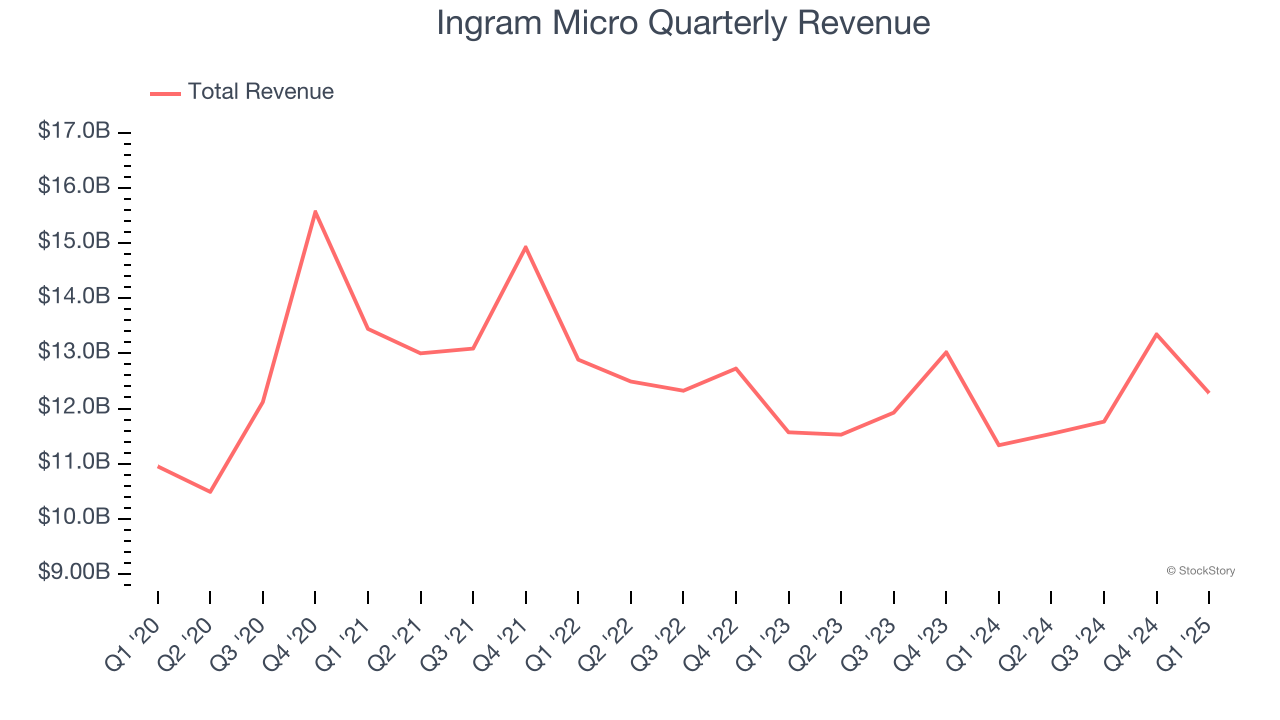

IT distribution giant Ingram Micro (NYSE:INGM) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 8.3% year on year to $12.28 billion. Guidance for next quarter’s revenue was better than expected at $11.97 billion at the midpoint, 1.4% above analysts’ estimates. Its GAAP profit of $0.29 per share was 28% below analysts’ consensus estimates.

Is now the time to buy Ingram Micro? Find out by accessing our full research report, it’s free.

Ingram Micro (INGM) Q1 CY2025 Highlights:

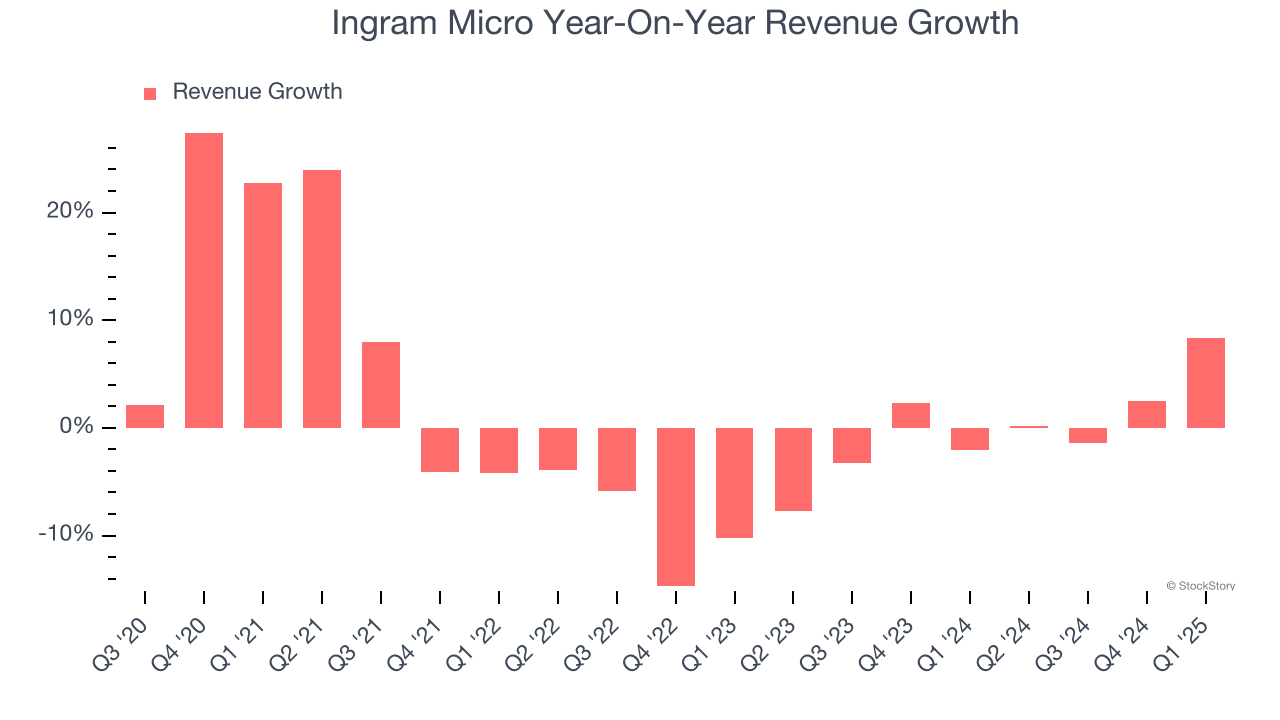

- Revenue: $12.28 billion vs analyst estimates of $11.61 billion (8.3% year-on-year growth, 5.8% beat)

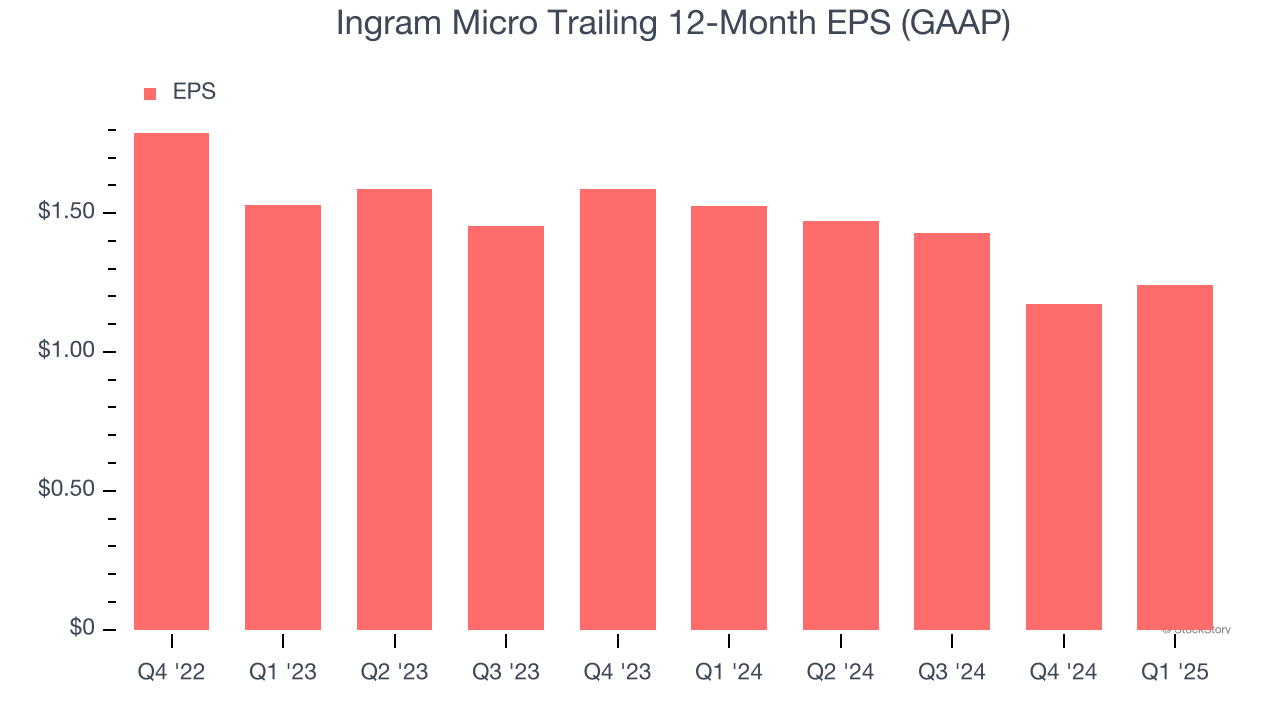

- EPS (GAAP): $0.29 vs analyst expectations of $0.40 (28% miss)

- Adjusted EBITDA: $290.8 million vs analyst estimates of $279.2 million (2.4% margin, 4.1% beat)

- Revenue Guidance for Q2 CY2025 is $11.97 billion at the midpoint, above analyst estimates of $11.8 billion

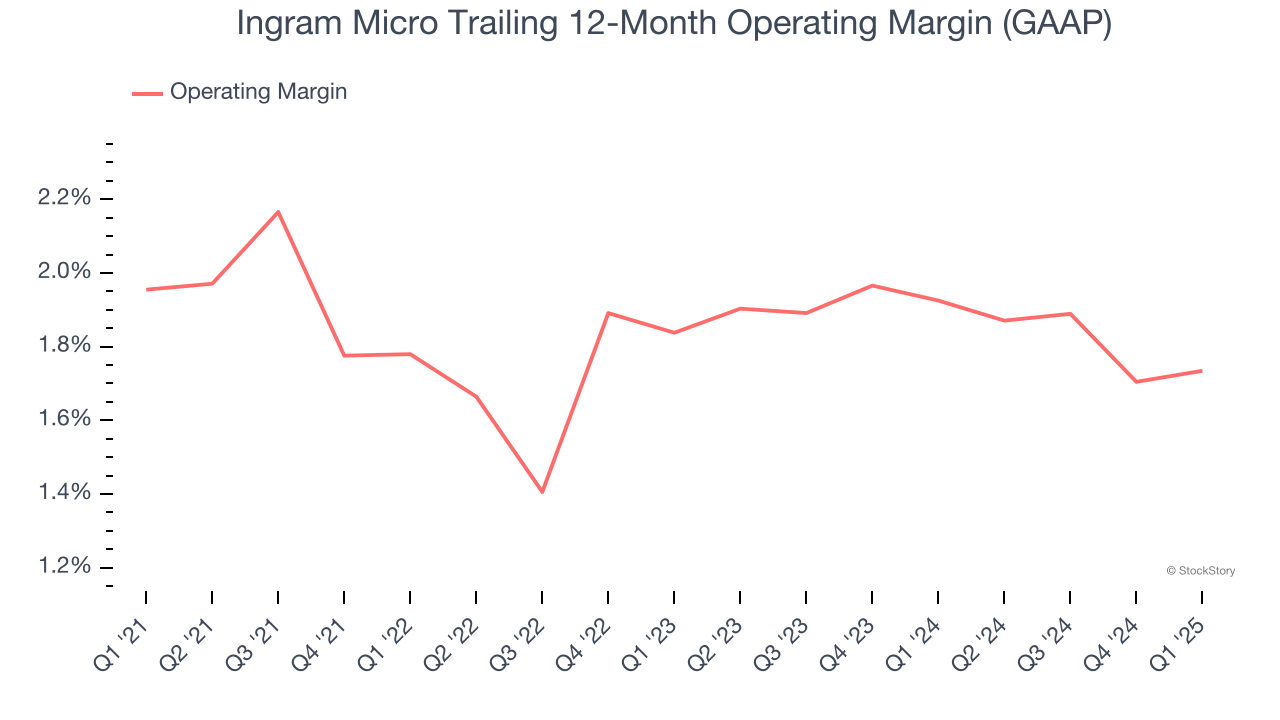

- Operating Margin: 1.6%, in line with the same quarter last year

- Free Cash Flow was -$230.2 million compared to -$135.8 million in the same quarter last year

- Market Capitalization: $4.46 billion

Company Overview

Operating as the crucial link in the global technology supply chain with a presence in 57 countries, Ingram Micro (NYSE:INGM) is a global technology distributor that connects manufacturers with resellers, providing hardware, software, cloud services, and logistics expertise.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $48.93 billion in revenue over the past 12 months, Ingram Micro is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Ingram Micro likely needs to tweak its prices, innovate with new offerings, or enter new markets.

As you can see below, Ingram Micro’s sales grew at a sluggish 1.3% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Ingram Micro’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Ingram Micro reported year-on-year revenue growth of 8.3%, and its $12.28 billion of revenue exceeded Wall Street’s estimates by 5.8%. Company management is currently guiding for a 3.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Ingram Micro was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.8% was weak for a business services business.

Analyzing the trend in its profitability, Ingram Micro’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Ingram Micro generated an operating profit margin of 1.6%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Ingram Micro’s full-year EPS dropped 20.9%, or 9.9% annually, over the last two years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Ingram Micro’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Ingram Micro reported EPS at $0.29, up from $0.22 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Ingram Micro’s full-year EPS of $1.24 to grow 99.7%.

Key Takeaways from Ingram Micro’s Q1 Results

We were impressed by how significantly Ingram Micro blew past analysts’ revenue and EBITDA expectations this quarter. We were also glad its revenue guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its EPS missed. Still, this print had some key positives. The stock remained flat at $19.68 immediately after reporting.

Is Ingram Micro an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.