Genomics company Illumina (NASDAQ:ILMN) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, but sales fell by 1.4% year on year to $1.04 billion. Its non-GAAP profit of $0.97 per share was 3.2% above analysts’ consensus estimates.

Is now the time to buy Illumina? Find out by accessing our full research report, it’s free.

Illumina (ILMN) Q1 CY2025 Highlights:

- Revenue: $1.04 billion vs analyst estimates of $1.04 billion (1.4% year-on-year decline, 0.5% beat)

- Adjusted EPS: $0.97 vs analyst estimates of $0.94 (3.2% beat)

- Adjusted Operating Income: $212 million vs analyst estimates of $211 million (20.4% margin, in line)

- Management lowered its full-year Adjusted EPS guidance to $4.25 at the midpoint, a 7.1% decrease

- Operating Margin: 15.8%, up from 11% in the same quarter last year

- Free Cash Flow Margin: 20%, up from 3.9% in the same quarter last year

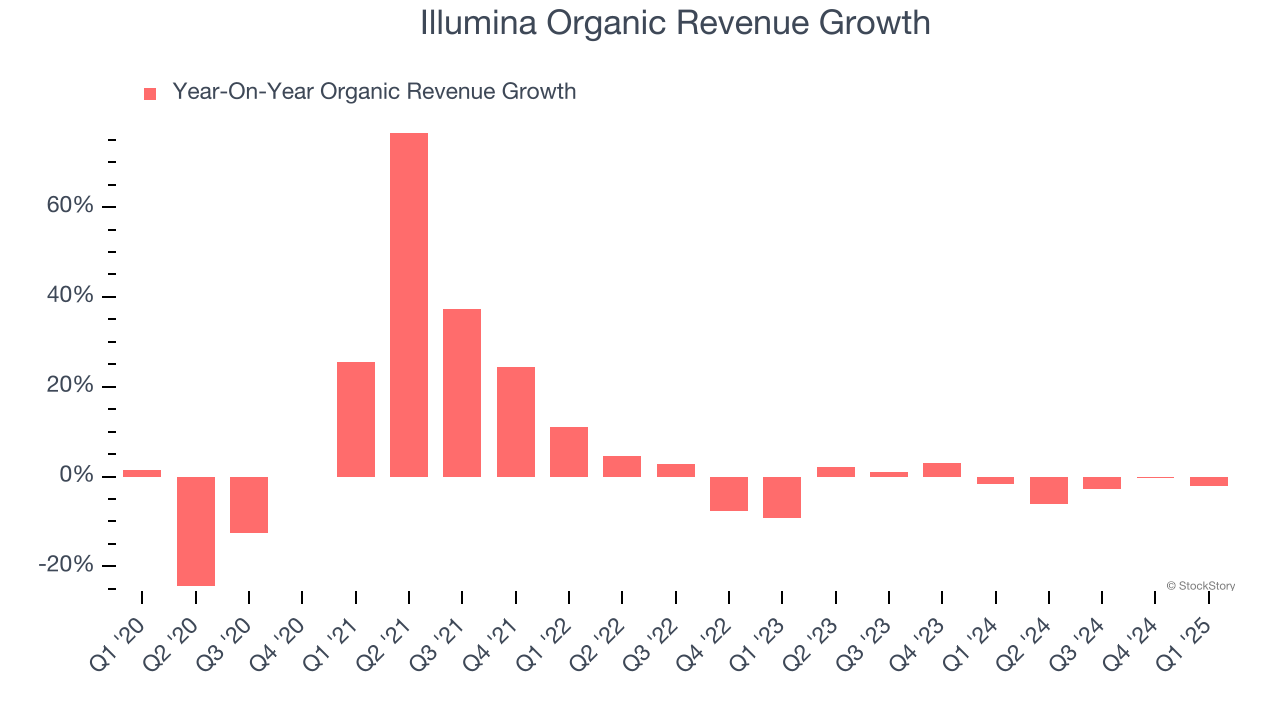

- Organic Revenue fell 2% year on year, in line with the same quarter last year

- Market Capitalization: $12.08 billion

Company Overview

Pioneering the ability to read the human genome at unprecedented speed and affordability, Illumina (NASDAQ:ILMN) develops and sells advanced DNA sequencing and microarray technologies that allow researchers and clinicians to analyze genetic variations and functions.

Sales Growth

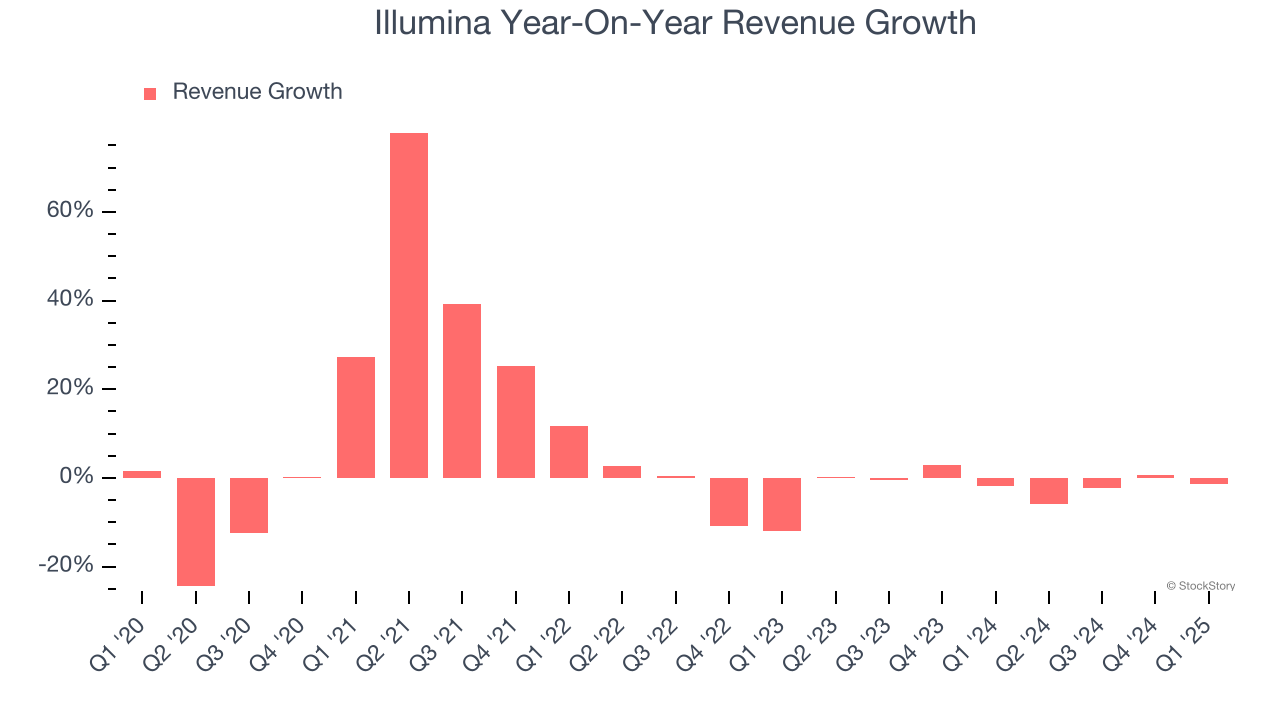

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Illumina’s sales grew at a tepid 4% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

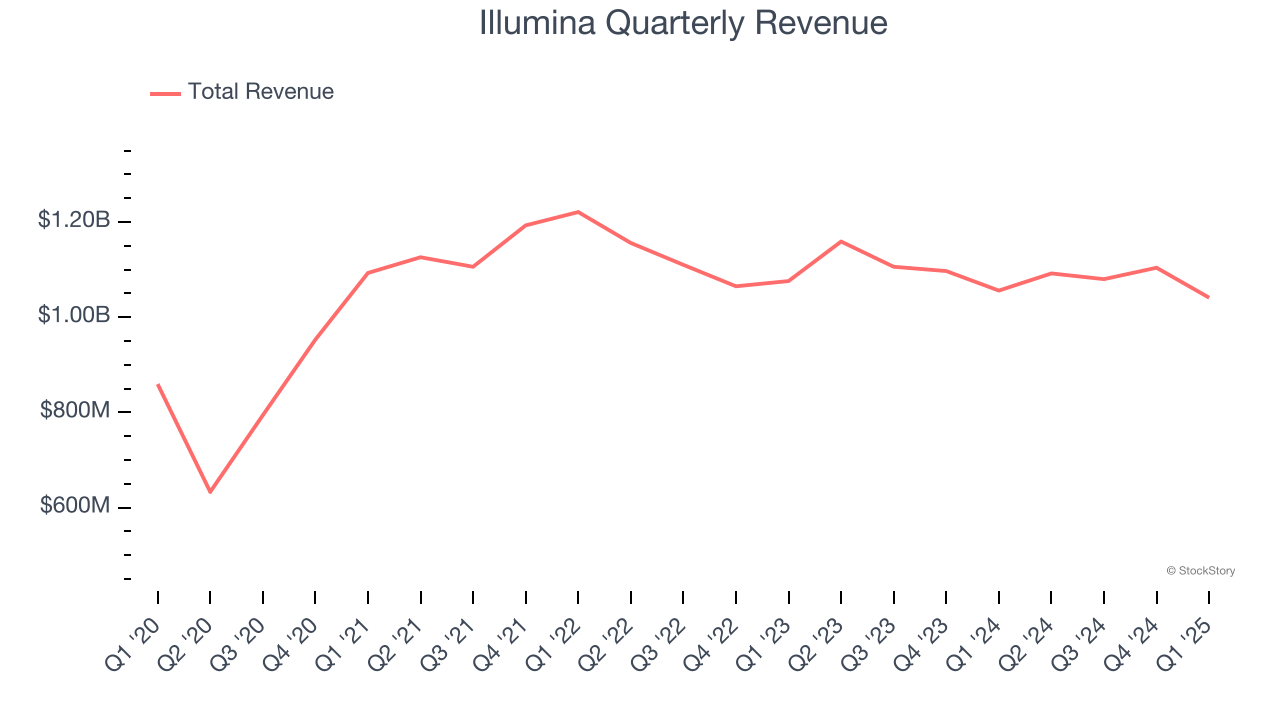

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Illumina’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1% annually.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Illumina’s organic revenue was flat. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Illumina’s revenue fell by 1.4% year on year to $1.04 billion but beat Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

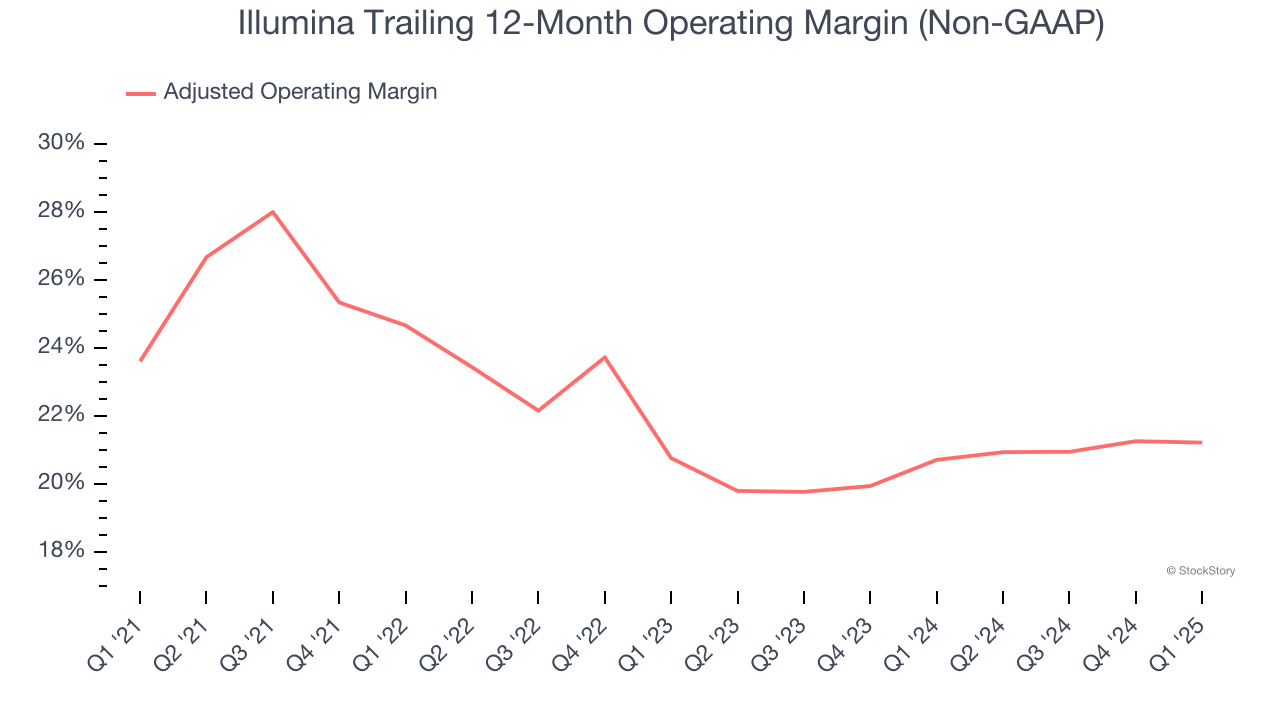

Illumina has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 22.2%.

Analyzing the trend in its profitability, Illumina’s adjusted operating margin decreased by 2.4 percentage points over the last five years. A silver lining is that on a two-year basis, its margin has stabilized. Still, shareholders will want to see Illumina become more profitable in the future.

In Q1, Illumina generated an adjusted operating profit margin of 20.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

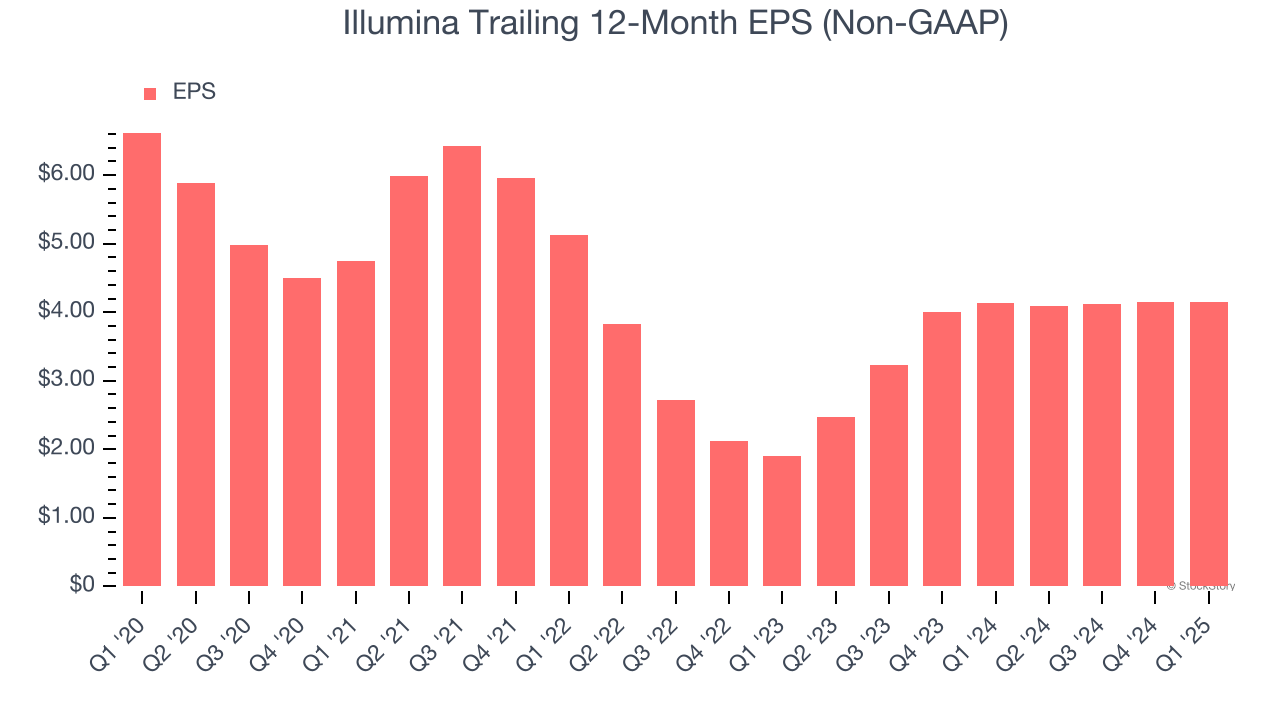

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Illumina, its EPS declined by 8.9% annually over the last five years while its revenue grew by 4%. This tells us the company became less profitable on a per-share basis as it expanded.

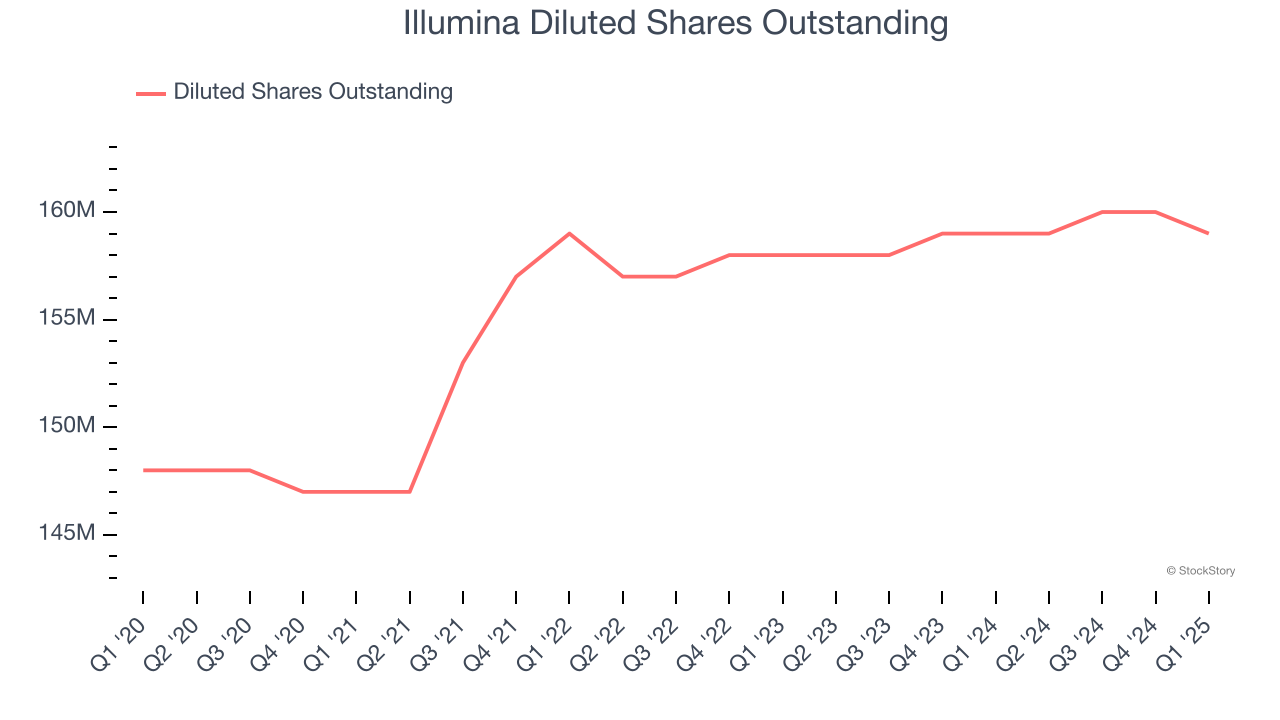

We can take a deeper look into Illumina’s earnings to better understand the drivers of its performance. As we mentioned earlier, Illumina’s adjusted operating margin was flat this quarter but declined by 2.4 percentage points over the last five years. Its share count also grew by 7.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Illumina reported EPS at $0.97, in line with the same quarter last year. This print beat analysts’ estimates by 3.2%. Over the next 12 months, Wall Street expects Illumina’s full-year EPS of $4.15 to grow 11.9%.

Key Takeaways from Illumina’s Q1 Results

It was great to see Illumina beat analysts’ revenue and EPS expectations this quarter. On the other hand, it lowered its full-year EPS guidance missed. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 3% to $77.19 immediately after reporting.

So should you invest in Illumina right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.