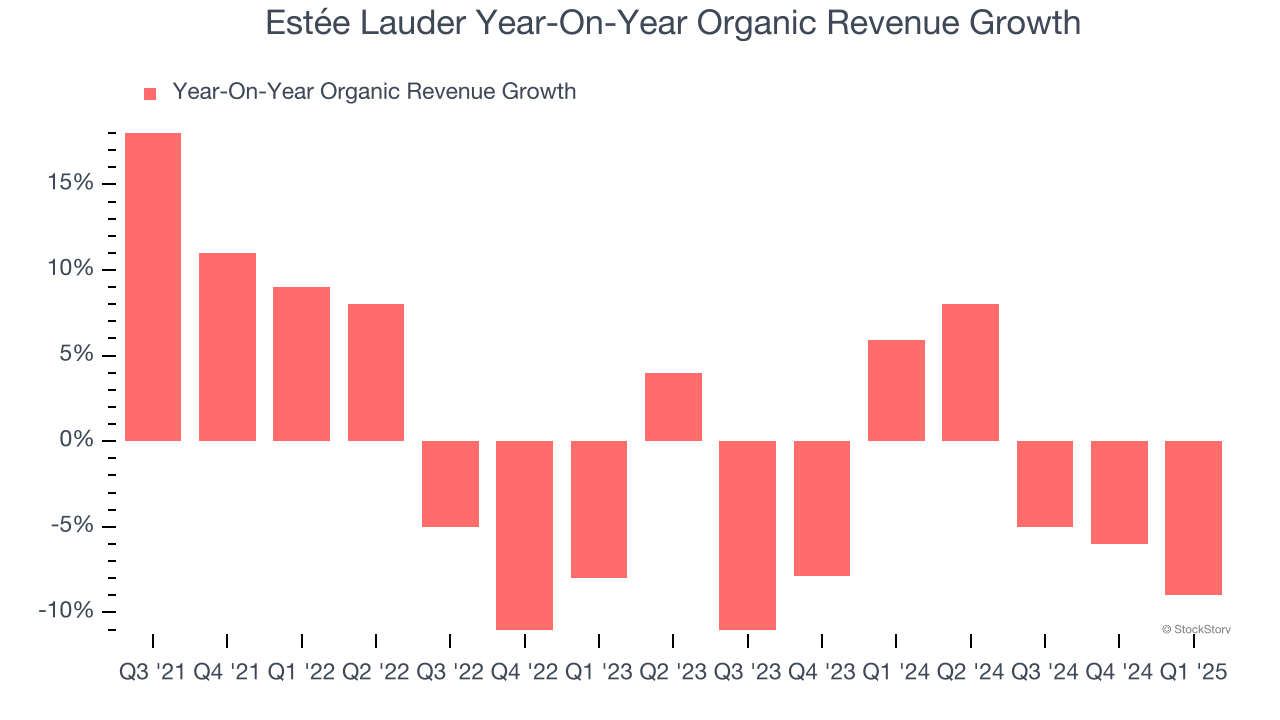

- Organic Revenue fell 9% year on year (5.9% in the same quarter last year)

- Market Capitalization: $21.57 billion

Stéphane de La Faverie, President and Chief Executive Officer, said, “In the third quarter of fiscal 2025, we delivered our organic sales outlook and exceeded profitability expectations. We are moving decisively and building momentum as we bring our “Beauty Reimagined” strategic vision to life across its five key priorities.

Company Overview

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE:EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $14.79 billion in revenue over the past 12 months, Estée Lauder is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To expand meaningfully, Estée Lauder likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Estée Lauder struggled to generate demand over the last three years. Its sales dropped by 6.6% annually, a tough starting point for our analysis.

This quarter, Estée Lauder’s revenue fell by 9.9% year on year to $3.55 billion but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products will fuel better top-line performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Estée Lauder’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 2.6% year on year.

In the latest quarter, Estée Lauder’s organic sales fell by 9% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Estée Lauder’s Q1 Results

We liked that Estée Lauder beat analysts’ revenue and EPS expectations this quarter. We were also excited its EPS guidance outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 3.3% to $61.85 immediately after reporting.

Sure, Estée Lauder had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.