As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at semiconductor manufacturing stocks, starting with IPG Photonics (NASDAQ:IPGP).

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was 2.8% below.

Thankfully, share prices of the companies have been resilient as they are up 5.9% on average since the latest earnings results.

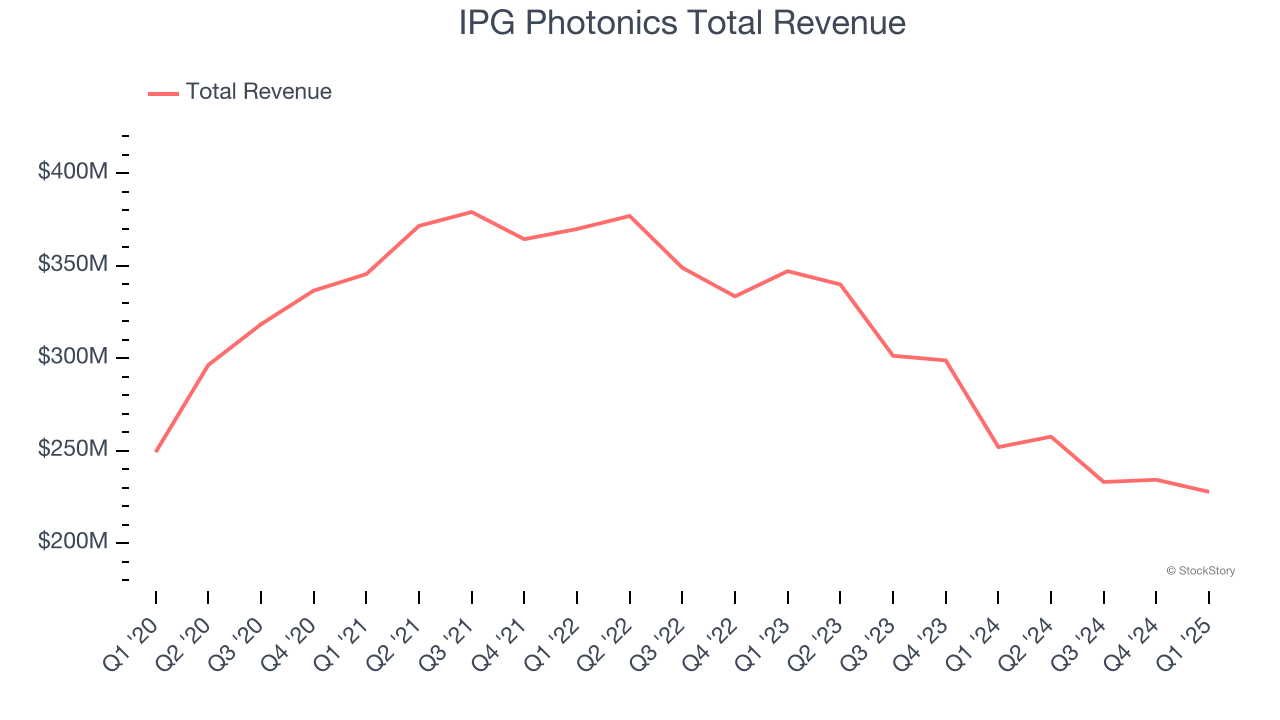

IPG Photonics (NASDAQ:IPGP)

Both a designer and manufacturer of its products, IPG Photonics (NASDAQ:IPGP) is a provider of high-performance fiber lasers used for cutting, welding, and processing raw materials.

IPG Photonics reported revenues of $227.8 million, down 9.6% year on year. This print exceeded analysts’ expectations by 1.2%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ adjusted operating income estimates.

“IPG had a strong start to the year, delivering revenue, adjusted earnings per share and adjusted EBITDA above the midpoint of our guidance and gaining early traction in key areas that are central to our strategy, including medical, micromachining, and advanced applications,” said Dr. Mark Gitin, Chief Executive Officer of IPG Photonics.

The stock is up 8.1% since reporting and currently trades at $68.23.

Is now the time to buy IPG Photonics? Access our full analysis of the earnings results here, it’s free.

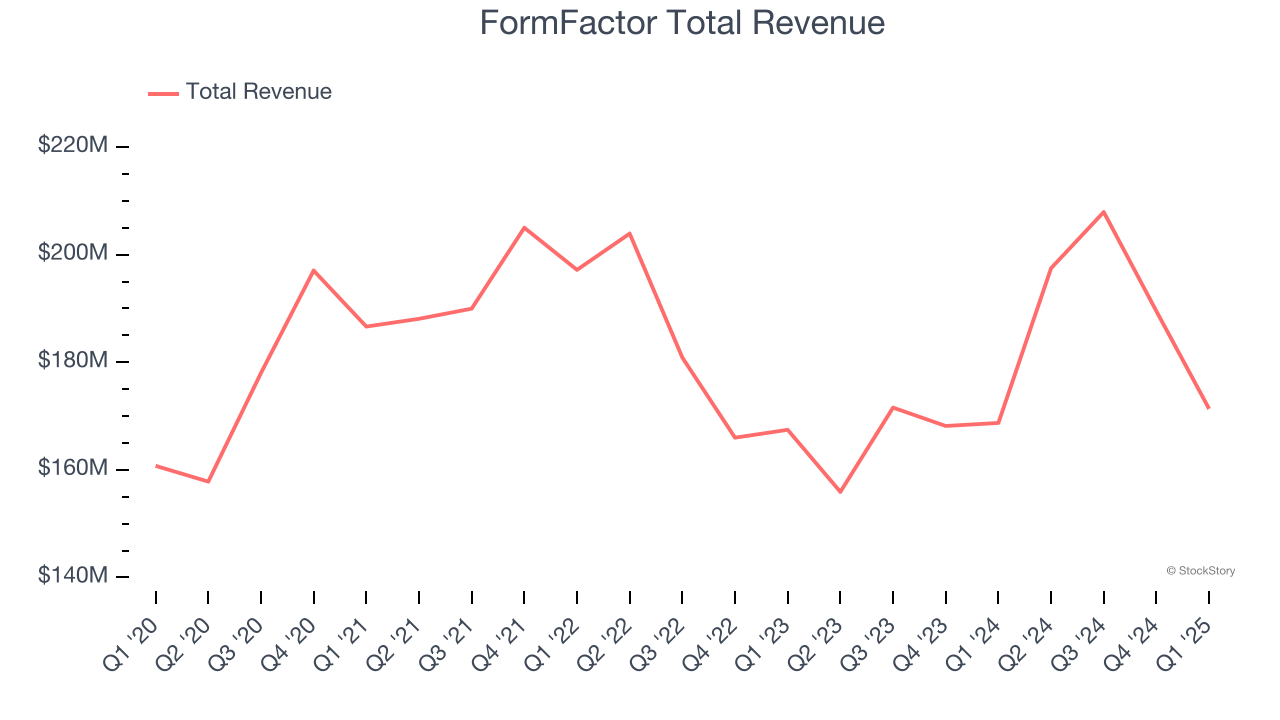

Best Q1: FormFactor (NASDAQ:FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ:FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $171.4 million, up 1.6% year on year, outperforming analysts’ expectations by 0.9%. The business had a strong quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ adjusted operating income estimates.

The market seems happy with the results as the stock is up 14.9% since reporting. It currently trades at $32.25.

Is now the time to buy FormFactor? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Photronics (NASDAQ:PLAB)

Sporting a global footprint of facilities, Photronics (NASDAQ:PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Photronics reported revenues of $211 million, down 2.8% year on year, in line with analysts’ expectations. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 12.1% since the results and currently trades at $17.65.

Read our full analysis of Photronics’s results here.

Amtech (NASDAQ:ASYS)

Focusing on the silicon carbide and power semiconductor sectors, Amtech Systems (NASDAQ:ASYS) produces the machinery and related chemicals needed for manufacturing semiconductors.

Amtech reported revenues of $15.58 million, down 38.7% year on year. This result lagged analysts' expectations by 15.8%. Overall, it was a disappointing quarter as it also produced revenue guidance for next quarter missing analysts’ expectations and a significant miss of analysts’ EPS estimates.

Amtech had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is up 21.4% since reporting and currently trades at $4.08.

Read our full, actionable report on Amtech here, it’s free.

Teradyne (NASDAQ:TER)

Sporting most major chip manufacturers as its customers, Teradyne (NASDAQ:TER) is a US-based supplier of automated test equipment for semiconductors as well as other technologies and devices.

Teradyne reported revenues of $685.7 million, up 14.3% year on year. This print was in line with analysts’ expectations. Overall, it was a strong quarter as it also logged an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ adjusted operating income estimates.

The stock is up 6.6% since reporting and currently trades at $81.88.

Read our full, actionable report on Teradyne here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.